Sometimes the most powerful inflection points present themselves when a secular trend manifests, accelerating adoption of a company's products naturally, and then, suddenly.

Palantir comes immediately to mind. Before ChatGPT hit, it was solely a clandestine provider of intricate and sophisticated intelligence software to mission critical defense and ancillary U.S government agencies and its allies around the world.

With AI proliferating the last two years, after spending billions on accelerated compute, enterprises turned to Palantir's enterprise offerings, ushering in a generational inflection point the last four quarters. In short order, it's enterprise vertical is now poised to become much more consequential than it's Government businesses.

Right place, right time.

After swimming in the desert and being left in the dust by large Cloud Data Warehouse players like Snowflake and Databricks, Domo, Inc. (DOMO) now finds itself in the right place at the right time.

Domo operates a cloud-based modern AI and data products platform that offers a number of interconnecting tools for enterprises which allows data to be aggregated, stored and visualized quickly and seamlessly.

The company's platform is smooth and seamless, allowing an intutitive user experience, native integration capabilities, and reduced total cost of ownership. Domo's software has over 1,000 connector products which helps companies streamline their data into one unified platform.

Unfortunately, lacking the scale and depth of Snowflake's and Databricks Cloud Data Warehouses, Domo hit a brick wall a few years ago, as share gains were stunted and revenue growth turned south:

With the company's subscription model failing, Domo waited too long to pivot, but pivot they did two years ago to a consumption-based model. This was an important first step for Domo to turn its business around.

For those customers that quickly switched to the consumption model, the results and the reviews have been stellar. While it has taken awhile, Domo is nearing the end of its transition to this new paradigm. On its most recent conference call, management informed investors its transition to a consumption model would be 90% complete by the end of this fiscal year.

The timing for the completion of this transition to a consumption-based model is very timely. With over 1,000 software connectors that help to seamlessly aggregrate data, as enterprises look to make more sense of the proliferating data that their models are spewing out, the need to consume more of Domo's software connections will increase materially in the coming years.

The proof is in the pudding. Under the hood, the majority of the most important metrics used to analyze the forward progress of software companies improved dramatically quarter-over-quarter:

- Subscription remaining performance obligations, or RPO, growth accelerated to 24% Y/Y. This was a strong increase from the prior quarter's 14% growth.

- Subscription total contract value, or TCV, was up 69% Y/Y.

- Long-term subscription RPO was up 61% Y/Y. This was up significantly from the previous quarter's growth rate of 38%.

- Net retention was up sequentially for the third consecutive quarter and ARR was also up sequentially. Sales force productivity was up over 60% Y/Y and up for the third consecutive quarter. Gross retention improved to 86% from 85% last quarter.

When you sift through these data points, the underlying momentum is clear - the consumption model is working. More and more companies are making a long-term commitment to Domo's consumption model and its 1,000+ connector products.

Another key reason its consumption model is beginning to hum is due to the Domo platform's ability to help enterprises quickly develop new AI agents. This capability is a key feature set that has helped manifest the inflection we are seeing in its underlying long-term RPO metrics.

This momentum allowed Domo to increase its guidance and to also guide to a nice uplift to its forward guidance:

"Over the past several quarters, we have made significant progress transitioning from cash burn to achieving free cash flow positivity and expanding our operating margin. As we look ahead, we expect to exit this year at 5% billings growth and 5% operating margin, and we anticipate exiting FY '27 at 10% billings growth and 10% operating margin.

These achievements demonstrate not only our strengthening fundamentals, but also substantial progress on our Rule of 40 profile. This shows that our model is working and positions us for sustained profitable growth going forward."

After seeing its stock languish since the end of COVID - cratering 90%+ peak-to-trough - Domo's stock finally inflected after its most recent quarter. We think this is just the beginning of a strong multi-quarter/multi-year move:

Importantly, Domo's valuation is still quite attractive at current levels.

Currently, it trades for 1.8x forward consensus. As its business inflects in the coming quarters and next fiscal year, Domo's valuation will naturally increase as new Buy Side investors warm up to the story. The Sell Side will take longer to warm up to the name. On its Q1 call, there were only three analysts present. Remember, allthese guys were burned badly in the name from late-2022 until now. So, its not surprising to see the Sell Side less-than-enthusiastic about the name.

As an aside, the Cantor Fitzgerald analyst is the ace on the stock. He bottom ticked the name earlier this year with an Overweight rating when DOMO was languishing below $10.

He then moved his PT up to $17 recently. Importantly, it does not take much to get to his target. Even a modest re-rating to a 2.5x Price-to-Sales multiple on our forward numbers gets us a near-double from current levels to $22-$24.

Not only is Domo super cheap on a Price-to-Sales basis - note INFA was recently taken out for 5x sales (even though its growth has been stunted for years) - the company also has a strategic asset with its $1B+ in NOLS. On an after-tax-basis, this works out to $250M+ of value for an acquirer. We therefore think there is wonderful assymetry in a stock that has only just begun to rise from its deathbed.

Additionally, the share structure is quite tight - only ~40M shares outstanding. It will not take much additional new institutional ownership to get the stock to head toward $22-$24 the next 3-4 quarters.

To wit, institutional ownership in DOMO has declined consecutively for 8 straight quarters. It is ripe for new blood and we are already seeing that each day, with its stock trading nearly 1M shares a day vs 400k a day, prior to its inflection:

Turning back to the numbers...

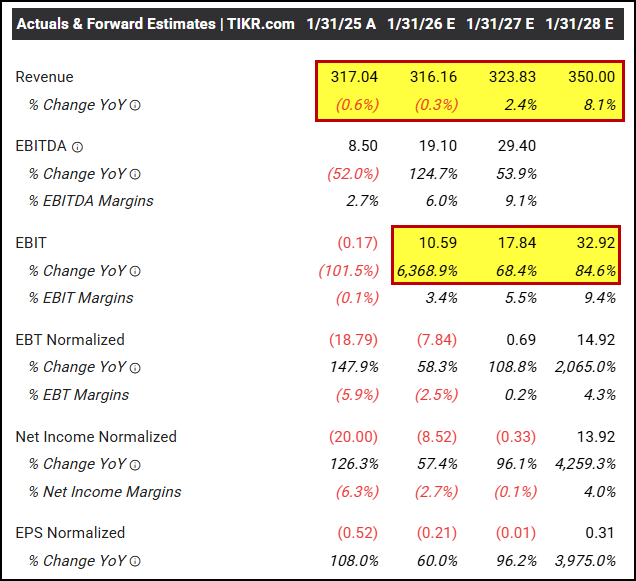

With so many important metrics turning up, we believe forward consensus is woefully low. We think Domo will exit this year at a 10%+ growth rate and exit FY26 at a 20-25% top-line growth rate. Our numbers are WELL ABOVE CONSENSUS:

As noted in the highlights above, Domo is finally poised to see bottom-line leverage in its model inflect. With gross margins clocking in at ~81% currently, as its retention metrics continue to improve, Domo's gross margins should also inflect to the 85% zone.

We see $375-$390M in revenues for FY27 and $450M in revenues for FY28. If we are correct, as these higher levels of revenues manifest, we will see EBITDA inflect well above consensus. We think EBITDA for FY27 and FY28 can double current consensus.

Why are we so optimistic and forecasting numbers so much higher than consensus?

DOMO's partnership with Snowflake is at a powerful inflection point moment.

A year ago, after begining its consumption transition journey, Domo smartly decided to partner up with all the big players in the Cloud space. Snowflake, Databricks, Google Cloud, Oracle, IBM have all partnered with them. Thus far, Snowflake has been the only partner to lean into its Domo partnership in a significant way.

While it has taken a few quarters for this relationship to bloom, bloom it has.

In its most recent conference call with investors, Domo noted that its Top-of-the-Funnel PARTNER pipeline - the ready-to-convert-to-revenue portion of the pipeline - increased 200% sequentially. Moreover, its win rates are significantly higher - 3-4x higher - than the win rates its internal sales force has seen.

During a fireside chat with Cowen last week, Domo noted that Snowflake is now bringing them in to pitch new biz and has begun integrating Domo in with its OWN expansion sales teams. This opens up Snowflake's entrenched customer base for DOMO to sell to as well - a major catalyst that will help to accelerate growth to double-digits in the coming quarters.

Snowflake partnership w Domo is enabling it to compete better vs Microsoft and Tableau. Previously CIOs were not aware of Domo's presence in the marketplace. Now, with Snowflake's blessing of Domo's data platform, it has created wonderful synergies for the sales process.

This early traction is significant as Snowflake is Domo's first partner to really lean into cross-selling with the Domo plaftorm. Databricks, Google, Oracle and IBM partnerships are up next.

In and of itself, with the Snowflake partnership moving into overdrive - Snowflake would NOT be opening its expansion sales force team to Domo if it did not see BIG UPSIDE - we think the relationship is enough to spur an inflection upside to current consensus that we previously outlined.

This is supported by the strong momentum Snowflake is currently seeing in its own AI initiatives.

This morning, UBS upgraded SNOW to a $265 PT, referencing increasing win rates and burgeoning strength in its new AI product lines. While Microsoft will clearly be one of the biggest winners in AI, the inflection in demand for data is so strong and accelerating so quickly, enterprises are willing to pay SNOW's premium prices. They are willing to pay because Snowflake & Domo are able to help them ingest, visualize and make sense of the incredible amount of datasets that are being generated from Generative AI.

This trend will only increase further in the coming years, as AI Inferencing has only just begun to go into overdrive. This will be a multi-year growth curve for companies levered to data.

Importantly, we see nearly 100% upside to DOMO in the next 3-4 quarters just from the momentum from its SNOWFLAKE partnership.

Databricks is up next.

In July, Domo will be finishing a second iteration of their updated cross-selling platform with Databricks. Domo is also hiring additional sales reps to support the Databricks roll out. By year-end, Databricks and Domo's partnership could be humming. While there is risk that Databricks does not scale to similar levels to Snowflake, SHOULD this relationship become needle-moving, the potential for a 6-8 quarter multi-bagger move in DOMO is very tangible.

Some quick math:

If Domo were to accelerate to a 30% top-line growth run-rate two years out and Operating Margins inflect to 25-30%, its multiple could re-rate to 4-5x forward sales.

4x $450M revenue in FY28 would get us to a $1.8B market cap. That is ~250% upside from current levels.

Again, we are NOT counting on Databricks for our base case: a near-doubling in DOMO over the next 3-4 quarters.

While forward numbers have yet to reflect the underlying momentum being generated under the hood, we think it is just a matter of time before Domo raises its guidance again. In particular, we think the strength in the current top-of-the-funnel pipeline will translate into accelerating top-line and bottom-line momentum in the2H of the year. So, there is a lot to look forward to.

Considering the cheapness of the stock and how it has been left for dead by both the Sell Side and the Buy Side, as this expected inflection manifests, we think the stock can stage a powerful move in the back half of this year.

Similar to PLTR a year ago, we think DOMO is at the right place and right time to see a strong inflection in its stock materialize.

Of course, there are risks to our thesis.

Macro is front and center. There is the chance Snowflake chooses NOT to further its relationship with Domo, especially if the burgeoning Databricks partnership takes off for the company. Then, there is the risk that Snowflake is the ONLY partner that ever materializes for Domo and Databricks and the other partnerships go nowhere.

Taking this into account, with Domo's strong data-connecting aggregator capabilities helping Snowflake improve its win rates vs Microsoft, we think the odds are very low Snowflake suddenly loses interest anytime soon.

With minimal downside to its shares and strong upside potential, we remain buyers of DOMO at current levels and on dips to the $12s.

Stop Loss: Our conviction is a 10 here, thus we are implementing a Time Stop over the next few quarters.

We view our position in DOMO as a long-term hold vs a short-term trade idea inflection.

----------------------------------------------------------------------------

Disclosure: We are long DOMO stock and calls for the capital we oversee. We may change our positioning at a moment’s notice, without notifying you of any such moves.

Disclaimer: All of the information in this piece has been prepped by Inflections Consulting LLC. Readers should know that it would be incorrect to assume that past and future names of interest will be profitable or will not turn into a loss. Inflections Consulting LLC does not and will not assume any liability for any loss that could occur if you invested in such stocks written about.

All the content in these reports have been prepared by Inflections Consulting LLC. We believe our sources to be reliable, but there is no guarantee here. The information in this piece does not constitute either an offer nor a solicitation to buy or sell any of the securities name-dropped in this piece.

All contents are derived from original or published sources believed reliable, but not guaranteed. This report is for the information of Top Tier Inflections members/subscribers, only. Absolutely none of our content may be reproduced in whole or in part without prior written permission from Inflections Consulting LLC. All rights reserved.

In no shape or manner should the views expressed in this piece be considered investment advice. We reserve the right to change our positioning in our DOMO stock and options positions at a moment’s notice without updating you on any such change in opinion and positioning. That may be tomorrow, even before our price target is hit. Facts change, our opinions can change quickly too.

Investors need to consider their investment risk tolerance before investing in the stock market and also before investing in any of the stocks mentioned in this report.