CorMedix Inc. (CRMD) stands to post one of the best ramps you will see in Med-Tech this year. We think there is major upside to BOTH Q1 and FY25 numbers. If we are correct, and Q1 exceeds as we think it will, CorMedix has strong potential to quickly move to the mid-to-high teens.

First, a quick refresher...

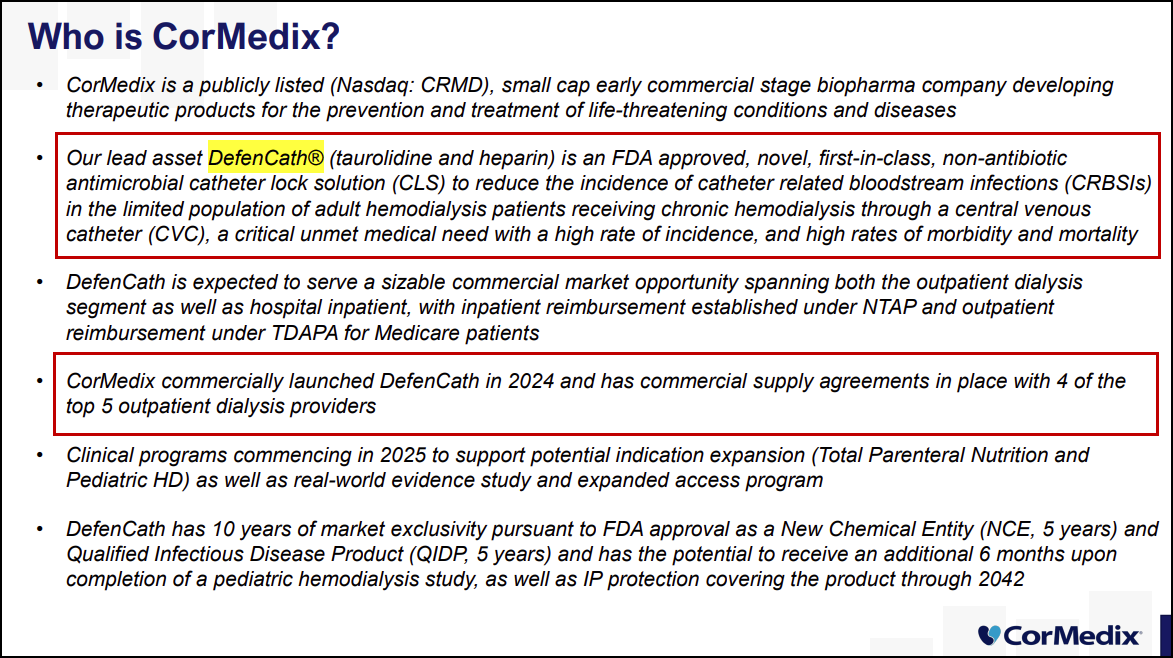

The vast majority of hemodialysis patients are initially treated using a central venous catheter (CVC). The average time on a CVC for a hemodialysis patient is around 220 days.

Unfortunately, with this lengthy CVC treatment time comes an increased incidence of catheter-related bloodstream infections (CRBSI). CRBSIs can occur in 25-33% percent of CVC Hemodialysis Patients and are often resistant to conventional antibiotic treatments. Tragically, patients w CRBSI’s are three times more likely to die within 90 days of infection. In fact, CVCs are responsible for around 70% of access-related bloodstream infections in hemodialysis patients.

With an estimated 19M outpatient dialysis treatments performed in 2024, not counting inpatient settings, there is a growing need for improvements and protection against the risks of CRBSIs for patients receiving hemodialysis.

On Jan 7, CorMedix announced incredibly strong preliminary Q4 numbers, guiding for:

Furthermore, the company also provided an incredibly bullish business update:

CEO Joe Todisco commented:

“CorMedix continues to execute well on our key objectives particularly around our outpatient launch, and I am pleased with the implementation efforts we have seen thus far from key customers in the outpatient segment.

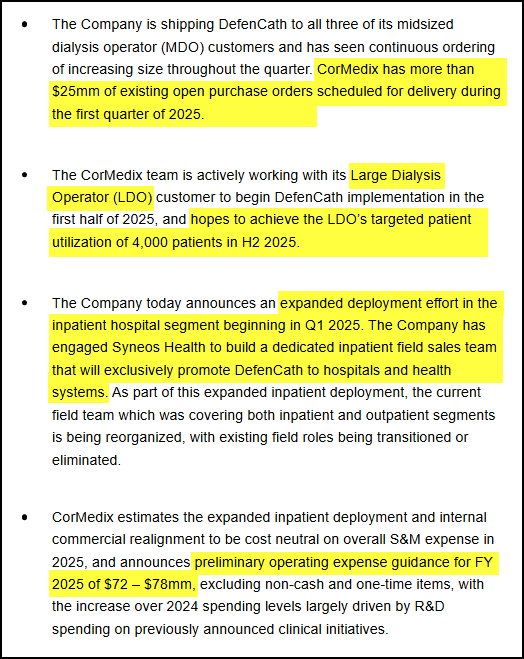

Today's announcement of our agreement for inpatient expansion with Syneos Health reinforces our commitment to grow DefenCath across settings of care.

I believe we begin 2025 in a strong position and look forward to updating investors as we continue to execute over the months ahead."

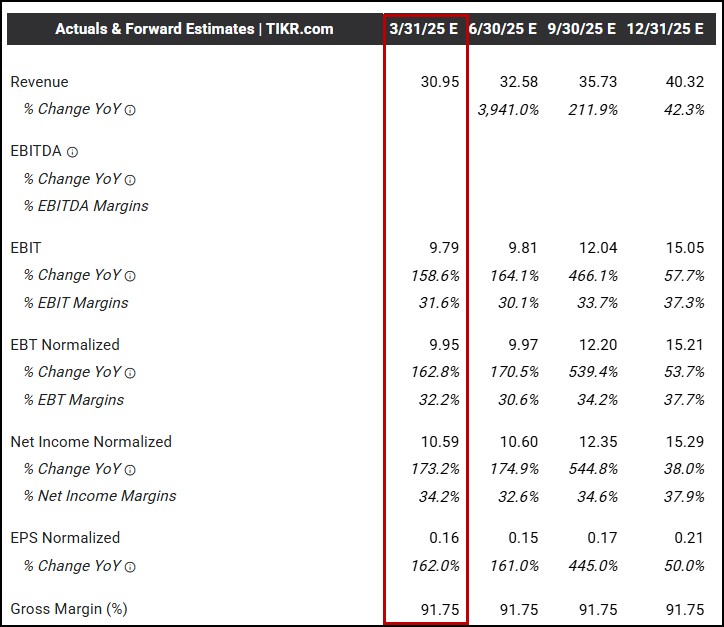

CorMedix stated orders for Q1 were $25M through Jan 7th. This was two and a half months ago. In the update, the company expects its Large Dialysis Operator (LDO) to begin ramping in 1H’25. While we are not sure if it starts in Q1 or Q2, we believe the odds favor CorMedix benefiting from a month or two of the initial ramp in Q1.

Even without ANY contribution in Q1 from its LDO – what will eventually be their No. 1 Customer – we should STILL see significant upside to consensus for the quarter.

Why significant upside?

Well, in the Q4 pre-announce, CorMedix stated they experienced continuous and accelerating orders throughout the quarter. With $25M in orders in hand for the first seven days of the quarter, even if the company ONLY received another $15M in orders since then, at $40M in Q1 Revenue, we could be looking at ~30% of upside. Take a look:

Keep in mind, the $31M in sales for Q4’24 entails around 2k patients from its three mid-size dialysis operators (MDOs). As the LDO begins to ramp in 1H’25, this contract adds 4k new patients with the potential to “achieve the LDO’s targeted patient utilization of 4,000 patients in H2 2025.”

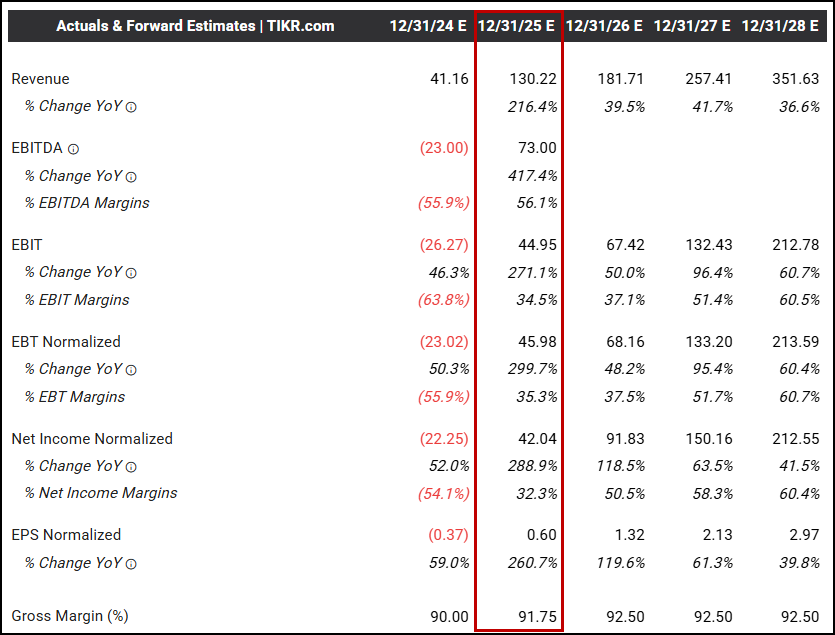

Net-net, we think CorMedix could do $200M+ in revenue for FY25.

Once again, take look at consensus. There’s potential for 50%+ upside to current estimates:

Conservatively, say we are off on our numbers and CorMedix simply does FY26 Estimates in FY25. At $181.71M in revenue and $1.32 in EPS, a 15x PE gets the stock to $19.80. If we are correct and the company posts $200M in revenue and $1.50 in EPS, a 15x PE puts the stock at $22.50.

It is worth mentioning, that SHOULD CorMedix land the final LDO in the space (we attach 25% odds), there is the potential for a move to $30-40 and multi-bagger potential.

CorMedix will announce Q4 Earnings this Tuesday, March 25 – before the market opens.

Given the current bear market/correction environment, we intend to keep our position very small into earnings. In the current backdrop, even good reports are being sold off in some instances, so we believe “Caution is the better part of Valor” as the market grapples with the uncertain climate.

That being said, CorMedix is a Med-Tech company, a space that is currently exhibiting positive relative strength and we believe an impressive Top Tier Inflection is just beginning to occur. Viewed this way, we believe it makes sense to be long into the Q4 report.

If our thesis is correct, we can then add to our position tactically and begin to ride the stock over what promises to be a special year for CRMD.

Stop Loss: We are using $9.85 as our stop on CRMD.

CorMedix has hitched its star to an impressive product in DefenCath, but it IS a one-product company. As such, its fortunes are highly dependent upon CMS reimbursement for the foreseeable future. Should Trump/Congress elect to radically change or reduce benefits for Medicare/Medicaid, this would certainly have sizeable negative ramifications for the company.

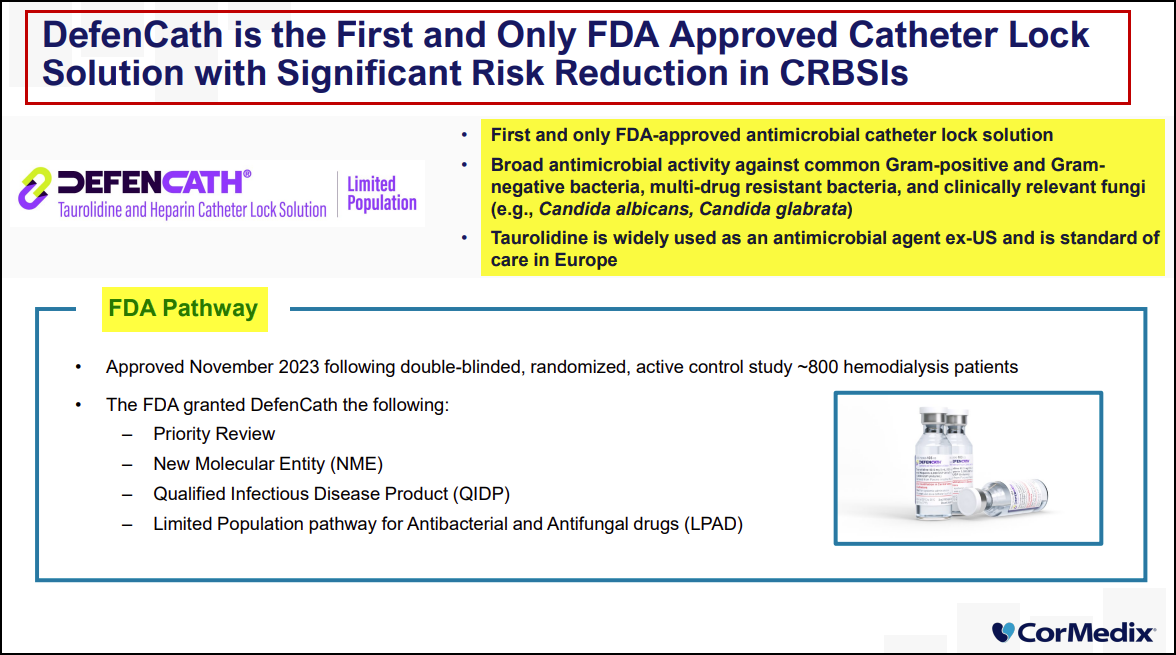

Med-Tech is a highly-competitive space, so there is always the possibility a competitor with deeper pockets emerges. However, given that CorMedix is the first and ONLY FDA-approved catheter-lock solution, we believe a larger competitor would simply buy it outright as an accretive tuck-in.

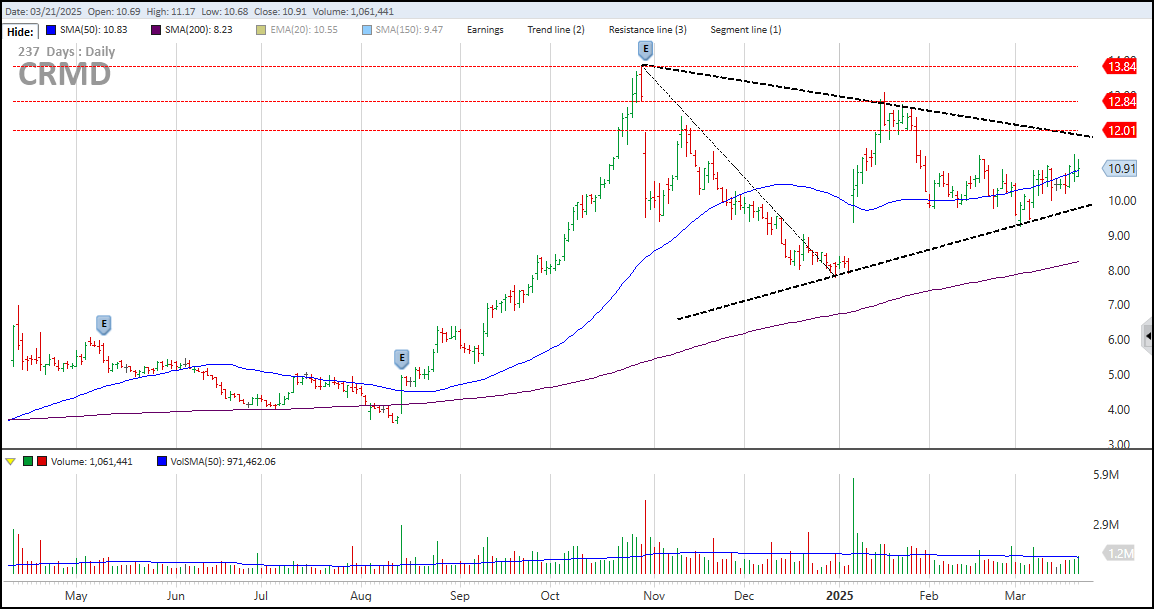

If Management offers upside Q1 guidance on the Q4 Report on Tuesday, we think CRMD will begin a stair-step ascent into the low-teens in the days and weeks after. Take a look at the chart below. The Measured Move on the symmetrical triangle, outlined in black, equates to an $18 price level.

As we state in the title: Nice Risk/Reward Into the Q4 Print!

Conviction Level 8: Due to the overall market backdrop and the CMS potential cut overhang.

-----------------------------------------------------------------------------

Disclosure: We are long CRMD stock and calls. We may change our positioning at a moment’s notice, without notifying you of any such moves.

Disclaimer: All of the information in this piece has been prepped by Inflections Consulting LLC. Readers should know that it would be incorrect to assume that past and future names of interest will be profitable or will not turn into a loss. Inflections Consulting LLC does not and will not assume any liability for any loss that could occur if you invested in such stocks written about.

All the content in these reports have been prepared by Inflections Consulting LLC. We believe our sources to be reliable, but there is no guarantee here. The information in this piece does not constitute either an offer nor a solicitation to buy or sell any of the securities name-dropped in this piece.

All contents are derived from original or published sources believed reliable, but not guaranteed. This report is for the information of Top Tier Inflections members/subscribers, only. Absolutely none of our content may be reproduced in whole or in part without prior written permission from Inflections Consulting LLC. All rights reserved.

In no shape or manner should the views expressed in this piece be considered investment advice. We reserve the right to change our positioning in our CRMD stock and options positions at a moment’s notice without updating you on any such change in opinion and positioning. That may be tomorrow, even before our price target is hit. Facts change, our opinions can change quickly too.

Investors need to consider their investment risk tolerance before investing in the stock market and also before investing in any of the stocks mentioned in this report.