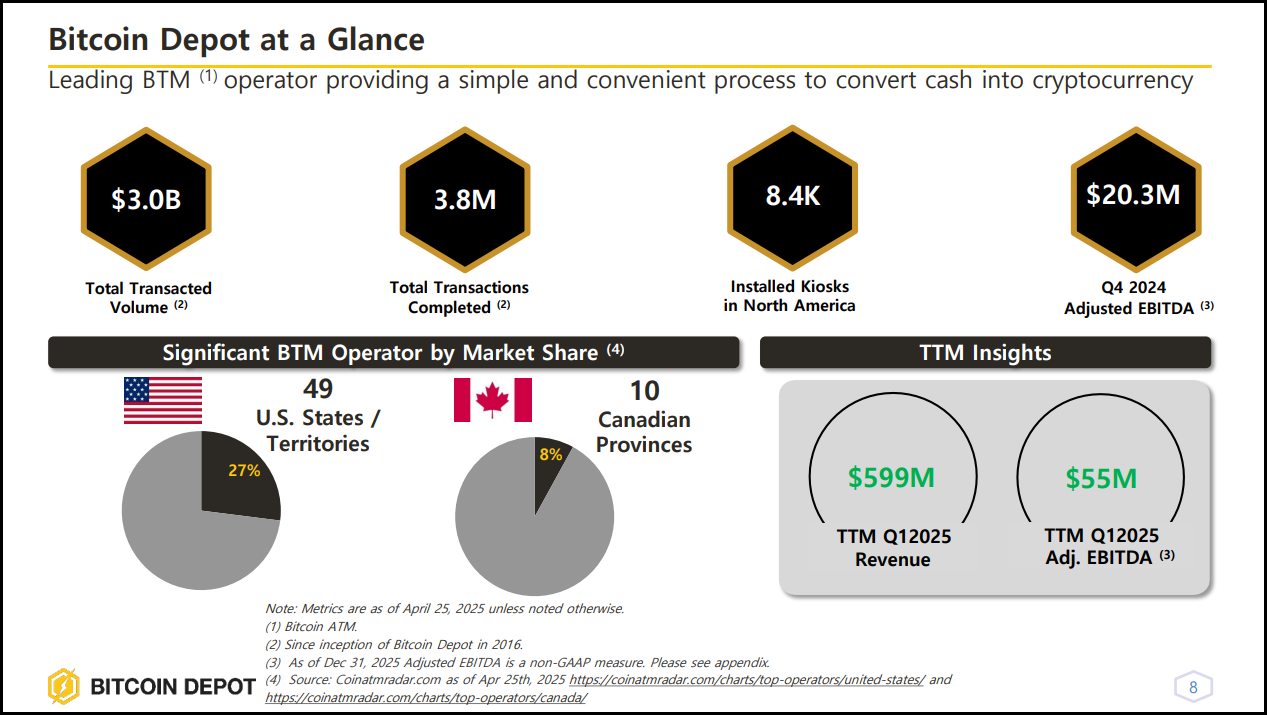

Bitcoin Depot Inc. (BTM) is the largest bitcoin ATM operator in the US:

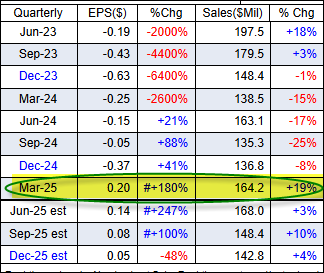

Bitcoin Depot came public via a SPAC in 2023. Like most SPACs it was left for dead...at least, until recently… In Q1, the company posted arguably its best quarter ever, a Top Tier Inflection:

We missed it. We should have caught it, but we did not. What a move:

What would be worse, however, would be to miss another big-up leg in such a powerful stock that has already doubled, and then some. After all, for a stock to become a 5X-er, it first needs to double, then triple, etc...

In this vein: after working on BTM extensively over the last week, we attach 80% odds that another new up leg is poised to manifest, one that should catalyze a second leg up to $6.5-$7.5 by the fall. Of note, while it is too early to go there until we see what the Q2 numbers are, we currently attach 50% odds BTM could more than double and head into the double digits by late-2025/early-2026.

Considering how strongly Bitcoin is holding above $100,000 and how it is getting aggressively institutionalized weekly, thereby further tightening its overall float further, we agree with Tom Lee's prediction that bitcoin could see a $200K+ handle by year-end. 35% odds that happens. We think 65% odds for $150K.

Quick sidebar - BTM's business is NOT correlated to bitcoin's daily vacillations and its intermediate trends. Adoption continues to broaden out, along with the average transaction size, relative to prior quarter's transactions sizes (note highlights):

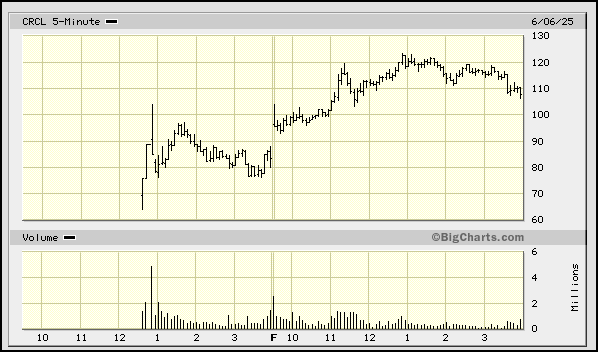

In the past few weeks, in additional to embracing the MicroStrategy, Inc. (MSTR) strategy of raising capital to increase its Bitcoin Treasury holdings, institutional investors are going wild over new IPOs in the crypto space.

In case you missed it, Circle Internet Group, Inc. (CRCL), the 2nd largest stablecoin in the crypto ecosystem, looks poised to become the next CRWV. Even with scores of insiders dumping stock in the IPO, new institutional holders like Cathie Wood bought aggressively (4M shares) into CRCL on its first two days of trading. After pricing at $31-$31.5 above the mid-point of the expected range, CRCL opened in the $60s and finished the week above $100, more than tripling in two days:

Turning back to BTM, notwithstanding its powerful leg up the last month, shares are STILL attractively valued. To be frank, while we are unsure of what the appropriate multiple should be for a Bitcoin ATM business, at less than 3x likely forward EBITDA and 0.3 of 1x sales, it is not unreasonable to see further multiple expansion in the coming quarters to a mid-single-digit forward multiple.

Looking at current consensus, we see STRONG UPSIDE – another factor that makes us very bullish on shares at current levels and on any dips to the low-to-mid $4s.

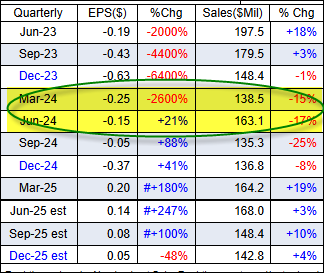

To wit, note the big move last year in revenues from Q1 to Q2. Typically, Q2 is the STRONGEST QUARTER of the year for the company; as tax refunds hit, many younger consumers are using that extra cash to buy Bitcoin. While this trend may not be as strong this year and going forward as it has in previous years with consumers utilizing apps that help expedite quicker tax refunds, considering that the average sequential gain in revenues from Q1 to Q2 the last three years has been ~13%, we think the odds are very high we see a 10% sequential bump in Q2 revenues, relative to Q1 #s:

Current consensus is only calling for a 2% sequential increase in revenues, along with a DROP (?!) in EBITDA and EPS. We view current consensus as VERY BEATABLE:

To be conservative, we are only modeling an 8% sequential increase in revenues from Q1 to Q2, or, $177M, $9M above current consensus. But, wait, the story gets better, along with Q2's likely final revenue #s.

On top of the seasonal bump, the company is also going to start to see a natural bump in its top-line over the next 4-6 quarters due to the company coming ouf of the other side of what we view to be its biggest upgrade cycle ever. After California put a # of restrictions on Bitcoin ATM deposits in late 2023, the company spent most of 2024 re-deploying hundreds of these machines and thousands of others from lower-performing locations to new locations by Q2 of last year.

Typically, it takes 4 quarters before the company sees the benefit of those new locations that reach a steady state run rate usually seen in quarters 5-8 once they have been relocated to new profitable locations.

Here are some stats gleaned from the company's most recent conference call:

With these additional data points, one can see how the expected seasonal uplift in Q2 will also see a further improvement in the revenue associated with the 2,000+ kiosks kicking into the 87% higher revenue run rates associated with these kiosks installed at profitable locations for 12-24 months.

By 2026, this could translate to an additional $20M-$25M a quarter in add-on revenues. So, a couple of very important reasons why there is a high likelihood that Q2, in particular, will come in well above consensus, along with the second half of this year and 2026, as well.

On the bottom line, we are even more bullish with our expectations. Since DESPAC-ING the company has done a fantastic job of taking out a number of public company costs associated with this process, zeroing in on cost cuts in areas such as accounting and also legal fees.

At least for now, the company seems to have found religion on its current $15M per quarter cost structure. This means we should see additional leverage in its model kick in. To wit, for Q2,

We see strong potential for a sizeable beat on the bottom line to $0.24-$0.28 in EPS, along with strong upside in its EBITDA line, relative to consensus. Of note, should our numbers be right, a $.26 mid-point result in EPS would be a strong 30% bottom line beat compared to current consensus. While we would see a sequential down tick in EPS in both Q3 and Q4 as seasonality benefits wane, rough math suggests BTM has very good odds to do ~$.75 in EPS this year.

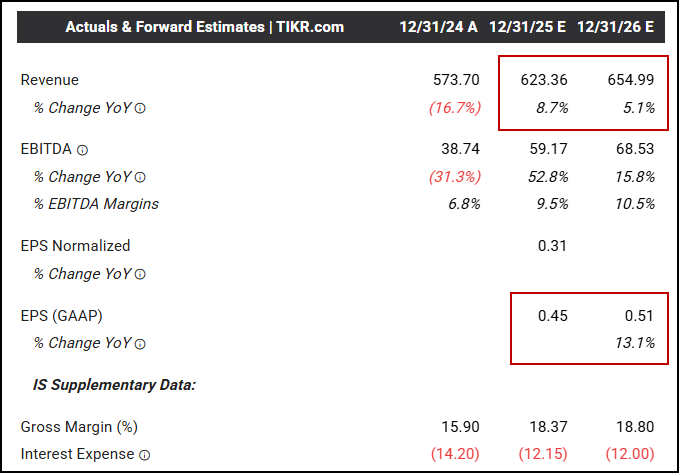

Looking further out to 2026, we think the company can post $800M in revenues and $1.15 in EPS. Put a 0.7 of 1X Price-to-Sales Multiple and an 8X Price-to- Earnings multiple on these forward #s and one can see how BTM doubles, and then some, from current levels to $10+ by year-end in an uber bull scenario playing out.

Here is what 2025 and 2026 consensus looks like currently:

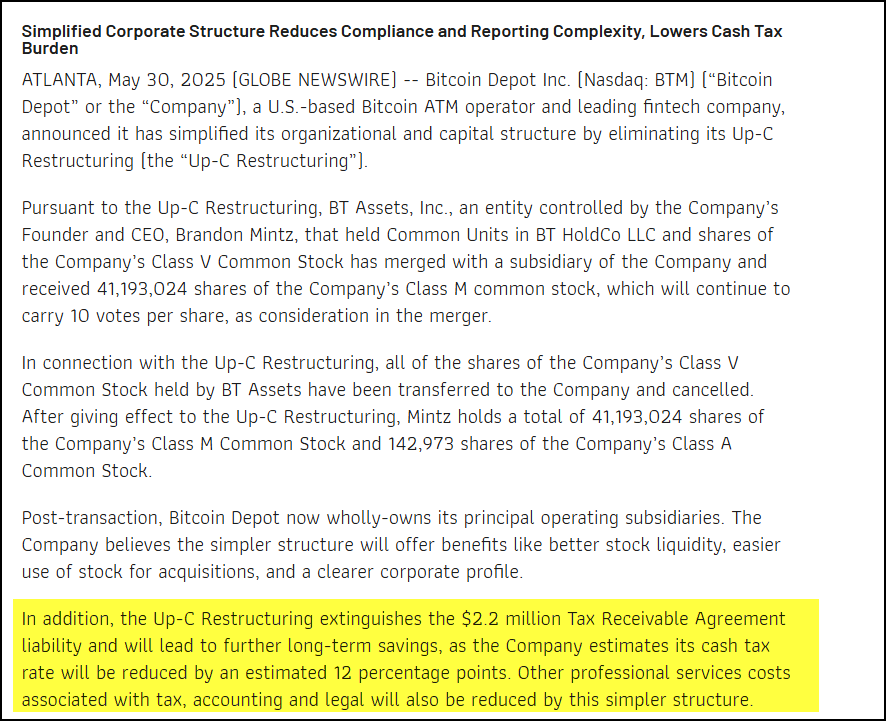

Last week the company announced a change in its share structure. As the company's largest shareholder, the company's CEO has THE BIGGEST MOTIVATION of any shareholder to get the stock dramatically higher. We love this move. Note the highlights, which shows the strong costa and tax savings by switching the Class of shares as it did:

So, while there is certainly a risk the CEO could unload shares at some point, when you consider how everything is going so right for the company suddenly and how its improved cost structure will lead to additional leverage in its model as revenues move back toward record quarterly levels of ~$200M next year, we do not think the CEO sells stock any time soon.

With 63M shares outstanding and taking into account the CEO's 41M shares held, there are only 23M shares freely traded in its float. With the stock still so attractively valued and with the stock trading almost 2M some days, the entire shareholder base has been turned over. Many of these are value oriented investors who still see the value we do.

Keep in mind, this is a very basic business to model out, so we like our #s a lot. And we are sure many other investors have the same set of #s we do. We just wish we did the math a few weeks ago...

Nonetheless, considering its enhanced liquidity, there are tangible benefits from not being the first one in the pool, i.e. the improved liquidity allows for bigger position sizes and a much easier time establishing and exiting one's position compared to how it was trading pre-Q1 print.

Even with things looking very strong for the company and its future prospects bright for its stock in the second half of the year, clearly, there are risks to be mindful of, including:

- A Democratic Congressman has introduced a Know Your Customer Bill meant to tighten regulations on Bitcoin ATM transactions. We attach a 3% chance anything passes that is Anti-Bitcoin related in the coming quarters/years. We had to mention though, as it is really the main risk we have come across.

- Further State actions are another risk. Similar to how California lowered the max deposit amount to $1k a transaction, other states could follow suit with additional onerous laws restricting activity on the local level. Three other states have also followed California's lead. So this is a risk to think about when sizing one's position in the name.

We are comfortable with these risks. BTM has strong protocols in place to deal with new restrictions, as they develop. One way they are hedging this risk is by moving into new countries. Australia has seen interest in Bitcoin J-curve, so the company is placing 300 machines in the country this year. Two other countries are expected to follow.

- The final risk revolves around a potential tightening in the vig Bitcoin Depot takes with every cash deposit. Should the current ~16% commission be forced to much lower levels, that would put a serious dent into its margins and its current business model. Again, something we are not worried about in the near-term, but something worth mentioning. The same holds for COIN by the way.

In aggregate, we think there is a nice window for BTM to have another big leg up from current levels in the coming days and weeks and, in particular, into year-end.

Similar to SEZL's powerful inflection point, BTM's inflection point left its stock much higher, but also still attractively valued as forward numbers went up dramatically for both companies after their respective inflection points manifested. We think a similar thing happens after Q2 numbers. Assuming the company beats consensus by a strong margin on the bottom line, in time, 2025 EPS numbers may come in at $0.75 cents, which is ~66% higher than current consensus. So even if the stock were to go to our base case levels, it would actually be trading for a cheaper valuation up 50% vs. current prices.

This is why we see 50% odds for a spirited move to $10+ by the end of the year.

Taken together, we remain buyers on all and any dips in the stock to the $4.30-$4.6 zone. We think the stock heads into the $5s soon, so we plan to be mostly full with our purchases over the next few days.

With our conviction a 10-rating on a very attractively priced stock, we are also implementing a time stop in BTM through Q2 numbers. We want to be long into this print, as new fireworks could and should materialize for the stock, thereafter. On this front, the bigger any Q2 beat, the more inclined we would be to trim less of our position once our base case levels are hit, thereby positioning us to treat this as a longer-term hold into 2026, perhaps, with a third of our position.

STOP LOSS: Thereafter, we will most likely implement a trailing stop loss below the company's 50-day SMA, post its Q2 print.

Should our math be wrong and were the stock to react badly to Q2 numbers, in that scenario, we would then exit the stock.

Always good to plan for all contingencies and to adopt the principles applied by the Stoics, where a base case, an upside case and a worst case scenario are all visualized well ahead of the catalytic event transpiring.

-------------------------------------------------------------------------------

Disclosure: We are long BTM for the capital we oversee. We may change our positioning at a moment’s notice, without notifying you of any such moves.

Disclaimer: All of the information in this piece has been prepped by Inflections Consulting LLC. Readers should know that it would be incorrect to assume that past and future names of interest will be profitable or will not turn into a loss. Inflections Consulting LLC does not and will not assume any liability for any loss that could occur if you invested in such stocks written about.

All the content in these reports have been prepared by Inflections Consulting LLC. We believe our sources to be reliable, but there is no guarantee here. The information in this piece does not constitute either an offer nor a solicitation to buy or sell any of the securities name-dropped in this piece.

All contents are derived from original or published sources believed reliable, but not guaranteed. This report is for the information of Top Tier Inflections members/subscribers, only. Absolutely none of our content may be reproduced in whole or in part without prior written permission from Inflections Consulting LLC. All rights reserved.

In no shape or manner should the views expressed in this piece be considered investment advice. We reserve the right to change our positioning in our BTM stock and options positions at a moment’s notice without updating you on any such change in opinion and positioning. That may be tomorrow, even before our price target is hit. Facts change, our opinions can change quickly too.

Investors need to consider their investment risk tolerance before investing in the stock market and also before investing in any of the stocks mentioned in this report.