We have been waiting patiently to see an inflection of this magnitude from Alphatec Holdings Inc. (ATEC) for the past three years. This is a Top Tier Inflection:

First, some 411 on Alphatec:

With more than 30 years in the Spine Industry, ATEC's CEO Pat Miles knew exactly what he was doing when he came to Alphatec 8 years ago. He knew that the spine industry was filled with inertia and was ripe for innovation.

Alphatec invested heavily in creating dozens of new products from 2018-2020. With 230 engineers internally, Alphatec truly has become an innovation machine, growing its market share in spine from 1% to 8% in 8 years.

And, ATEC is still innovating:

Alphatec's ramp has been nothing short of spectacular.

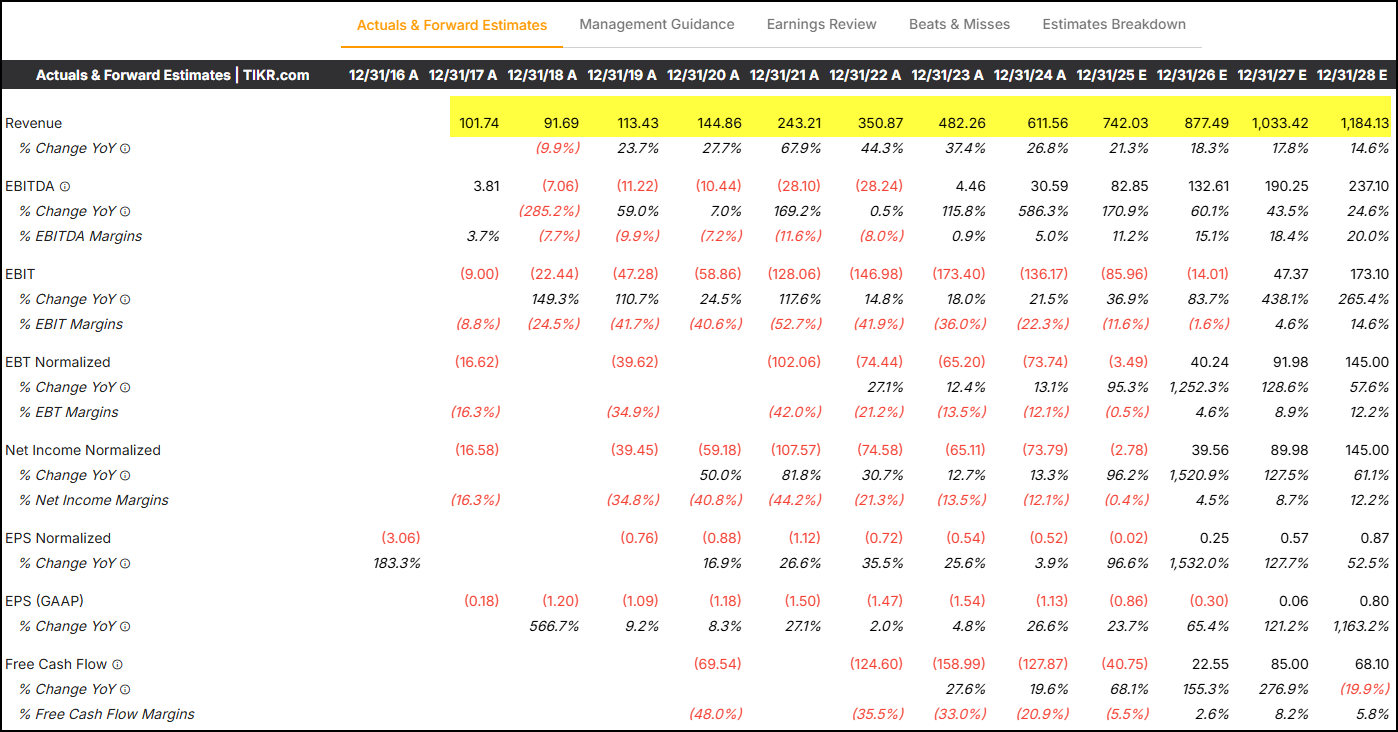

From 2018, the company has grown - mostly organically, but also, with three tuck-ins - from just under $100M to close to $800M in sales this year:

Importantly, in addition to there being room for upside to revenues in 2026 and beyond, relative to consensus, we are also at the point in the company's evolution where incremental revenues will be highly profitable. To this end, we think the company can achieve its 17% EBITDA margin target next year.

There are a multitude of reasons why we believe this inflection point is so powerful.

First, the 8% beat in revenues was its largest beat in three years.

ATEC is continuing to gain market share versus the entrenched larger players in the space like Globus (formerly Nuvasive), growing 6x-7x faster than others in the industry.

Here is a link to the company's slide deck.

Some salient slides of interest to quickly get you up to speed:

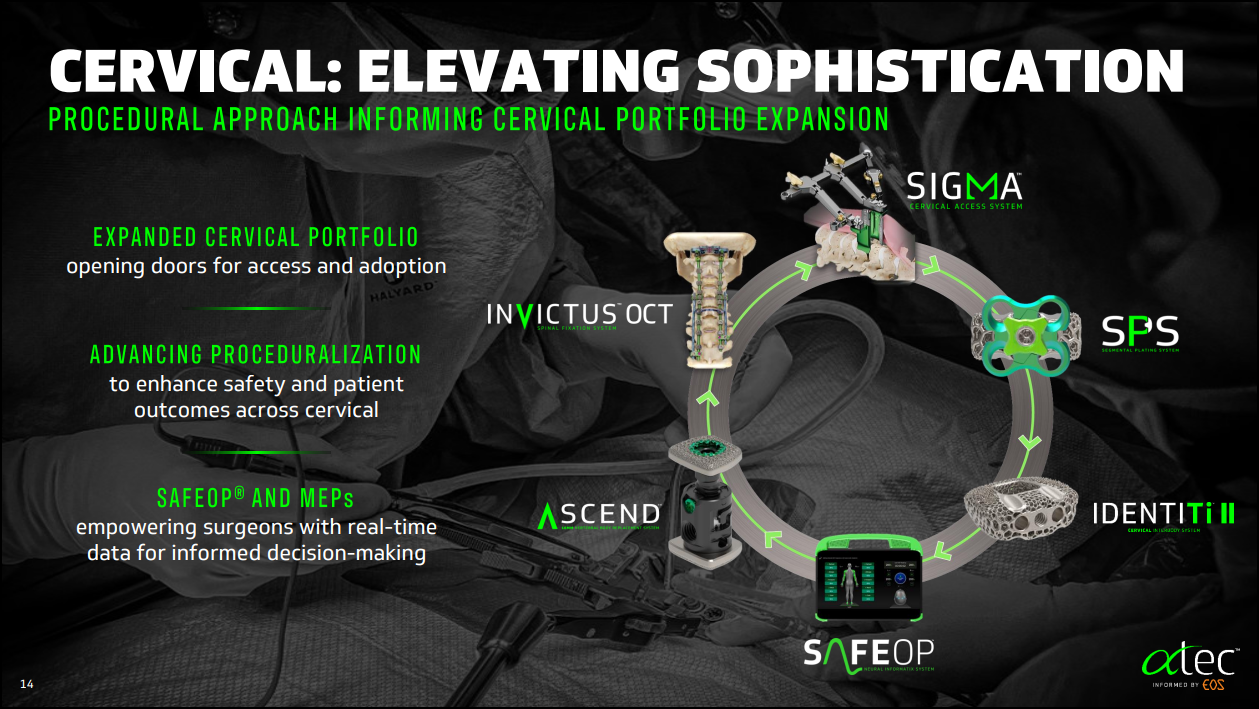

Looking ahead to 2026, with Alphatec's move into the cervical part of the spine paying dividends...:

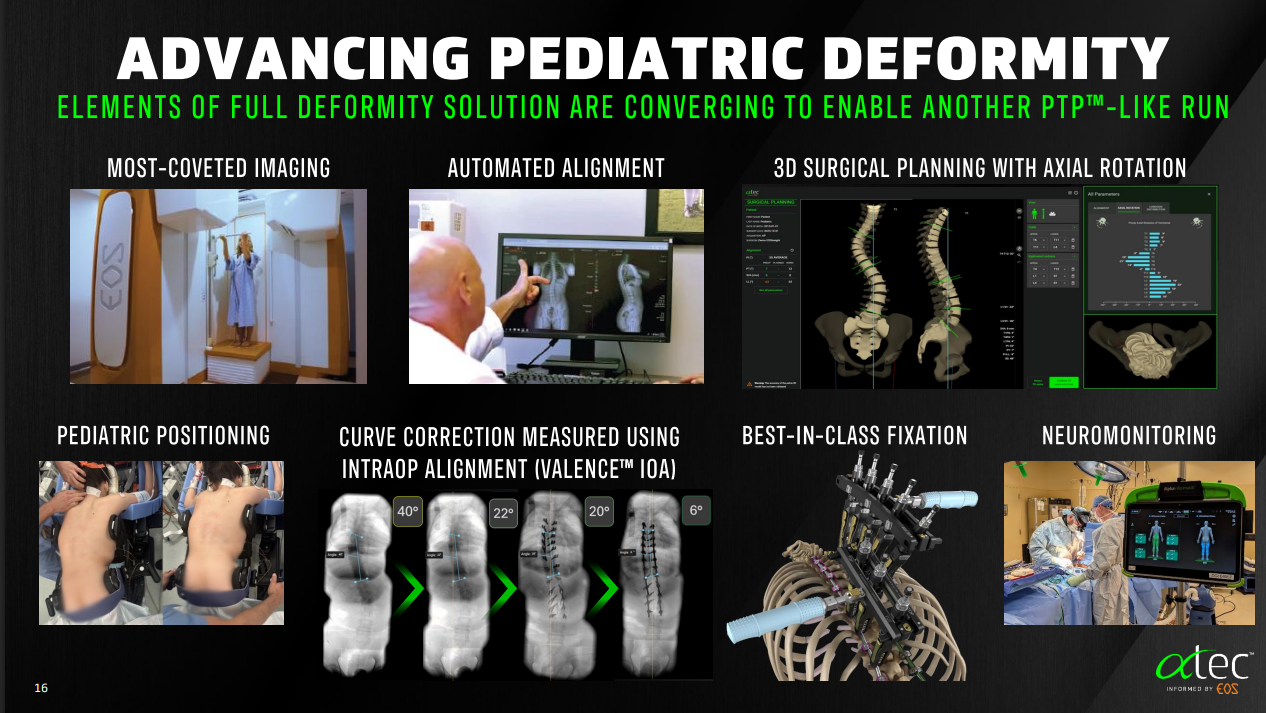

And, expectations high for its third vertical, Deformity, poised to inflect, as well...

We think there will be big upside to 2026 numbers. More on that shortly.

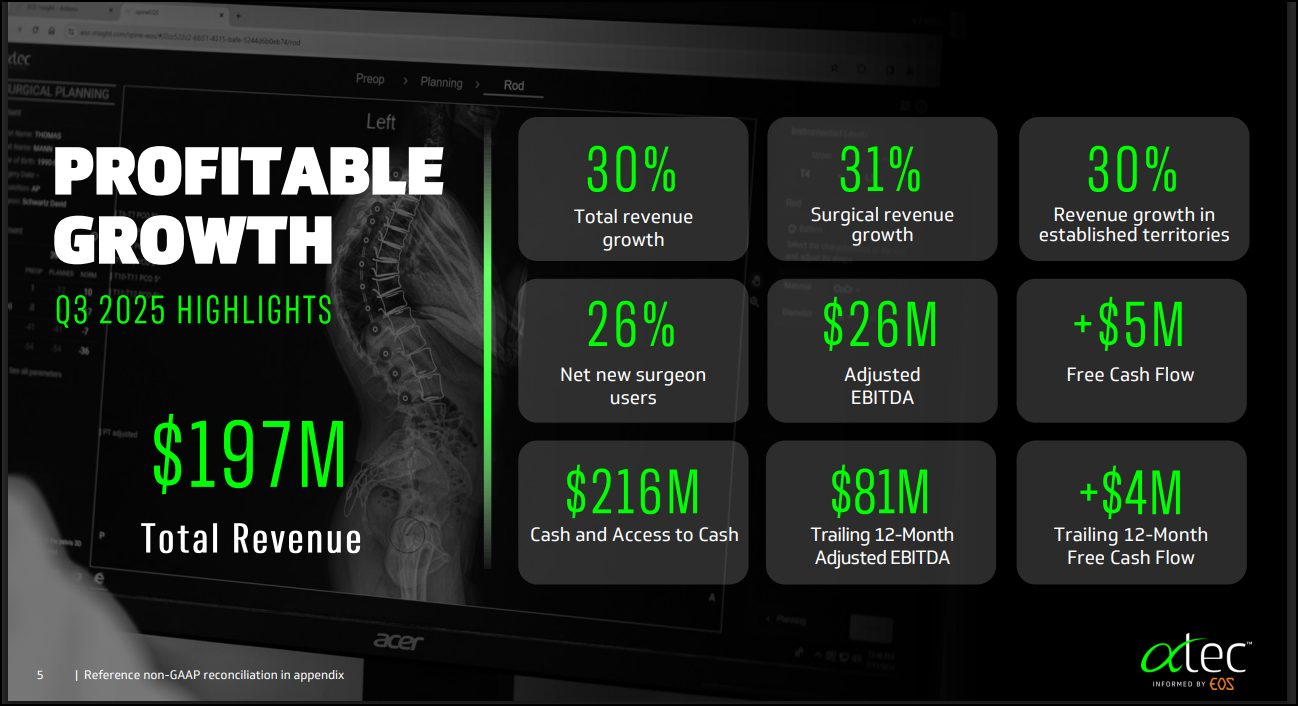

As for the remainder of 2025, some quick stats:

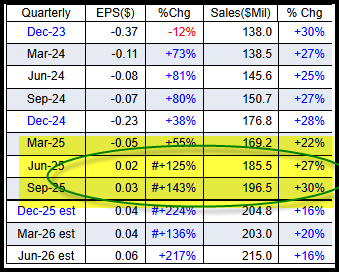

Typically, ATEC barely grows from Q2 to Q3 due to summer holidays. Instead of the 1.5-2% sequential growth seen the last two years, this year ATEC grew 6.2% sequentially, from $185.5M to $196.5M. This is the hallmark of the most dynamic Top Tier Inflections. When growth rates smash typical growth patterns seen from one seasonal quarter to the next, it typically speaks to accelerated adoption occurring in real time.

Take a look (and, also be sure to note how ATEC is growing EPS at accelerating triple digits rates, as well:

Looking ahead to Q4, management - who is known to always give very beatable guidance - issued what we view to be a ridiculously low guide. Typically, Alphatec grows 17-18% every year, sequentially, from Q3 to Q4. As patients look to utilize their deductibles before the year is over, Q4 is always the best quarter for med-tech companies that provide tools for these surgeries.

We believe Alphatec will post ~$231M in revenues in Q4, which equates to a 17% rise from Q3 to Q4. Considering ATEC just blew away the typical seasonality it is prone to each year in Q3, we think the company could even beat our estimate. It could potentially exit the year at a 32-33% run rate.

We think our math is very solid, as this type of business is very easy to model out when the backdrop is stable and healthy as it is now.

Given Alphatec CEO's bullishness on the market-share gains in the Cervical space AND the needle-moving market-share gains they expect for Deformity in 2026, we think there is better-than-even odds ATEC could grow 30%+ in 2026.

To be conservative, we are modeling for just under 30% next year, translating to nearly $1B in sales. This would mean Alphatec will be reaching its $1B Long-Term Target one year ahead of time. But, this is not surprising, as the company has been besting their long-term guidance for years.

With Alphatec the ONLY disruptor in spine and its incredible track record of innovation, spurring a notable ramp in revenues from $100m to $1B in 9 years (even with $125M-$140M coming from tuck-ins), we believe ATEC deserves a 4.5x multiple on 2026 sales.

This gets us to $30 in 2-3 quarters, which is the main crux of this investment.

Finally, one last factor that makes us very bullish on 2026 is that Net New Surgeon Adds inflected to 26% Y/Y growth in Q3, up from 21% growth in Q2. This is an important indicator of future growth, as it typically takes 1-2 years before these new surgeons begin to truly utilize Alphatec's various offerings, implying there is future embedded growth coming in 2026 and 2027 from these recently added new surgeons.

Longer-term, it’s not hard to see how ATEC achieves 20% market share and $2B in sales by 2029, which would get us to $60 in a few years, as well. So a lot of runway here.

BUT, Alphatec will need a new plant by 2027-2028, so there could be some speedbumps on that part of the journey, including a couple-quarter investment period where margins potentially get dented.

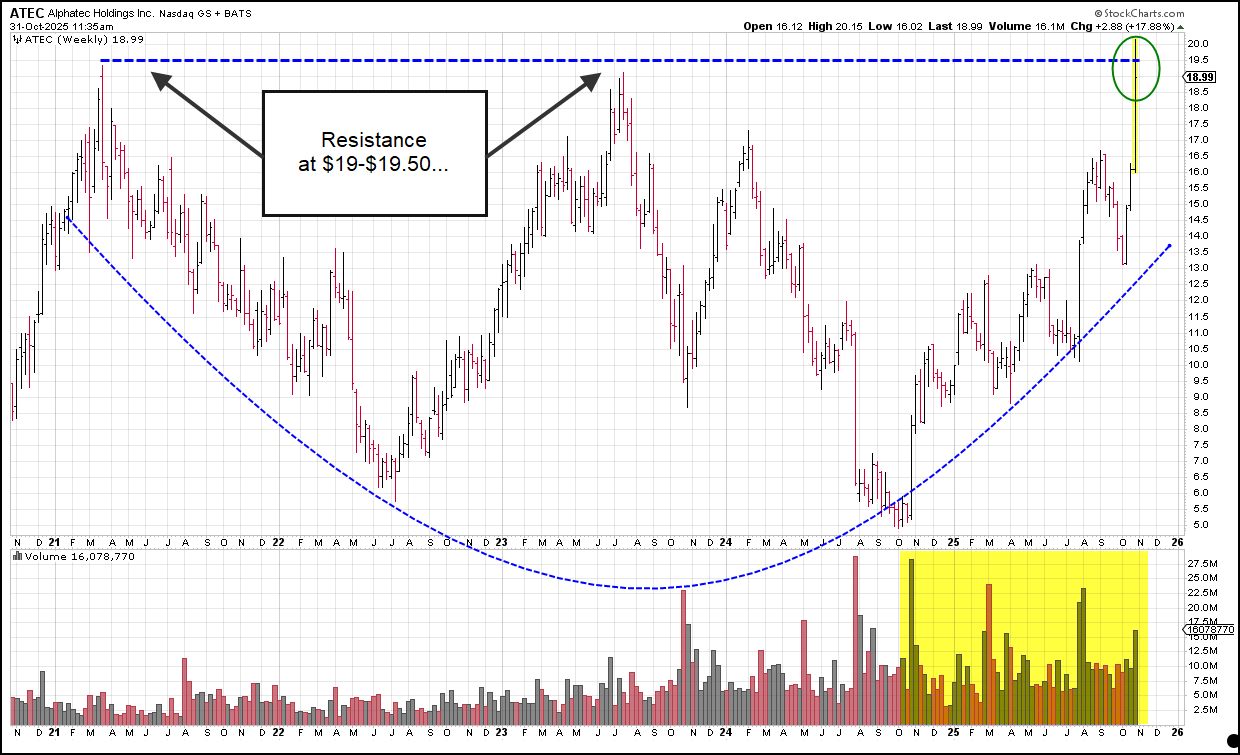

ATEC is poised to clear a powerful 5 year base today. As such, there will be significant long term resistance to clear at the $19-$19.50 level, so expect a flush in the morning.

We therefore plan to bid aggressively in the $18s and low $19s this morning.

Nonetheless, we do not think the flush will last long due to the powerful nature of ATEC's Top Tier Inflection. With this in mind, we plan to accelerate our accumulation in ATEC should $20 be taken out quickly.

We think ATEC finishes the year at $23-$24 as new growth investors move into the name.

Investors Business Daily (IBD) will also likely start pumping it, as Alphatec is poised to grow its earnings at triple=digit rates the next 4 quarters.

The best inflections take years to manifest.

We have been waiting for this ATEC inflection for the past three years. We therefore plan to size up and expect this to be a Top 3 position exiting today.

-----------------------------------------------------------------------------

Disclosure: We are long ATEC stock and calls. We may change our positioning at a moment’s notice, without notifying you of any such moves.

Disclaimer: All of the information in this piece has been prepped by Inflections Consulting LLC. Readers should know that it would be incorrect to assume that past and future names of interest will be profitable or will not turn into a loss. Inflections Consulting LLC does not and will not assume any liability for any loss that could occur if you invested in such stocks written about.

All the content in these reports have been prepared by Inflections Consulting LLC. We believe our sources to be reliable, but there is no guarantee here. The information in this piece does not constitute either an offer nor a solicitation to buy or sell any of the securities name-dropped in this piece.

All contents are derived from original or published sources believed reliable, but not guaranteed. This report is for the information of Top Tier Inflections members/subscribers, only. Absolutely none of our content may be reproduced in whole or in part without prior written permission from Inflections Consulting LLC. All rights reserved.

In no shape or manner should the views expressed in this piece be considered investment advice. We reserve the right to change our positioning in our ATEC stock and options positions at a moment’s notice without updating you on any such change in opinion and positioning. That may be tomorrow, even before our price target is hit. Facts change, our opinions can change quickly too.

Investors need to consider their investment risk tolerance before investing in the stock market and also before investing in any of the stocks mentioned in this report.