Trading for a ~$600M market cap near $15, Domo, Inc. (DOMO) remains significantly undervalued.

At current levels, we see minimal downside along with 75% odds for the stock to double to $30 the next nine to twelve months and then triple+ to $50 the next 18 months.

It's very hard to find the type of value we see in DOMO in the current backdrop. So, we want to be fully transparent: we own a sizeable position in the name; DOMO has become our #1 position for the accounts we oversee, by a wide margin. Let's dig in.

First, why is there minimal downside? Well, a few reasons, including:

With $2.5B of NOLS - which translates into a Total NOL CF Savings of ~$335M to an acquirer (more than half its market cap) - along with $800M invested into its data platform since its formation, DOMO offers a ton of value from both an economic and technology perspective to a potential acquirer. To wit, at the D.A. Davidson conference three weeks ago, DOMO's CEO stated he would begin talking to anyone who was willing to start the bidding for a takeout at 4X sales.

Fundamentally, with growth poised to re-accelerate in a meaningul manner the next two quarters, forward #s are woefully too low, particularly for Fiscal 2027. DOMO trades for ONLY 1.6X our Fiscal 2027 revenue estimates of $375M, which are ~15%ish above consensus.

Considering DOMO sits in the next sweet spot for AI - the need for data will rise exponentially in the coming years as the world moves closer to Agentic AI -we think its shares have minimal downside trading at such a lowly forward Price-to-Sales. Look no further than the recent INFA take-out for 4.6X sales. Were DOMO to be scooped up for a similar multiple vs. our current $375M Fiscal 2027 estimates, this would equate to a takeout at $42.

Current comps trade for 3.4X-4.6X sales. Let's use 3.4X sales X our $375M in Fiscal 2027 #s. This gets us to $30 in 12 months. So numerous ways to get a double, on its own, or via a takeout.

Importantly, there are three catalysts which we think will organically catalyze a double the next 3-4 quarters. These include:

1. The transition from a subscription model to a consumption model will be 90% complete by the end of this fiscal year. As AI agents proliferate (In Barrons this weekend, legendary growth/tech investor Laffont from Coatue noted a dramatic surge in usage of AI chatbots in Q2) and Agentic AI is reached in the next 12-24 months - most likely, by Open AI or META after its recent coup in bringing onboard SCALE AI's CEO into the company, - DOMO's customers will utilize more advanced feature sets from DOMO's full stack data platform.

As longer and larger contracts are signed by companies looking to utilize DOMO's vast resources, consumption will increase materially as we move into 2027, and beyond, catalyzing a turn upwards in its base business.

2. DOMO pivoted aggressively to integrating a partner-centric sales approach 12 months ago. The fruits of these efforts will be realized in the next two quarters, with 20%-25% of the hundreds of deals in the pipeline with its main partner, Snowflake, along with various other Systems Integrators and Cloud Data Warehouse Partners like Databricks, Oracle, IBM and Google - yes, DOMO is the white label partner to all these big guys - finally closing.

Considering its partner deals are larger, stickier, move more quickly and have a 20% better close rate than its direct sales force, as these deals get closed, it will re-ignite growth and catalyze a stair stepped re-rating in DOMO the next 3-4 quarters.

3. Currently, there are only two analysts who see what we see - a new DOMO poised to achieve record levels of performance and PROFITABILITY, which will spearhead the company's most pivotal inflection point since coming public.

We foresee an exceptional beat and raise in the November print. This should be the quarter that gets DOMO to begin a parabolic move into year-end and the first half of 2026. You see, what the Street is missing is the incredible leverage forthcoming in DOMO's model as revenues inflect and its growth rate reignites.

When the rest of the Street wakes up and smells the coffee as the stock moves toward and then into the $20s, this will bring in an entirely new shareholder base into the stock. As value investors pass the baton to growth investors, our long-term roadmap to $50 will come into view in 12-18 months. More on these respective catalysts shortly.

For now though, let's go in reverse and dive into what exactly DOMO does, what happened after their IPO, what led to the collapse in the stock and why we think now is the time to, as DOMO's CEO stated at D.A. Davidson 3 weeks ago, "BACK UP THE TRUCK ON THE SHARES."

DOMO has created a world class enterprise-grade data and AI analytics platform that helps companies rapidly ingest data and make quick sense of it on Day 1.

DOMO's product portfolio is vast and robust. Its capabilities include:

- Business Intelligence

- Data Warehousing

- Data Discovery

- Analytics

- Collaboration

- Dashboarding

- Visualization

- Security and Corporate Governance

DOMO's journey started in 2012. From the very beginning, DOMO had high aspirations. DOMO's CEO Josh James is a serial entrepeneur who sold his first company called Omniture to Adobe in 2009 for $1.8B.

When he started DOMO in 2012, he wanted to create a full stack data platform. As such, he stacked many disparate and valuable software tools together. Therefore, we think it is accurate to think of DOMO as many start-ups rolled into one company, a key differentiator that allowed the company to scale to impressive heights from 2017-2023.

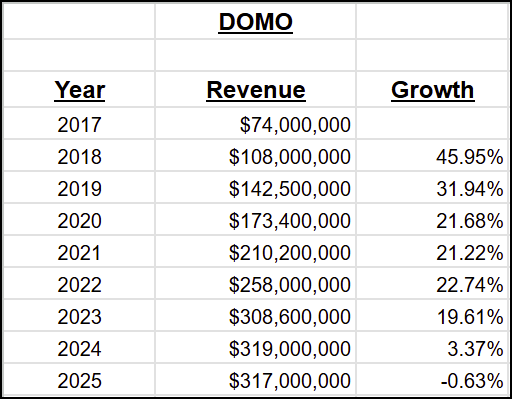

Yes, 8 years ago, DOMO was a true disruptor, quadrupling its revenues in a 7-year period:

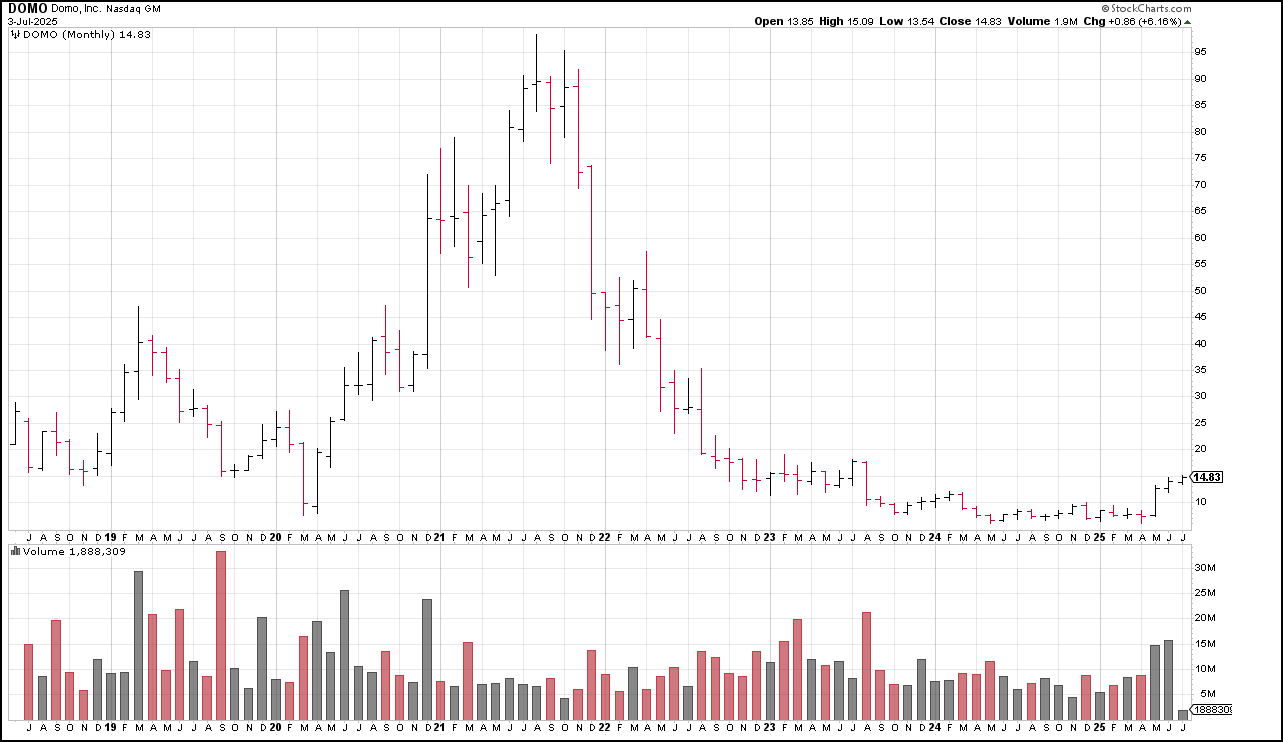

Its stock did quite well during COVID. Until it didn't:

DOMO hit a brick wall in Fiscal 2024 and 2025. During this time, DOMO had a hard time getting in front of C.I.O.'s as much larger Cloud Data Warehouse companies - particularly Snowflake and Databricks - boxed DOMO out from these important gatekeepers. This caused retention to falter and forced the company to make two important pivots.

The first was to switch from a seat-based subscription model to a consumption model. The second was to accept that the only way DOMO would transform itself to entirely new levels was by partnering with the Cloud Data Warehouse companies by doing what they do best - ingesting data the fastest among data integration companies on the market.

To say it has been a journey is an understatement.

After growing sequentially EVERY QUARTER for almost 5 years after its IPO, the company hit a brick wall 8 quarters ago - revenues have essentially been flat since then:

In the middle of 2023, sensing trouble in its model - in our view, management got caught with their pants down by not getting ahead of the competitive threat posed by both Snowflake and Databricks - Domo switched from a subscription based model to a consumption one.

With a subscription model, a company will subscribe to a certain number of seats for anywhere from 1-5 years, thereby giving users access to specific software applications. This is not the best model for those companies who cannot predict the data usage needed in the future.

Because of the long-term nature of the subscription contracts, DOMO has made the transition to its consumption-based model in increments. After ending last quarter with nearly 75% of its business switched to consumption, DOMO expects the percentage of revenues coming from consumption to approach 90% by the end of FY26.

We think the timing is perfect with the advent of AI Agent already here and Agentic AI quickly approaching.

Think about it. In a consumption model, DOMO grants access to its entire platform to an entire company's workforce on Day 1 the enterpise-wide license goes into effect. With a prospective customer allowed to "test the goods out" before signing up for the license, it allows those companies that sign up for the freemium model to hit the ground running.

As customers utilize advanced data sets in greater volumes, consumption expands, leading to a positive flywheel effect, one in which higher consumption leads to gross and net retention rates increasing, which then increases revenue growth, organically.

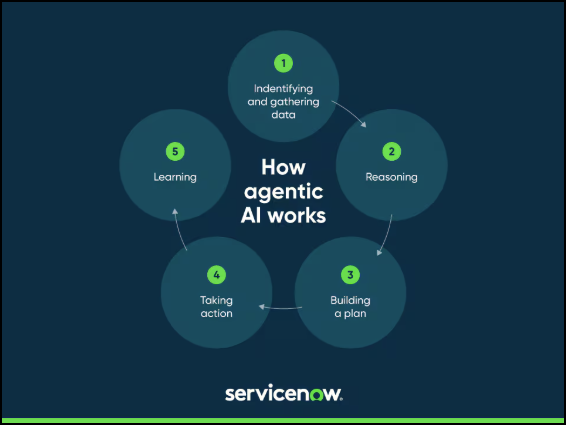

The timing could not be more optimal with the advent of Agentic AI Before we continue with our deep dive on DOMO's other catalysts that will re-ignite growth for the company, we thought it very important to spend some time on expanding further on Agentic AI and why DOMO is in the right place at the right time.

Here is some great info from a wonderful article from Techtarget earlier this year:

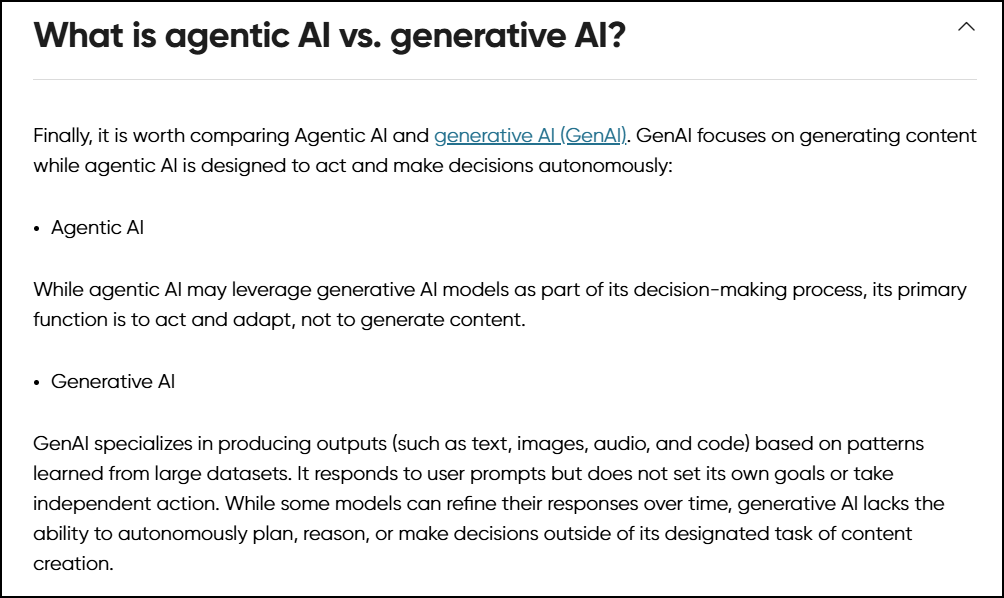

"The term Agentic AI, or AI Agents, refers to AI systems capable of independent decision-making and autonomous behavior. These systems can reason, plan and perform actions, adapting in real time to achieve specific goals. Unlike traditional automation tools that follow predetermined pathways, Agentic AI doesn't rely on a fixed set of instructions. Instead, it uses learned patterns and relationships to determine the best approach to achieving an objective.

To do this, Agentic AI breaks down a larger main objective into smaller subtasks, said Thadeous Goodwyn, director of generative AI at Booz Allen Hamilton. These subtasks are then delegated to more specialized AI models, often using more traditional, narrow AI models designed for specific actions.

The decisions and actions of these component AI systems ultimately enable the AI agent to achieve its primary objective. And this capability is quickly maturing, according to Goodwyn.

The idea of agents is not new; we've been working on this for a while," he said. "But the reason why it's getting so much attention now is because large language models and generative AI accelerated some of the characteristics Agentic AI needs to be successful."

According to "Deloitte's State of Generative AI in the Enterprise" report, Agentic AI is one of the most closely watched areas in AI development. Respondents described Agentic AI (52%) and multi-agent systems (45%) -- a more complex variant of Agentic AI -- as the two most interesting areas in AI today."

Salesforce, Inc. (CRM) Q1 Call

"We are in a moment in time where every company is coming to us saying, how do I go forward and how do I deliver this incredible agentic revolution."

NVidia, Inc. (NVDA) Q1 Call

"The transition from Generative to Agentic AI, AI capable of receiving, reasoning, planning and acting will transform every industry, every company and country.

We envision Agentic AI agents as a new digital workforce capable of handling tasks ranging from customer service to complex decision-making processes. I think it is fairly clear now that AI is going through an exponential growth, and reasoning AI really busted through...

I think a lot of people are crossing that barrier and realizing how incredibly effective agentic AI is and reasoning AI is."

Enterprise AI

"Much more than generative AI, agentic AI is game-changing. Agents can understand ambiguous and rather implicit instructions and are able to problem solve and use tools and have memory and so on."

Harvard Business Review (Dec'24)

“You can define Agentic AI with one word: proactiveness... While previous AI assistants were rules-based and had limited ability to act independently, Agentic AI will be empowered to do more on our behalf."

Bank of America (June’25)

“Agentic functionality could be the defining catalyst for AI monetization, as agents have the potential to unlock sustainable, measurable and material workforce productivity improvements."

BofA believes Agentic AI spending could soar to $155B by 2030, 3x more than current consensus.

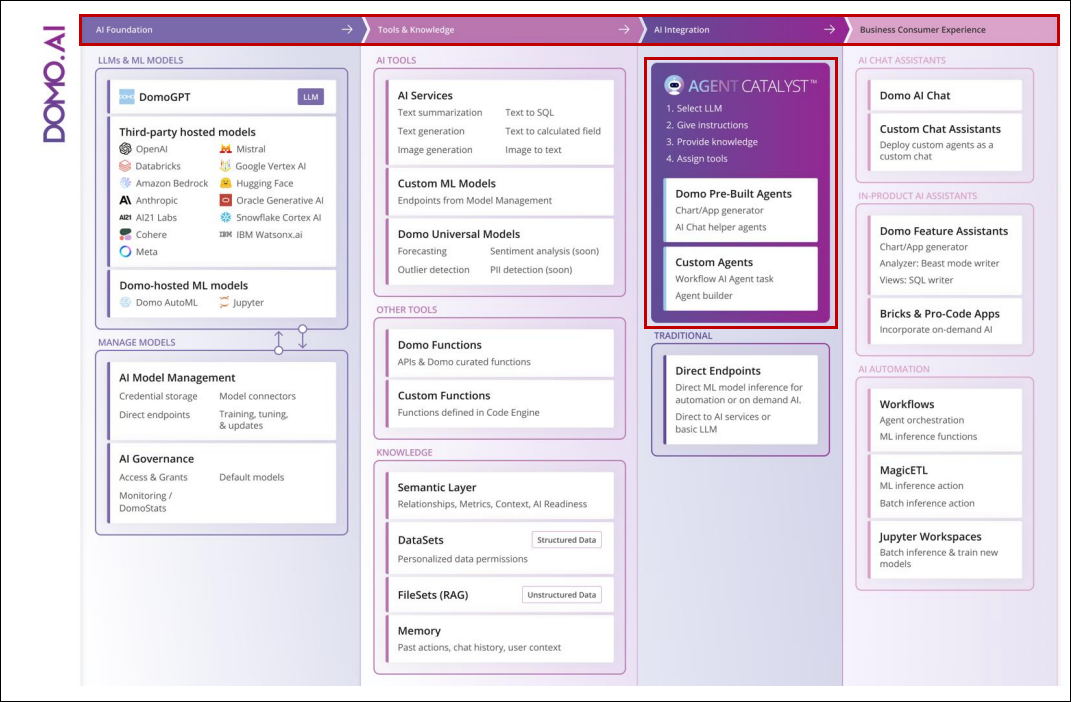

Because DOMO had the vision to create a full software stack, it has allowed them to quickly move to the center of important conversations with customers and new logos about how to integrate AI into their enterprises.

DOMO moved very quickly in the last 18 months, quickly creating a multitude of new AI capabilities in its platform, including its Agent Catalyst product. AI Catalyst should be a significant springboard that will spur consumption utilization and usher in a renewed and sustainable period of double-digit growth as we move into Fiscal 2027:

We believe Cantor Fitzgerald's Yi Lee is an outstanding analyst who has done excellent work on DOMO. He bottom ticked the stock, initiating coverage in early January, thereby bringing a fresh perspective to the name.

Currently, Cantor has a $17 PT on the name. Although JPM is ahead of Cantor with a $20 PT, we believe that Mr. Lee is the ax on the stock and is the one to pay attention to. To that end, we expect Lee to move his PT into the $20s after the next earnings report by DOMO.

In his initiation piece, this snippet summarizes perfectly why DOMO's consumption model will be catalyzed by AI:

On its recent earnings call, DOMO's CEO emphasized how its full stack and governance capabilities have positioned the company to excel in this next phase of AI:

In summary, DOMO's ability to quickly access and then curate the data needed for AI, to quickly integrate models to gain further insights and to then deliver these insights to the enterprise will allow the company to offer enhanced R.O.I.'s on their customer's AI investments. As customers lean into DOMO's offerings, particularly its ability to quickly create AI agents and AI driven workflows, consumption will naturally increase.

And the timing appears optimal. Last year, Palantir Technologies, Inc. (PLTR) was one of our top picks as the data stack they developed through the work with worldwide governments served as a perfect catalyst for enterprise adoption for companies looking to make sense of the data being gleaned from all the GPUs they purchased.

Palantir's success has amplified the focus enterprises are now placing on the data layer.

With corporations coming to understand how harnessing their data more quickly and seamlessly will drive AI application performance, we have only recently entered a robust and extensive investment cycle in the data layer that will last for the next 2-4 years.

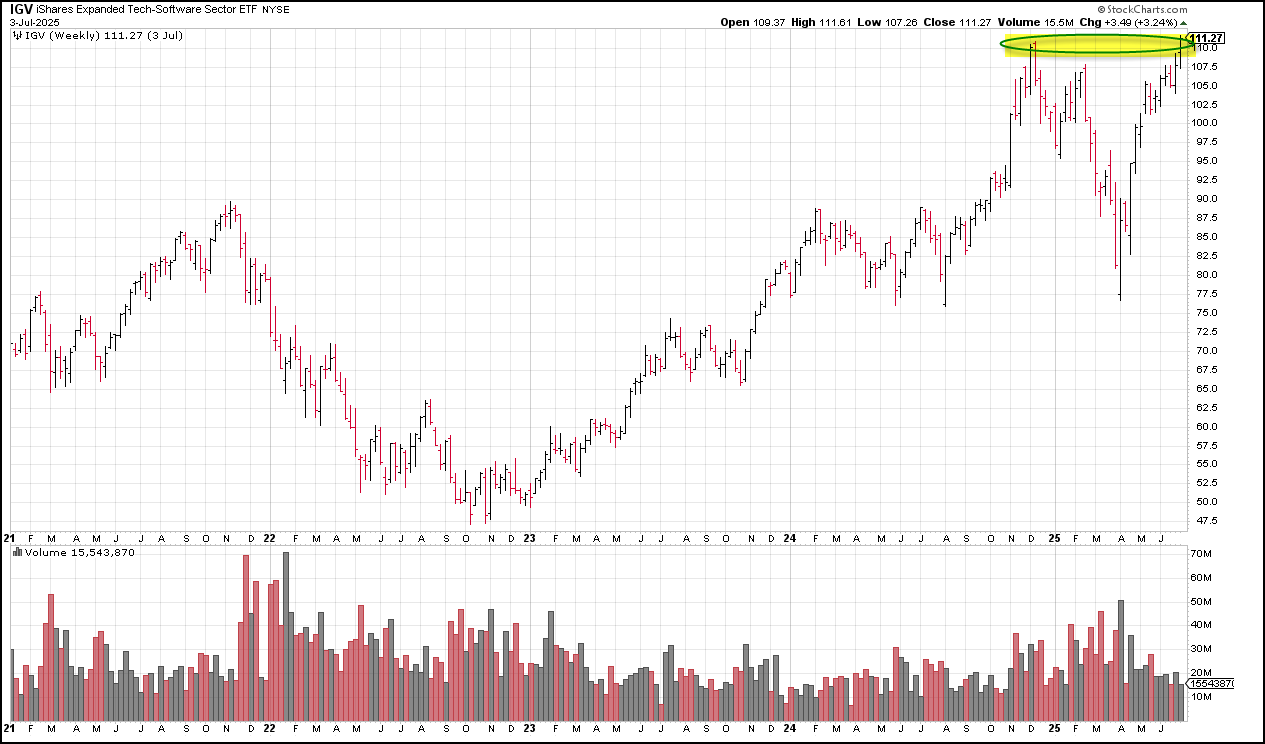

To spur outperformance in your portfolio the second half of this year, investors will need to be levered to the software and data space. This is why IGV recently made ATH's and why DOMO is our #1 position:

Go where the puck is going, not to where it has been – is a key part of our process, one which has helped us identify and maximize multiple multi-baggers in our career. We see the same trend manifesting here. So for DOMO, it’s the right place, right time. In many ways, they were built for this moment.

And, similarly, right place, right time for them to partner with the CDW's as well, which for us, is the energizing catalyst for DOMO in the next 2-6 quarters.

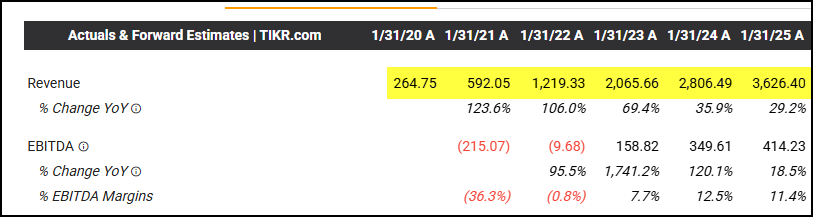

Between 2020 and 2025, Snowflake's revenues will have grown 13X - cra, cra:

Source: TIKR.com

From 2025 to 2030, SNOW is expected to post a near tripling in revenues:

This is what true disruption looks like, massive revenue growth, at scale. SNOW has it. And DOMO is now tied at the hip with SNOW in a major way.

A year ago, DOMO partnered with Snowflake, Databricks, Oracle, IBM and Google. Unsurprisingly, it has taken awhile for most of these partnerships to show any headway. Snowflake however, leaned in, seeing the value DOMO brought to them immediately.

Here is how DOMO's CEO explains what they bring to Snowflake:

"And since we now have this partner motion, we're able to go and really help those customers mine their customer bases and help them generate revenue. So it really is a win-win because we're making it faster and quicker for them to be able to go to market, make their customers happier because they're providing them data. And it's in line with the other information that and the other software that they're selling to them.

And then we're helping them improve and increase their revenue by selling this analytics add-on. So they're able to offset the cost they were paying for Domo in the first place. And in some cases make substantial revenue and profit margin out of it. And then at the same time out the back end comes good deals for us. In some cases, multi-million dollar deals."

With Snowflake utilizing DOMO as their preferred Data Vendor, DOMO's ease of use and unparalleled ability to rapidly ingest, store, prepare and visualize, and then make sense of these enormous datasets has resonated strongly with SNOW's sales force, helping them increase their win rates vs. Microsoft.

DOMO started out slowly with Snowflake, but the partnership is now inflecting in a big way. We think the current Fiscal Q2 quarter will be the first quarter where SNOW and these other CDW and Systems Integrator partnerships (about 90 in total, actually, although 75% of wins are coming from SNOW) will move the needle for DOMO.

From there, we expect it to become an exponential tailwind, one that will significantly re-ignite DOMO's billings, RPO metrics, and then its revenue growth rates, first to mid-to-high single-digits exiting this year, and then, to a 25%+ revenue growth rate exiting FY27.

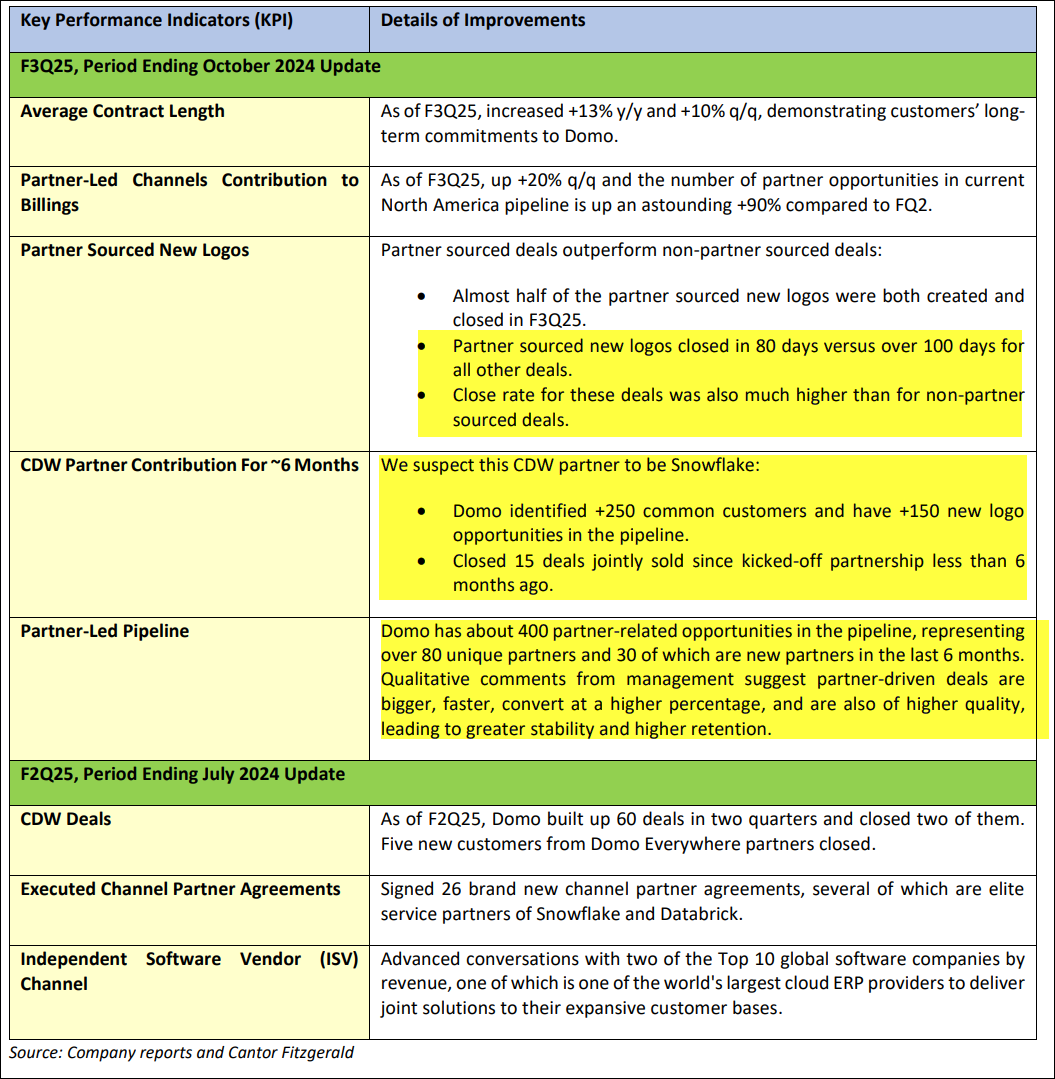

In its initiation report earlier this year, Cantor provided a summary of where the company was at that point in its sales partnership with SNOW and the other CDWs. Again, excellent work by Cantor here:

So, 400 deals in the pipeline as of Oct. 2024. Fast forward to May’25 and the metrics have gotten even juicier:

- The top of the funnel sales leads on the cusp of being converted increased 200% sequentially quarter-over-quarter.

Again, this is significant as these partner deals are bigger and have a higher percentage of converting, relative to their direct salesforce deals. Here is an illustration of how needle moving these deals can potentially be for DOMO in the near and intermediate term:

In the last month, things seem to be heating up even more intensely.

When DOMO presented at Cowen early in June, the CFO stated that SNOW was opening up its Expansion Sales Force Team to DOMO. This is after SNOW allocated 20 new logo sales teams to DOMO in the first few quarters. Clearly, SNOW is leaning in, which means deals are closing and win rates vs. MSFT are improving. Otherwise, why lean into DOMO?

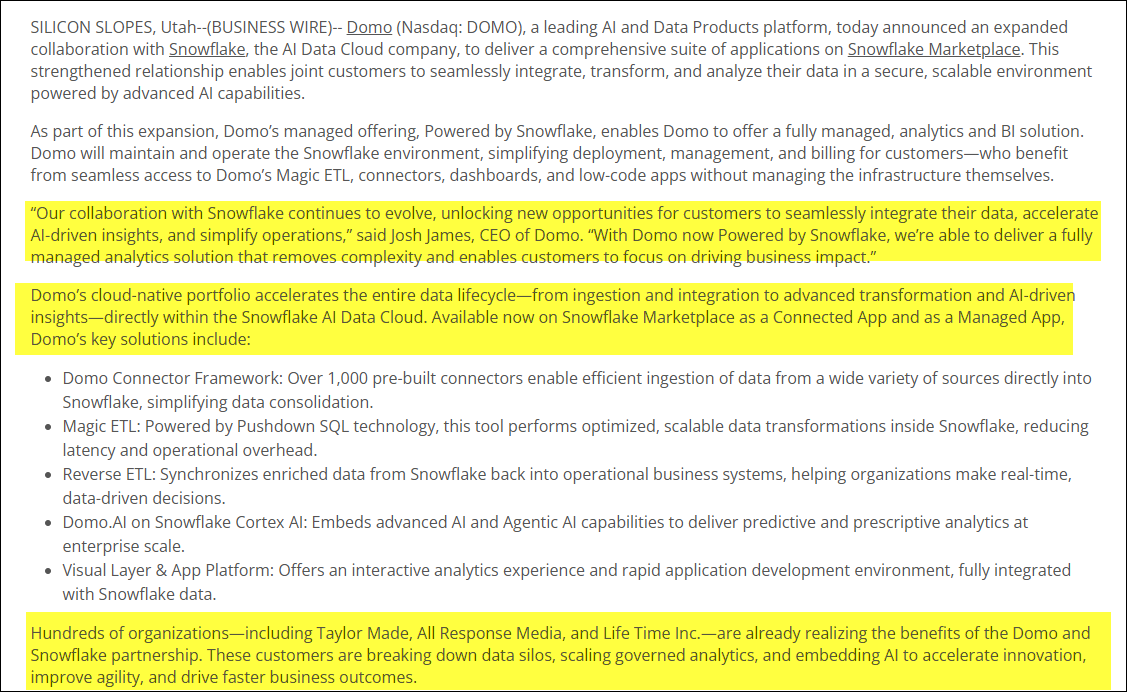

This is what we thought when we saw the recent PR, one in which DOMO trumpets how they are now essentially being white labeled in to run parts of SNOW's workflows for them:

At DA Davidson, DOMO's CEO came out and stated that it was still very early days for its partnership with Snowflake, explicitly stating they were only 10% penetrated with SNOW. And yet, with it being only 10% saturated with SNOW, DOMO's CEO has stated he expects the SNOW relationship to increase its new logos by 50-100% NEXT FISCAL YEAR. Think about that. That's just SNOW at 10% saturation.

In the last few years, DOMO's new logo growth has been non-existent. So, in of itself, as these new logo wins happen, DOMO is set to see revenues inflect meaningfully. And, remember, as outlined above, average deal size with partners is expected to be $1M, as these are significantly larger companies SNOW is engaging with, relative to the types of companies that make up half of DOMO's current customer base.

Let's assume they get 75 deals through the finished line with SNOW next fiscal year and 150 the year after. At $1M a clip, that gets $75M of incremental revenue just from SNOW in Fiscal 2027 and $150M in incremental revenue from SNOW in Fiscal 2028.

Our 2027 revenue estimates of $375M and our 2028 revenue estimates of $469M suddenly look very achievable when viewed from this prism.

At the recent Snowflake AI conference, DOMO had a big presence there with them. Its three booths drew in over 850 visitors.

Looking ahead, on July 15th, DOMO will be releasing its next iteration of its partner integration platform. This is a big catalyst, as it will make SNOW's salesforce more efficient in integrating DOMO into their sales calls with existing and new customers.

And, while very nascent, DOMO still believes relationships with the likes of Databricks will eventually begin to purr. We will see. Time will tell.

Turning to Databricks, we are not expecting much from them in the near-term. Yes, DOMO did have one sales rep at Databricks’ recent conference who generated 20 hot leads in one day. But we get the sense Databricks is moving slowly. We are not sure if this partnership ever gets humming, but if it does, wow, DOMO's revenue growth rate could/would quickly re-ignite to not just 25% top-line growth in FY28, but to 40-60% top-line growth.

Same goes for Oracle, IBM and Google Cloud. We are not modeling anything from them.

So, a lot to look forward to in the next 2-6 quarters just from Snowflake.

In addition to top-line growth inflecting, we also believe DOMO will see significant leverage in its model as this revenue inflection manifests.

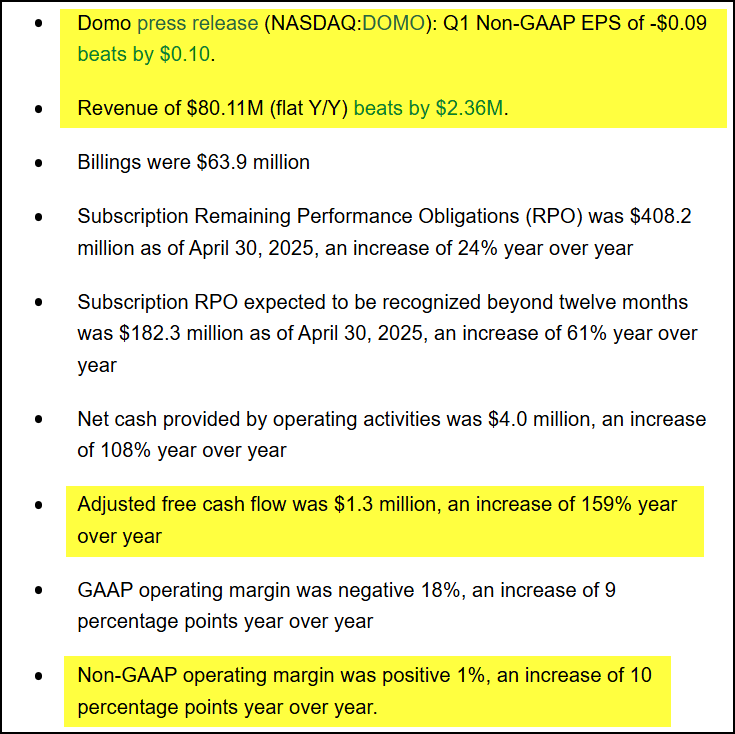

Q1 was the first quarter we began to see some leverage manifest in the model.

On a ~3% beat in revenues, EPS bested estimates strongly and Q1 was also the first time DOMO achieved a positive non-GAAP margin in any Q1 in its history:

Some additional metrics of note:

Josh James, Founder and CEO, emphasized:

“We demonstrated substantial operating leverage in the business showing that our model is truly working. Once again, we exceeded guidance on billings, revenue, and non-GAAP EPS, and generated positive adjusted free cash flow. Notably, this marks the first time we've achieved a positive operating margin in a Q1."

James reported accelerated RPO growth, a dramatic increase in sales efficiency, longer contracts, and momentum in the consumption-based pricing model, stating:

“Subscription remaining performance obligations, or RPO, growth accelerated to 24% year-over-year. Subscription total contract value, or TCV, was up 69% year-over-year. Long-term subscription RPO was up 61% year-over-year… salesforce productivity was up over 60% year-over-year. Gross retention improved to 86% from 85% last quarter."

Importantly, DOMO went out of their way to raise their long-term guidance as well:

"Over the past several quarters, we have made significant progress in transitioning from cash burn to achieving free cash flow positivity and expanding our operating margin. As we look ahead, we expect to exit this year at 5% billings growth and 5% operating margin, and we anticipate exiting FY '27 at 10% billings growth and 10% operating margin.

These achievements demonstrate not only our strengthening fundamentals, but also substantial progress on our Rule of 40 profile. This shows that our model is working and positions us for sustained profitable growth going forward."

Looking ahead, at DA Davidson in mid-June, DOMO's CEO explicitly stated there will be significant leverage in the model that manifests as the company achieves its next $100M of ARR. That statement is a big one, as first, it shows his confidence that ARR is poised to, in time, inflect by another $100M and, secondly, that when it does, the flow through margin will be significant. How significant?

Well, considering DOMO has 81.5% GM's and has not needed to hire many new sales reps or engineering staff, as existing roles were simply transferred from the Direct model to the partner model, on the next $100M of revenues, we think the flow through margins should be north of 60%. Perhaps 70%+. Hmmmm, the last time we saw such flow through margins was APP when we recommended it last year in the mid-$50s. Just saying. This inflection point is going to be something.

As expected, forward consensus is stale. Very stale.

Even with the clear acceleration in its partner business that can quickly stack $75-$150M of highly profitable, incremental revenue in its next two out years, forward numbers for FY27 & FY28 have not moved. This is expected. After all, DOMO has not delivered the past few years. If anything, they burned the analysts following them. So, inertia on out-year numbers is understandable and how the game is played.

In many ways, this reminds us how WGS played out last year. Estimates remained ridiculously low throughout the entire year, allowing the company to trounce consensus each quarter. We think the same thing plays out in DOMO's upcoming Fiscal 2027.

Take a look. There is one clue though about what is coming. Even though the revenue numbers are silly low, to the discerning eye, one will see the very beginning of the forthcoming leverage on the bottom line in the highlighted areas:

With this as a primer, imagine what a 60%-70% flow through margin on the next $50-$150M of incremental revenues will do the bottom line. Wow, when it arrives, the profitability inflection will be something to see in CY26. It will take time though, but it is coming and it will be powerful.

To this end, we are currently modeling:

For Fiscal 2027: $375M in revenues, $60M in EBITDA and $0.50 in EPS

For Fiscal 2028: $469M in revenues, $115M in EBITDA and $1.25 in EPS.

Yes, we are WELL ABOVE CONSENSUS.

While our numbers are dramatically higher than consensus, we deem them as quite reasonable. DOMO is not partnering with an unknown start-up. This is Snowflake we are talking about. SNOW + DOMO = equals improved win rates, relative to MSFT. What should that be worth for DOMO's market cap? In and of itself, we think that is worthy of a 4x Price-to-Sales, multiple, as a starting point.

Keep in mind, SNOW trades for 21x Price to Sales.

So, a re-rate to 4x is quite rational and reasonable for us.

Were we to apply a 3.4x multiple on $469M in FY28 revenues, this would get us to $40.

Increase the multiple to 4x and we get a ~$47 stock.

A 4.5x multiple, gets us to ~$52.76.

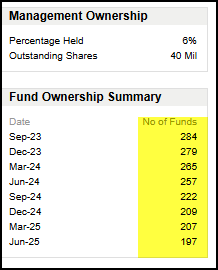

In addition to the forthcoming J-curve in forward numbers that are poised to manifest as the inflection point hits, another two ingredients poised to catalyze a significant re-rating in the shares are DOMO's tight share structure and its stagnant institutional base. If you build it, they will come.

In DOMO's case, we have only `40M shares outstanding, so the float is still super tight and then we have its institutional base, which has declined for 8 straight quarters. Not many funds left to sell. Everyone in the stock at this point surely sees what we see the next 12 months: a stair-step move to $20… $25… $30. It will not take much new blood to come in and cause a serious upside eruptionin DOMO's shares once growth investors get a hold of it in the high teens/$20s/$30s:

A final note: DOMO's CEO recently put his money where his mouth has been, accumulating $165k of shares in the $12s a few weeks ago, his eight purchase in two years. I give him credit for stepping up like he has on this front.

Clearly, should Snowflake decide to walk away from its partnership with DOMO that would immediately derail our long-term bullish thesis from manifesting. Thankfully, this seems EXTREMELY UNLIKELY anytime soon.

Snowflake is opening up its kimono to DOMO by introducing new sales teams to the company. This is what happens in a flourishing partnership.

DOMO expands SNOW's use cases. It is helping SNOW's win rates vs. Microsoft, as it makes the selling process dramatically enhanced with DOMO acting as the one-stop data aggregator solution for Snowflake.

Clearly, our FY28 numbers will occur much more easily if Databricks, Oracle, IBM and Google join the Snowflake party. We are not counting on that. Therefore, there is certainly the risk our numbers do not happen without them ramping up their sales efforts with DOMO.

Having noted such, we think SNOW can get DOMO to our numbers, in and of themselves, so we are currently not even focusing on these other partnerships. They would certainly bring an Uber Bull Thesis to $100 in play 2-3 years out, but it is too early to go there.

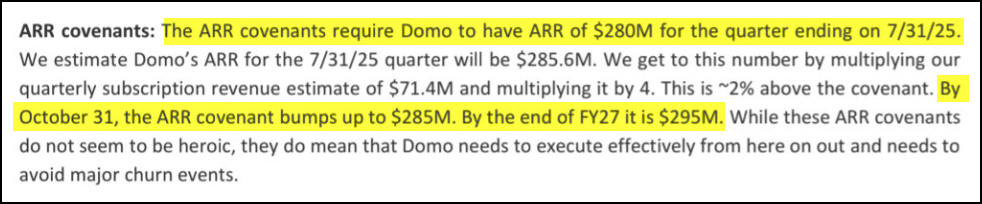

Finally, DOMO has specific covenants related to Debt that expires 4 years out:

These covenants seem like low bars to us. We doubt the CEO would have bought 165k of stock and been so bullish at DA Davidson, if there was any doubt these low hurdles would be hit.

While DOMO has doubled the last six weeks, we see 75% odds shares will double again the next 12 months. Moreover, we see strong likelihood an extended long-term move toward $50 will also manifest in the coming 18 months.

Everything lines up perfectly - the opportunity is huge, a multi-year SUPER CYCLE for software and data has just begun, DOMO is still very inexpensive and is still hated by BOTH the sell side and buy side. Meanwhile forward #s are silly low, the margin structure is top tier and the forthcoming leverage is quite easy to model out, for those willing to do the work.

Accelerating top-line growth, triple digit earnings growth, a tight share structure, combined with a huge dispersion between our numbers relative to consensus. It is music to our ears, as this is the same formula seen in many of our most recent big winners the last 15 months, including SEZL, POWL, APP, WGS, SMCI, ROOT, to name a few.

With a potential take out on the horizon as well, buttressed by its $2.2B in NOLS and $800M already invested into its full stack data platform, we are extremely bulled up on DOMO, as it is rare to find such value in a name levered to one of the biggest trends out there.

Stop Loss: As for a stop, we plan to hold DOMO through the November print. If we are wrong with our thesis, it will show up by then. But we like our odds and have therefore put our money where out mouth is with our outsized position and plan to hold DOMO well into 2026 should our thesis play out like we think it will.

-------------------------------------------------------------------------

Disclosure: We are long DOMO stock and various tranches of long-dated calls. We may change our positioning at a moment’s notice, without notifying you of any such moves.

Disclaimer: All of the information in this piece has been prepped by Inflections Consulting LLC. Readers should know that it would be incorrect to assume that past and future names of interest will be profitable or will not turn into a loss. Inflections Consulting LLC does not and will not assume any liability for any loss that could occur if you invested in such stocks written about.

All the content in these reports have been prepared by Inflections Consulting LLC. We believe our sources to be reliable, but there is no guarantee here. The information in this piece does not constitute either an offer nor a solicitation to buy or sell any of the securities name-dropped in this piece.

All contents are derived from original or published sources believed reliable, but not guaranteed. This report is for the information of Top Tier Inflections members/subscribers, only. Absolutely none of our content may be reproduced in whole or in part without prior written permission from Inflections Consulting LLC. All rights reserved.

In no shape or manner should the views expressed in this piece be considered investment advice. We reserve the right to change our positioning in our DOMO stock and options positions at a moment’s notice without updating you on any such change in opinion and positioning. That may be tomorrow, even before our price target is hit. Facts change, our opinions can change quickly too.

Investors need to consider their investment risk tolerance before investing in the stock market and also before investing in any of the stocks mentioned in this report.