Sometimes the best stock to buy is the one you already own. This was certainly the case for two of our best 2024 picks, APP & WGS, thus far this year.

We think Byrna Technologies, Inc. (BYRN), can do an APP or WGS and continue to be a big market leader throughout 2025 as well. Let's dig in.

First, Byrna has a very easy business to model. Consumers love their non-lethal guns. The level of sales the company is able to produce is perfectly correlated to the money funneled into their various marketing channels.

During Byrna’s last conference call, Management stated new channels were opening up for the company and that consumer awareness of the non-lethal space has increased markedly:

"We are also expanding the platforms where we are running our advertisements as more and more cable and internet platforms are greenlighting our advertising campaigns.

In the Q4, most of the $21.3M in web sales, our highest-margin sales channel, were directly attributable to our current roster of influencers. These influencers spread the word about our mission to provide less-lethal personal-security solutions and they have helped us successfully build a very strong brand awareness.

This has also allowed us to build a more robust multichannel marketing strategy that now includes traditional media such as cable and broadcast networks. Prior to our advertising pivot, we were not allowed to broadcast on traditional broadcast TV channels.

Fast forward to now and we are able to advertise regularly on new networks and we are also frequently featured in news stories as less lethal solutions become a larger part of the conversation."

Looking ahead, in addition to testing out 4 company-owned stores – to be rolled out in CYQ1 – Byrna is also trialing a new store-within-a-store model. They are rolling out storefronts within 12 initial Sportsman Warehouses. We believe this new initiative will be a needle-mover next year.

Even a low-end estimate of $25K per store could translate into $25M in sales for this new vertical next year. What’s more, there is nothing stopping Byrna from adding additiional retailers to the store-within-a-store model.

The right new products ALWAYS spur major inflection points.

Well, next up for Byrna is the launch of its highly-anticipated Compact Launcher (CL). Though the Byrna states the CL will arrive this summer, CEO Bryan Ganz has shown a penchant for beating consensus expectations mightily over the past four quarters.

Does the CR possibly get released early, in March, April, May or June? Hmmmm..

Byrna will have 30k CL’s in inventory, on the shelves, ready to be shipped whenever the new CR does drop. That's $18M of high-margin revenues that should immediately be filled – most likely, the majority of it in the August quarter. So, the CL is, by far, the most important forthcoming catalyst for the stock.

The CL will be the company's most important product launch ever. We expect incredible demand for it out of the gate. Remember, the prominent complaint lodged by Byrna customers is the desire for a smaller gun. The CL is 30% smaller than the Byrna SD, making it fully concealable.

This is a game-changing factor that should bring in a substantial number of new women buyers into Byrna's ecosystem:

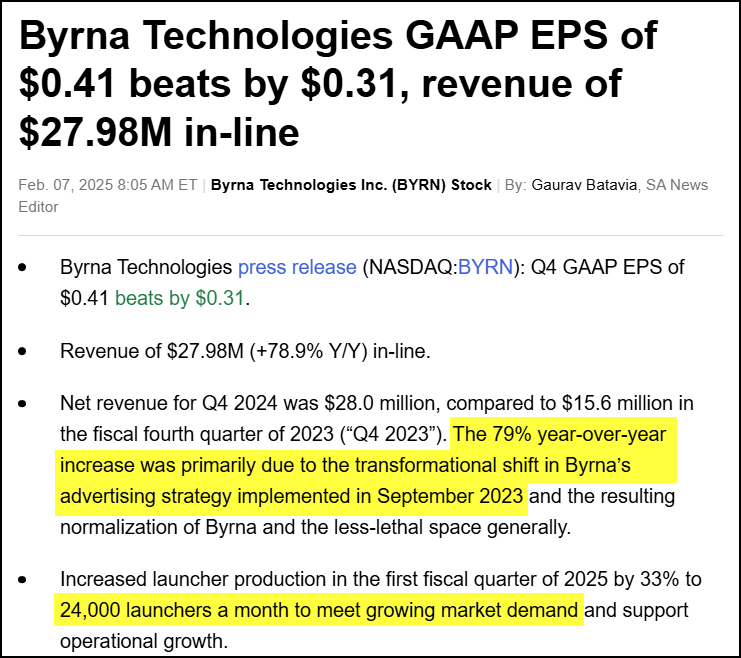

A quick note regarding Byrna’s recent Q4 report on February 7: It offered significant support for our Bull Case to $100, as the company demonstrated powerful leverage in its model.

As revenues ramped from $20.9M in Q3 to $28M in Q4 (34%), Byrna's expenses increased by only $1.3M sequentially, from $12.2M to $13.5M.

Viewed another way, EBITDA improved $3.3M on a sequential increase of $7.1M in revenues, equating to a 46.5% drop-down in margin.

During the Q3 call, CEO Bryan Ganz mapped out how Byrna expects its EBITDA margin to increase as certain revenue thresholds are met and exceeded.

Personally, I think EBITDA margins could go to 35-40% in five years if Byrna achieves $1B in sales by then, like I believe they can.

So, if we reverse-engineer what is coming for Byrna in the coming quarters, we should be able to etch out a reasonable model for where the puck is going to be, well ahead of the sleepy Sell Side guys.

This is where we take a little ride on the Crazy Train. Because, when we model out what is coming at $43M and $60M a quarter – where WE sit for Q3’25 and Q4’25 – the earnings growth numbers get VERY HEADY, very quickly.

We know the Compact Launcher is going to drop by May or June. That is $18M in sales poised to be shipped, perhaps very quickly. The CL launch would then open the spigots for what will be Byrna's FIRST and SIGNIFICANT upgrade cycle.

Byrna will have ~600k email addresses in their database to blast out the news of the CL release. We estimate 25% of this entrenched customer base will buy another Byrna, expanding the company's TAM significantly. That would be 150k CL's.

The timing is perfect in the near-term. We can envision 10s of thousands of new Byrna owners, brought in by the company’s cadre of new celebrity endorsers including Lara Trump, Megyn Kelly, and, I think Roseanne Barr, as well. We think this equates to a LOT MORE women becoming new customers and members of the loyal Byrna fold.

So, $180M gets added to the existing run rate biz of $30M’ish a quarter, or, $120M a year.

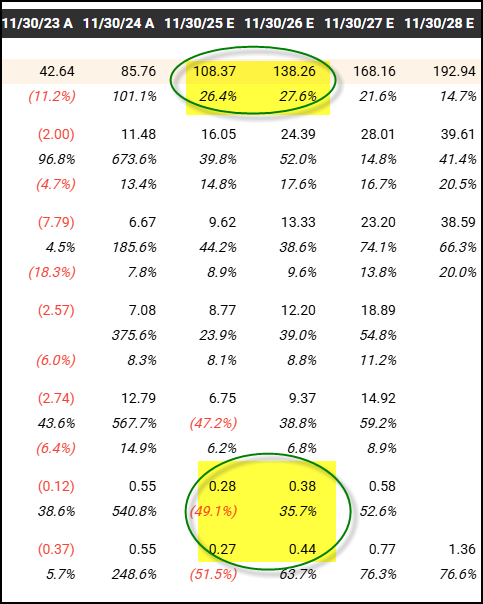

This brings us close to our $310M revenue estimate for Fiscal 2026, along with $3.13 in EPS.

In early March we could see a SIGNIFICANT upcoming catalyst for the stock. We think Byrna COULD proclaim its biggest pre-announcement ever.

Some quick math:

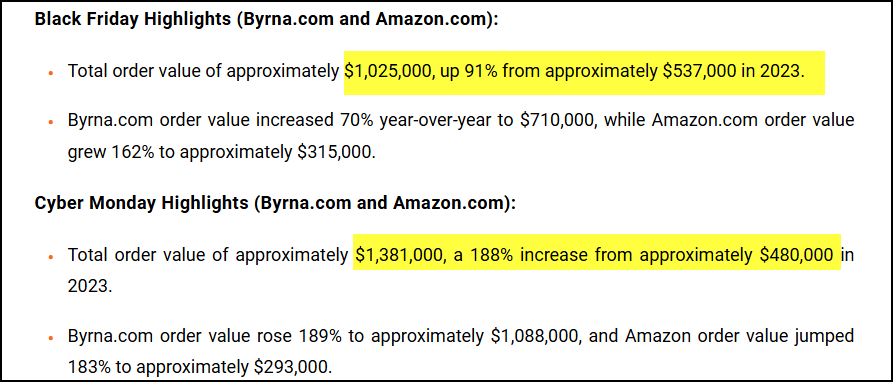

In early December, Byrna pre-announced a stellar set of results from Black Friday and Cyber Tuesday:

This $2.4M in revenues will all be booked in the current quarter, giving us a one-time revenue benefit that will help to amplify the potential pre-announcement from the company.

With Byrna doing $28M the prior three months to December, it is logical to assume they could have done an additional ~$9M for the month, bringing us to ~$11.4M for the first month of the quarter.

This is where things get super interesting.

On January 7th, during an interview with Roseanne Barr, the CEO Ganz stated the company was running at a $15M run-rate. I almost fell off of my chair…

We take this to mean Byrna’s new marketing channels and its new celebrity endorsements are resonating more swiftly with a growing audience of consumers, creating a real-time J-curve in its financial results.

January is one of the slowest months of the year. It seems as though Byrna has already re-accelerated to consistent 100% YoY revenue growth rates.

More math:

Assuming Byrna did $3.75M in Week 1 of January, and then decelerated to a $3M weekly-clip for the rest of the month, then January would clock in at $12.75M – another record month!

So, call it ~$11.4M for December, ~$12.75M for January. That's $24.15M in revenues for the first two months of Q1, "theoretically in the bag,” with potentially conservative math for January.

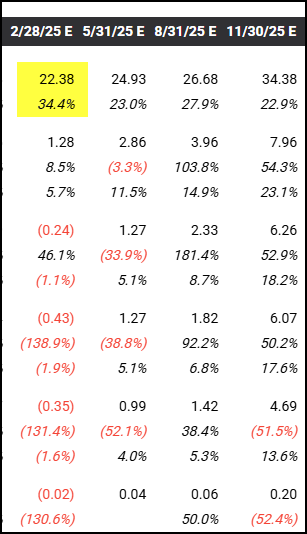

Here's consensus estimates:

If we pencil in $6.375M for February, or half of January revenues, which we view as an easy bar to hurdle, that gets us to ~$30.5M for Q1’25. At $30.5M, revenue would be ~$8M+ above consensus, or nearly 40% above the sleepy Sell Side.

Are we too optimistic? We don’t think so but it has been known to happen… Let’s take another look.

As we consider the rest of the year, we know Q2 is seasonally stronger. We should see a bump to $32M. Then, we get the J-curve ramp for Q3 in August.

With $23M in Compact Launcher-related sales kick-starting $43M in Q3 revenue, and then another $35M in estimated CL-related holiday/Xmas sales boosting the overall revenue to $60M in Q4.

Fiscal 2026 is farther down the road. But, we think a full year of the CL contributing more than half of Byrna's revenue gets us to $300M+, along with an eye-opening jump to $3+ in EPS.

So, two years of almost triple-digit growth, along with earnings potentially rising 1,000% over three years. Whoa, growth stock investor nirvana. Think SMCI, ROOT, POWL and WGS last year…

We believe a similar move is in the works for BYRN in the coming quarters. If the CL should become its best-selling product ever, as we think it will, BYRN has the potential to be one of the most memorable ramps of organic growth we will witness over the next 12-18 months.

Yes, my numbers are crazy high relative to consensus for the next two fiscal years. But, for many good reasons, the consensus appears WAY TOO LOW for us. This only magnifies our appearance of being off-the-hook cra cra:

Of course, we could be dead wrong about our projections.

Maybe Byrna will experience up manufacturing difficulties with Compact Launcher. It's possible. Additionally, Consumer Spending could suddenly slow down, crimping sales. Although, we think Byrna is very recession-proof at a $400-$600 price point.

We like our odds on both risks noted above.

Currently, BYRN is trading like a drunken sailor, not sure which way it is gyrating.

It's understandable. The stock has had quite the move. It also got hit yesterday in sympathy to the technical breakdown in AXON Enterprise, Inc. (AXON), which dived a second straight day, after decisively cracking its 50-day SMA yesterday.

We are playing the long game here. We understand BYRN may pullback some more in the near-term due to what has been a very heavy and tough tape, Friday being no exception.

The overall market breaking down further is our biggest risk I therefore believe.

IF our numbers are right for the next 4 quarters (I attach 70% odds), then, on the other side of this messy tape, BYRN stands poised to go on its powerful move yet.

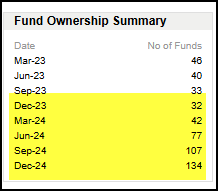

Of note, both Fidelity and Capitol Group bought almost 3.5M shares in Q4. Bryan Ganz owns ~1.7M. So, the float is super tight. There are only 23.5M shares fully-diluted. Fund sponsorship has expanded sharply in the last three quarters.

We expect this trend to continue further:

Add in a feel-good American story, with 100% of their parts, accessories and non-lethal guns being assembled and made in the USA the next two quarters, and there is NO Supply Chain, Tariff, or Currency Risk to the Byrna story.

We like that a lot.

Keep in mind, BYRN is trading near all-time highs. We think the stock will gather significant strength after the early March pre-release, potentially, even sprinting to new highs then:

Here at TTI, our eyes-on-the-prize quarter is expected to be revealed in early September, when the company typically announces its Q3 quarter. While typically slow, Q3 should benefit from the first full quarter of the Compact Launcher. It should be a barn-burner.

At that point, assuming BYRN gaps-up and runs into the $50s and $60s, IBD and Momo Traders should plow into the stock and help it sprint on a memorable run to ~$100, 12-18 months from now.

IF our numbers are right, next December could be a $60M Q4, with $0.55 in EPS. This would be accelerating triple-digit top-line growth and 267% YoY EPS growth. At that point $2-$3 should be obvious to all, which is when we expect the overshoot to 8x forward sales and a 35x PE multiple on our $3 in EPS estimate… We think this less-lethal story will attain some very lofty levels over time.

Good Weekend to all.