Over the last few days the outlook for stocks has increased so strongly we liken the set up now into year-end as “Goldilocks, On Steroids”.

First, the China noise looks past us. While rare earths will still be used as a negotiating tool by China in the coming years, the impending China trade deal removes the biggest macro risk into the end of the year and, potentially, throughout 2026. Assuming this gets kicked down the road for a year, it opens the door for a potential 4-6 quarter move that could mirror what we saw after Long-Term Capital was resolved in the Fall of 1998 - a run for the ages that climaxed with a historical run to silly levels.

Secondly, with CPI showing muted gains, should PPI show a similar deceleration, it would only amplify the case for additional Fed Rate Cuts.

That's super bullish.

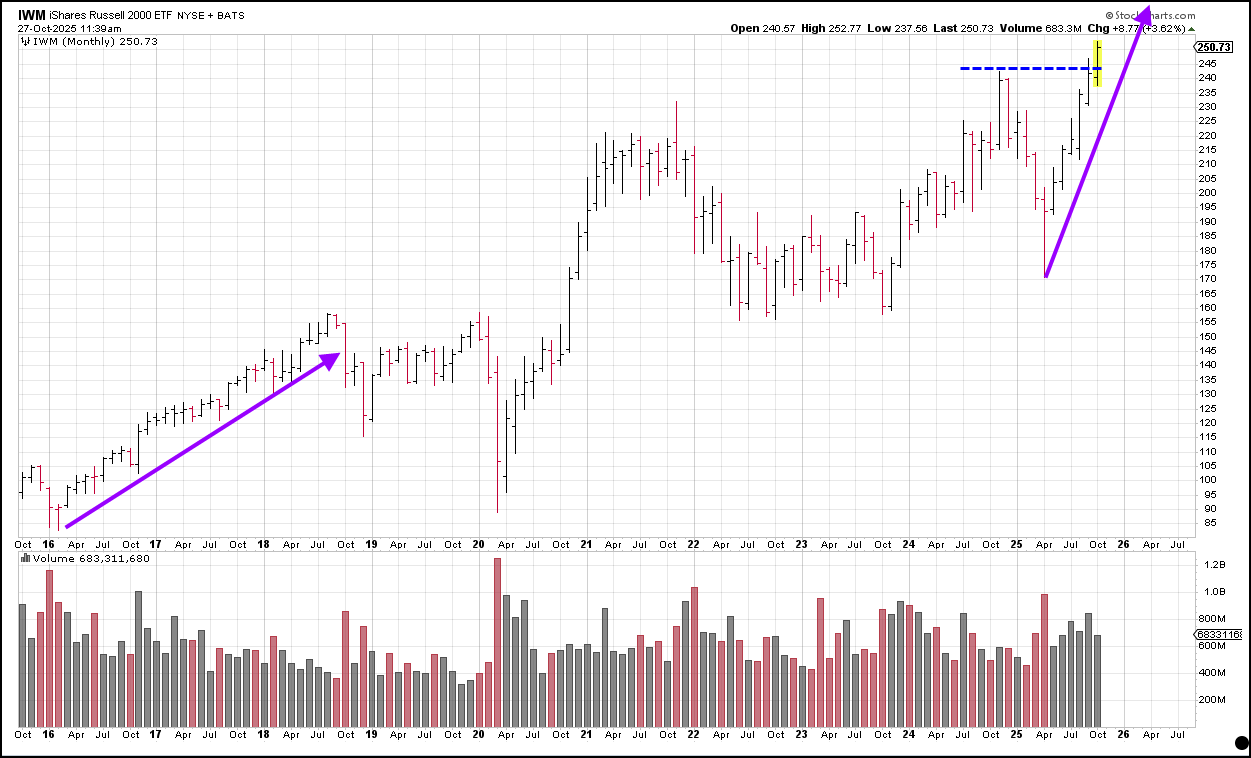

And this already meshes with what we are seeing play out in front us: Small Caps have quietly sprinted to all-time highs.

If the Fed is going to get more aggressive, after doing nothing for 4 years, why can't the Russell rise another 25-30% the next 12 months?

We think a multi-quarter move similar to the one that manifested from 2016-2018 is at hand:

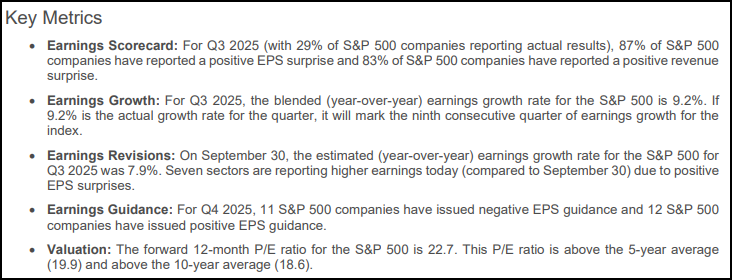

Thus far, earnings have been sensational.

The percentage of beats for S&P 500 companies are at impressive levels. We expect more good news from Big Tech this week. More on that shortly.

Some stats from our friends at Factset:

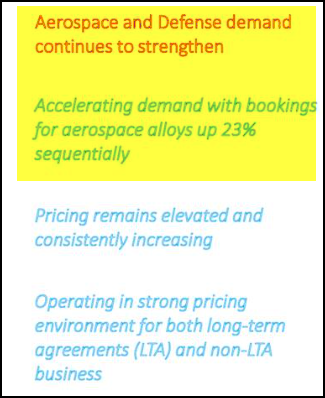

And, then, there is the Industrial Economy. It is inflecting in a major way.

Both Honeywell and steel speciality alloy play, Carpenter Technology Corp.(CRS) confirmed as much this week.

Here are some pertinent slides from CRS's earnings deck:

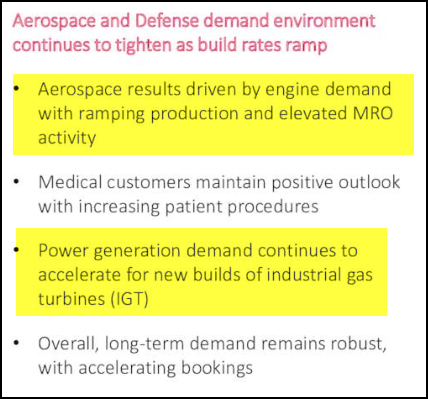

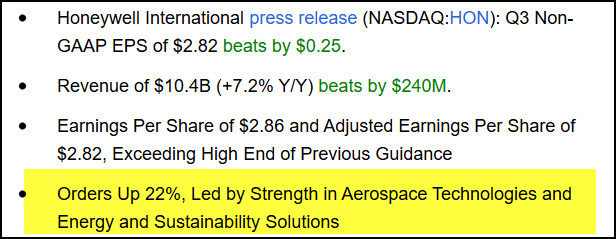

Honeywell International Inc. (HON)'s Q3 was also stellar. In particular, note the bookings strength:

We love when stocks break out to all-time highs. Everyone is a winner at all-time highs. And now, except for Mid-Caps, we have all the indexes at all time highs. We expect mid-caps to play catch up quickly.

Look what else is joining the all-time highs party... As of Friday, the NYSE Common Stock Only Advance-Decline Line is nearing never-before-seen levels:

We plan to get very aggressive tomorrow and ramp up our activity dramatically into year-end. We have been patiently waiting for the China narrative to pass and now we have the green light for what we think will be a huge move into-year end.

We think the S&P 500 can not only head to $7,000, but also to $7,500.

As for new tactical buys, let's start with our bread and butter, two small caps with tangible value we believe are poised for Top Tier moves the next 2-4 quarters.

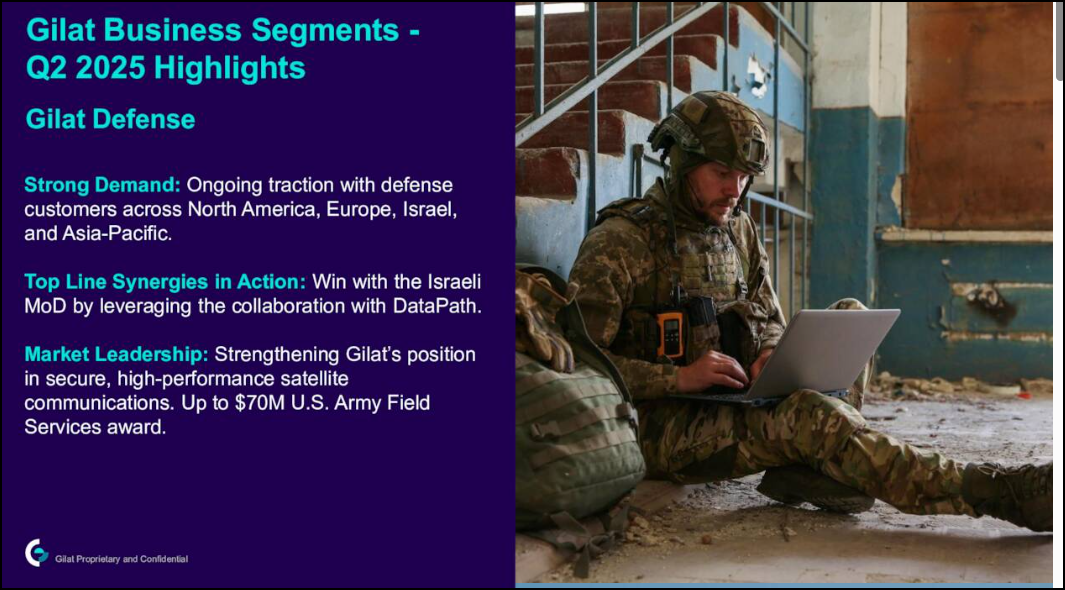

First, Gilat Satellite Networks Ltd. (GILT) is absolutely crushing it. Some 411 on the company:

Gilat serves three main verticals, Defense, Commercial and its International Business in Peru. They are all inflecting simultaneously:

We attach 75% odds GILT is headed to $25 the next 6-9 months. We also think $40-$45 is in play by the first half of 2027 if our uber-bull scenario of $1.50 in 2027 EPS plays out.

In the near-term, business is booming.

During the last six months, GILT has secured $340M of announced orders for its satellite and defense and communications verticals. Check out the Gilat's IR Page to see for yourself.

Current consensus is woefully low for not just Q3 and Q4, but also particularly for 2026 and 2027. Based on the current order momentum, we think there is a nice beat and raise coming when the GILT reports on November 13th.

Our confidence here centers on two inputs:

First, August's Q2 was a sizeable beat compared to consensus. Additionally, we expect GILT to show additional leverage in its bottom line in both Q3 and Q4 as well in 2026, as its Stellar Blu tuck-in reaches scale and crosses into EBITDA profitability.

In some ways, GILT reminds us of POWL last year at $100, when the Sell Side was asleep-at-the-wheel and forward numbers barely moved, even though Powell's order momentum had accelerated meaningfully.

We think the Sell Side will wake up and smell the coffee after the next print.

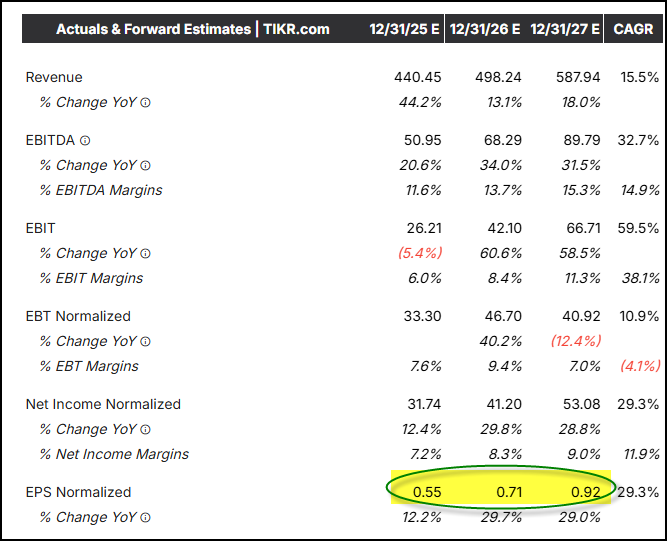

As for the next two years, we see $1.00 in EPS in 2026 and better than even odds we could see $1.50 in 2027, EPS numbers well above consensus:

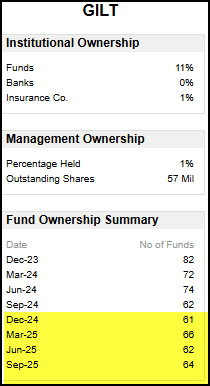

While GILT has doubled over the last three months, importantly, the company's institutional ownership remains extremely low and its accumulation period has only just begun. Look at this 20-year monthly base:

Only 64 funds are long GILT. So much runway here to re-rate:

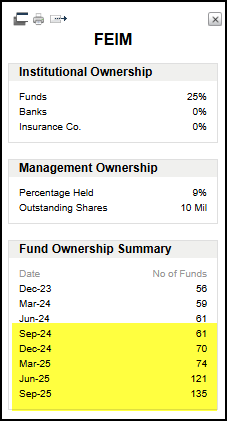

In many ways, GILT reminds us of FEIM when we recommended it last year at $13. Back then, nobody was paying attention to FEIM before it quietly tripled the last five quarters:

We are long GILT coming into Monday. We plan to increase our position again tomorrow, as we believe companies levered to Defense will see strong moves with the rare earth threat now removed from the narrative.

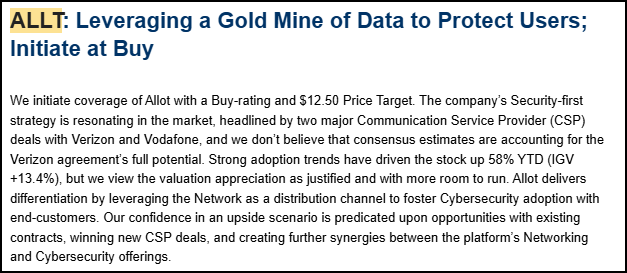

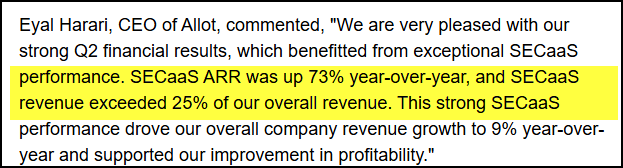

We are also very bullishly inclined on Allot Ltd. (ALLT), a ~$500M Israeli network management company that is poised to see a generational inflection point manifest in its dual-pronged business serving network providers. Allot also services Communication Service Providers with its consumer-oriented cyber-security solution.

Needham initiated coverage last week:

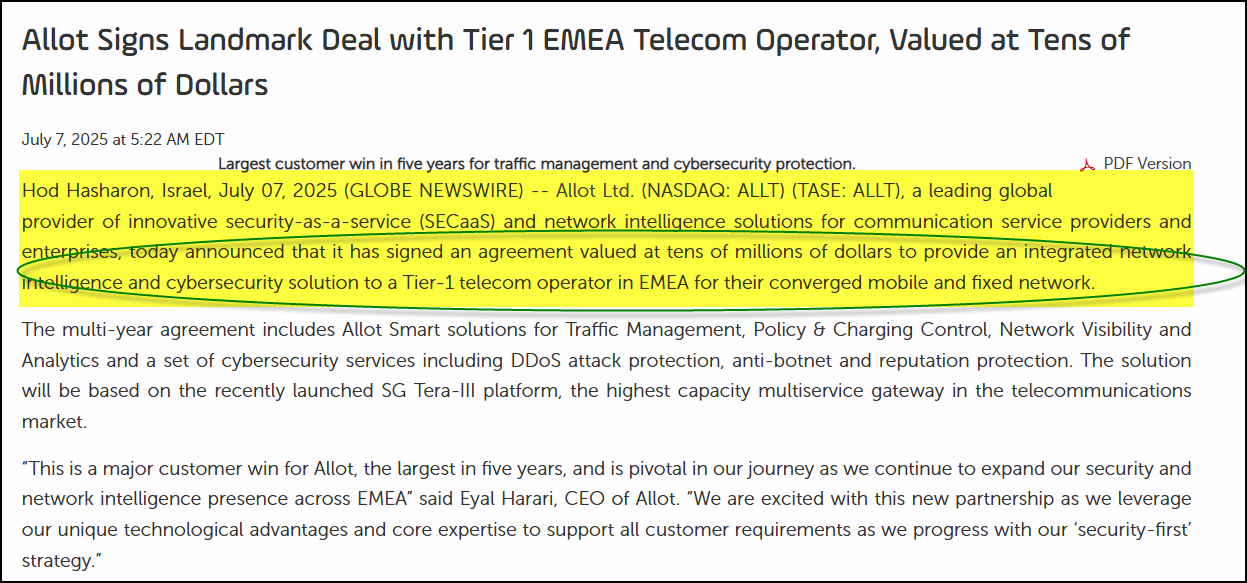

ALLT's legacy business, monitoring Large Communications Networks, is poised for a huge six quarters ahead.

This business has seen tremendous momentum in the last 3 months, with the company announcing its biggest deal in the last five years - supposedly worth anywhere between $50-$80M in revenues the next two years - late summer:

This is significant, as this deal came AFTER the momentum ALLT has been able to achieve the last few quarters in its legacy business.

In a stealth 6-K filing on September 30th, ALLT informed investors that its backlog growth had grown significantly from December 31st 2024 to June 2025:

"As of June 30, 2025, the aggregate amount of the transaction price allocated to remaining performance obligations that the Company expects to recognize is $ 93,783 of which approximately $ 66,552 is estimated to be recognized within the next twelve months and approximately $ 27,231 is estimated to be recognized after the next twelve months."

Add in the $50-$80M deal to the RPO as of June 30th and this means there is significant upside coming to forward numbers for Allot from this side of the business.

On Seeking Alpha, our props go to The Minataur, a hedge fund manager who has been super bullish on ALLT since $4.

His article HERE is worth the read. We completely agree with where his model is.

This is where the story gets juicy.

Allot has been quietly scaling its cyber security business with a number of large carriers. Of most import, are both Vodafone and Verizon, each of whom has granted Allot major add-on contract wins the last twelve months. And these ramps are just kicking in and have another 6-8 quarters of big growth ahead before they crest.

In Q2, the cyber division - which secures business lines from cyber attacks for both Vodafone's and Verizon's business customers - accelerated its growth rate to north of 70%. We think it exits the year closing in on a triple digit run rate:

Taken together, we see STRONG UPSIDE to not only Q3 and Q4 numbers for this year, but even more bullishly, for the whole of 2026 - for BOTH revenues and earnings.

How much upside?

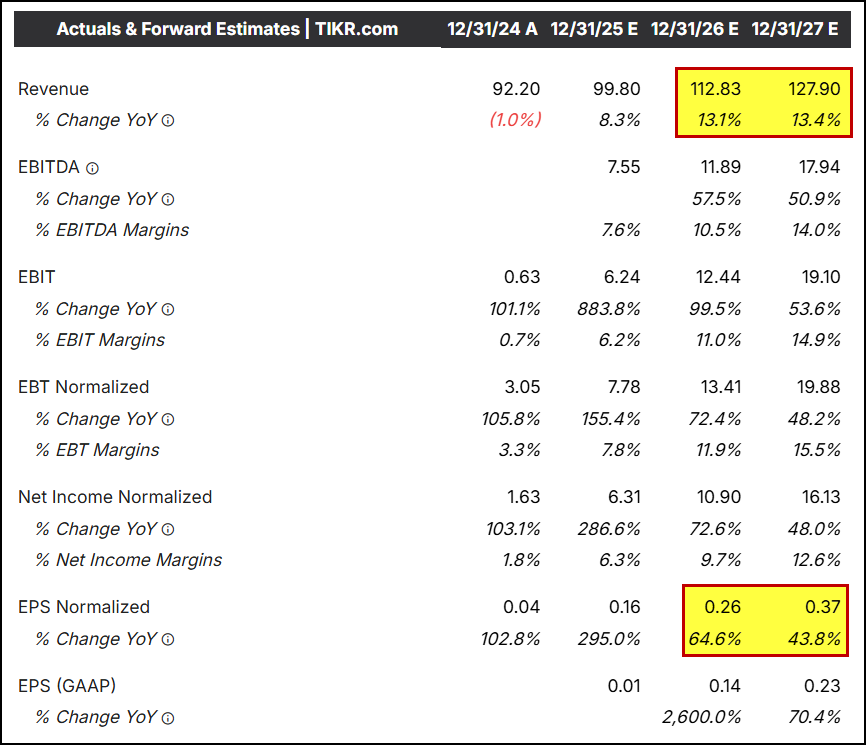

Well, for 2025, we think ALLT can do $130-$140M in revenues and earn $0.50 in EPS and for 2026, the company could do $170M-$190M in revenues and do $0.80-$1.00 in EPS.

2025 is really quite simple to model out, as the legacy business should do $90M next year and the cyber business, $40-$45M.

Needless to say our numbers compare quite favorably to current consensus:

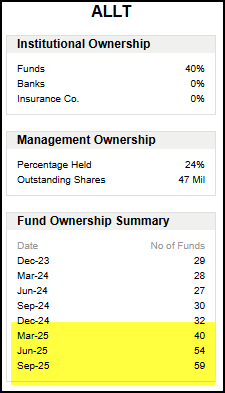

ALLT is also incredibly under-owned. We think the stock will double the next 3-4 quarters.

As its growth rate accelerates further, new growth funds will come onboard. Currently, there are less than 100 funds long the stock, so huge runway ahead for institutional ownership:

Importantly, the technicals jive with our fundamental work. ALLT has been basing perfectly. We think it is poised to go cray-cray the next 2-3 quarters.

$20 is our first long-term price objective.

We are long a small position in ALLT and plan to size it further in the coming days and weeks.

We advise getting onboard now ahead of the Q3 print.

ALLT only began giving guidance a quarter ago. No way they do that, and no way Needham comes out with coverage a few weeks ahead of the print, without there being nice upside relative to consensus.

To frame ALLT further, we see almost NO DOWNSIDE. Dangerous words in the stock market, right?

But, in ALLT's case, the math is simple and quite compelling. ALLT's cyber business is growing almost triple digits. It should do $45M in revenues in 2026. An 11x Price-to-Sales multiple for that business gets us the current market cap.

So, we are getting the legacy business and the future incredible cash flows all for free, when viewed from this prism. Incredible upside, relative to muted downside, its so rare to find in this market.

We plan to use a TIME STOP on both GILT and ALLT.

Each offers incredible value in a market where value is very tough to find.

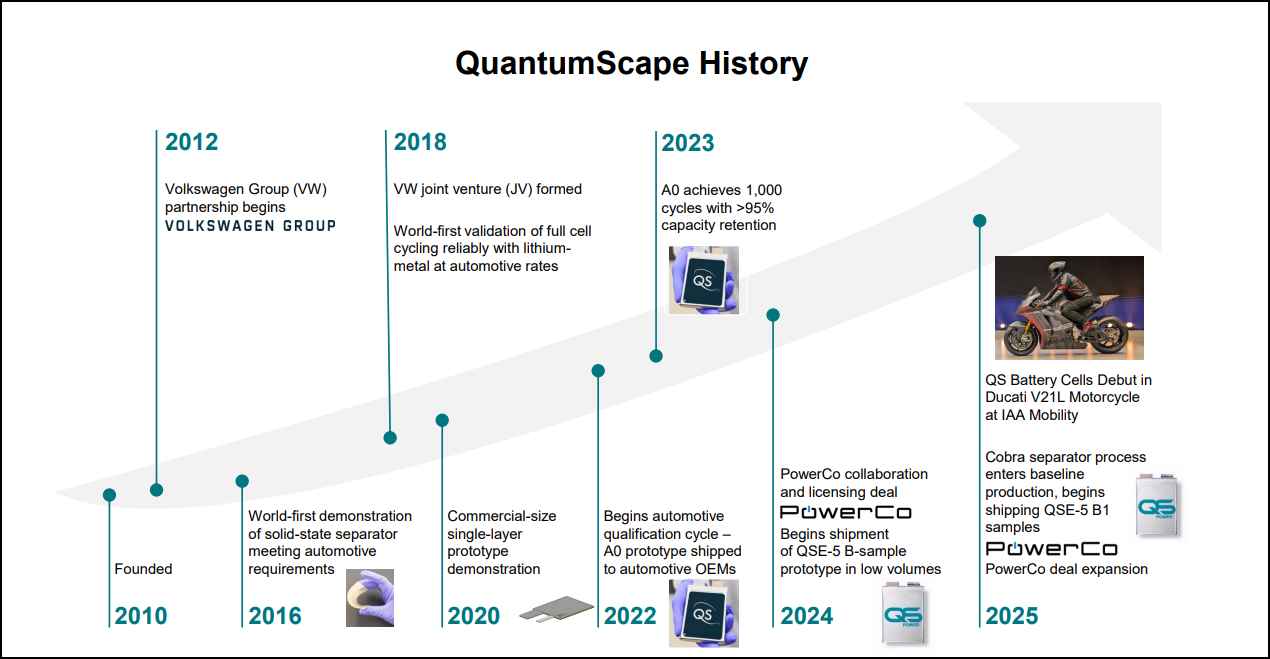

Turning to a mid-cap with multi-bagger potential, we are long a position in QuantumScape Corp. (QS). The thesis here reminds us of ASTS at $3 and then $6, when both AT&T and Verizon began to do business with them. A very similar thesis is playing out here for QuantumScape.

First some 411.

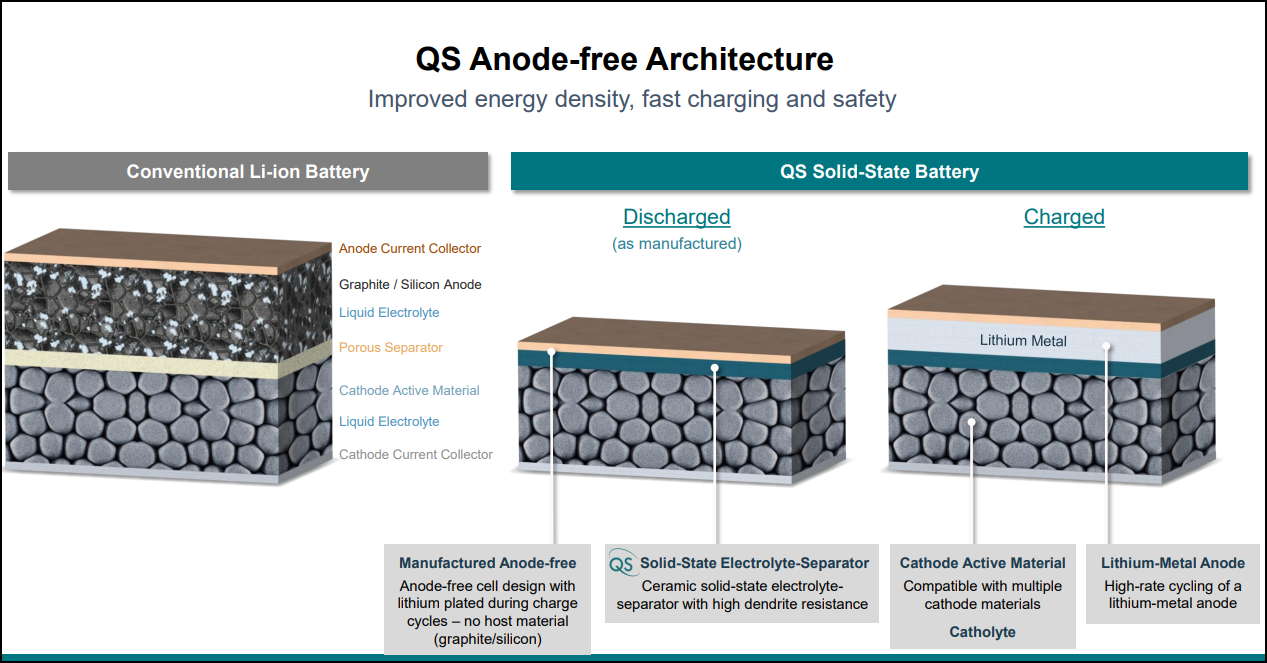

QS has what we view to be the best mouse trap for solid-state batteries, which have long been viewed as a science project, mostly because up until now, it HAS been a science project.

Quantumscape has been working on its technology stack for 15 years:

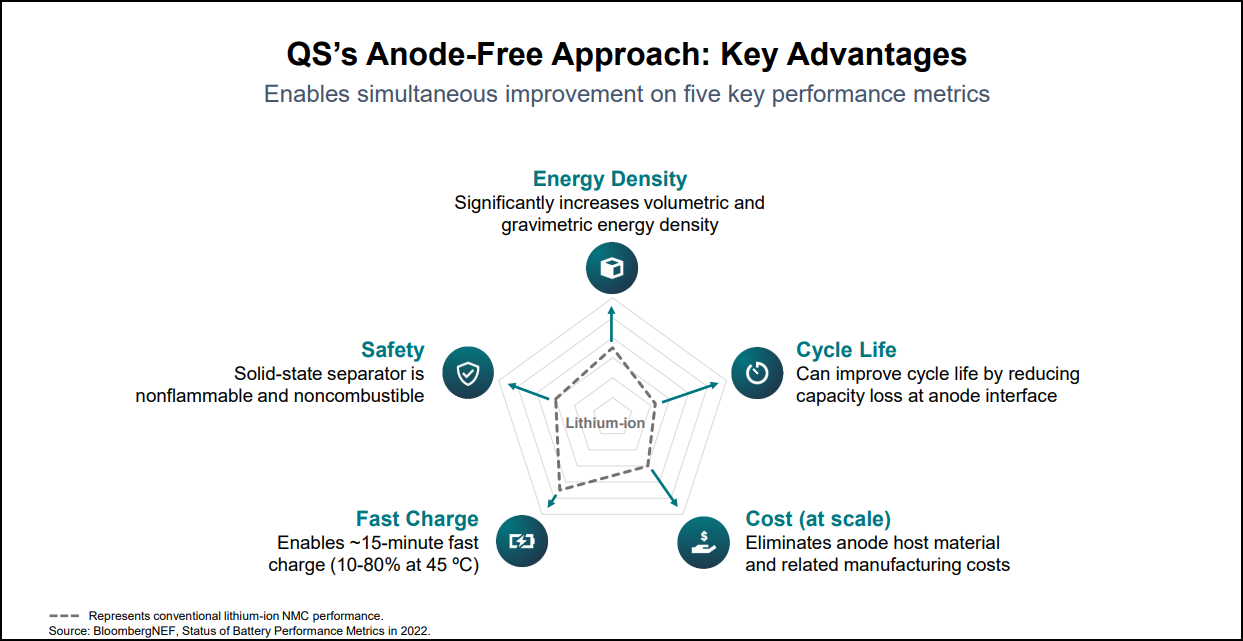

QuantumScape's technology has numerous advantages over other standard lithium batteries:

While its technology has always been impressive - QS has been partnered with Volkswagen since 2018 - there have been a few key events in the last few quarters that have materially increased the odds in the company's favor.

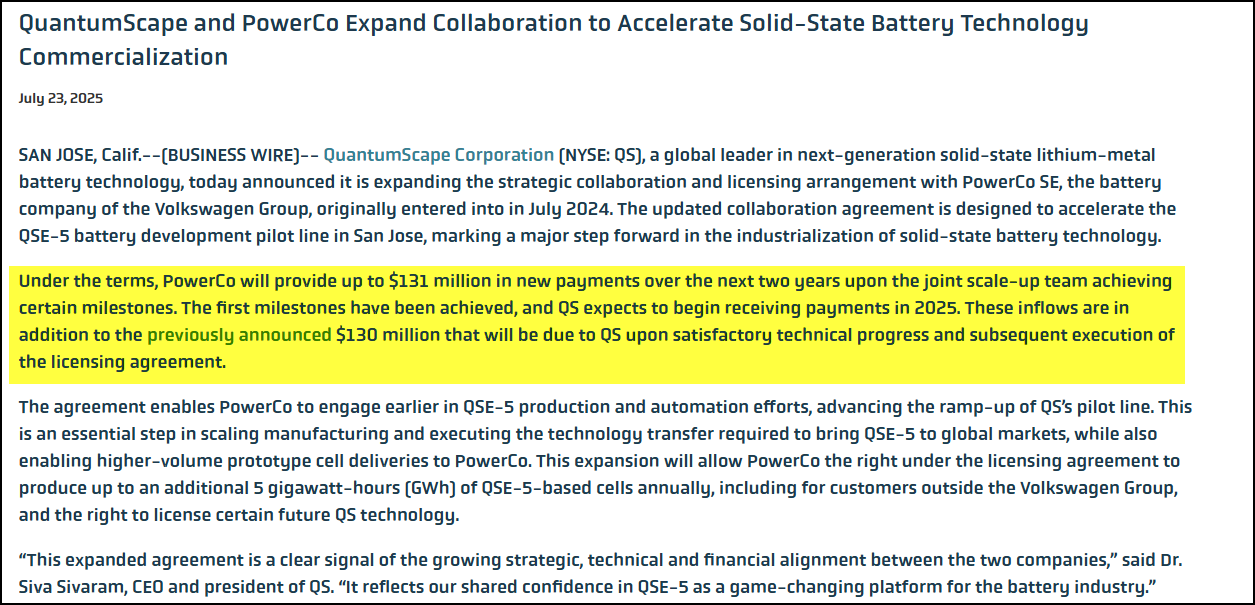

First off, Volkswagen has greenlit significant payments to QS for the next two years. QuantumScape recently invoiced VW for $12M in Q3. We are moving much closer to commercial adoption. This is a very clear signal Volkswagen believes Quantumscape has the goods:

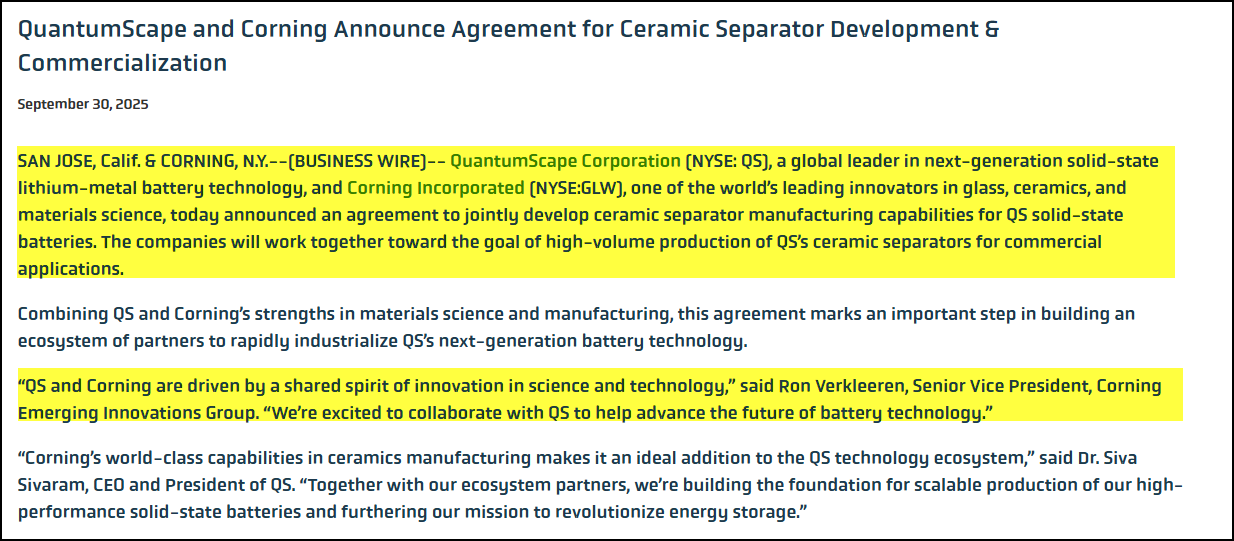

Then, QS announced a strategic deal with Corning. Bringing a tech stalwart like Corning aboard is further validation the company's battery tech is legit and it will be able to scale:

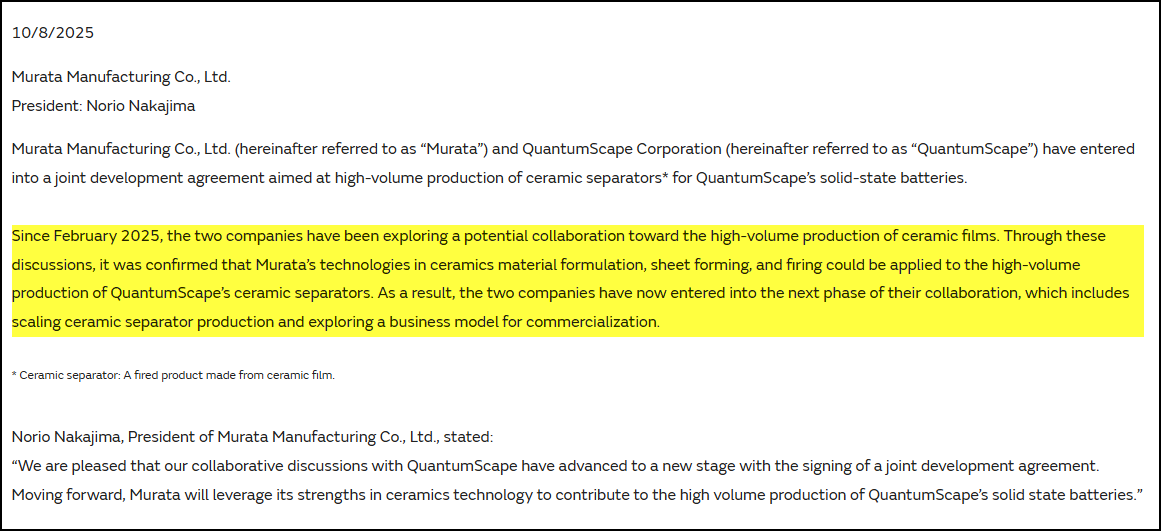

And finally, the icing on the cake. After vetting QuantumScape's technology for almost three quarters, Murata, a $35B Japanese conglomerate, has gone deeper with the company, forging an important partnership that will help QuantumScape scale its manufacturing capabilities:

While this is not yet Game-Set-Match, we view these three partnerships as the most important events to happen to QuantumScape in its corporate history. Collectively, the odds now seem to be better-than-even that QuantumScape may turn out to be a generational disruptor and compounder over the next 5-10 years.

IF it works, we believe QS - which currently sports a $9.4B market cap - will go to $100-$200 over the next 4-6 years, as its business model will be highly profitable.

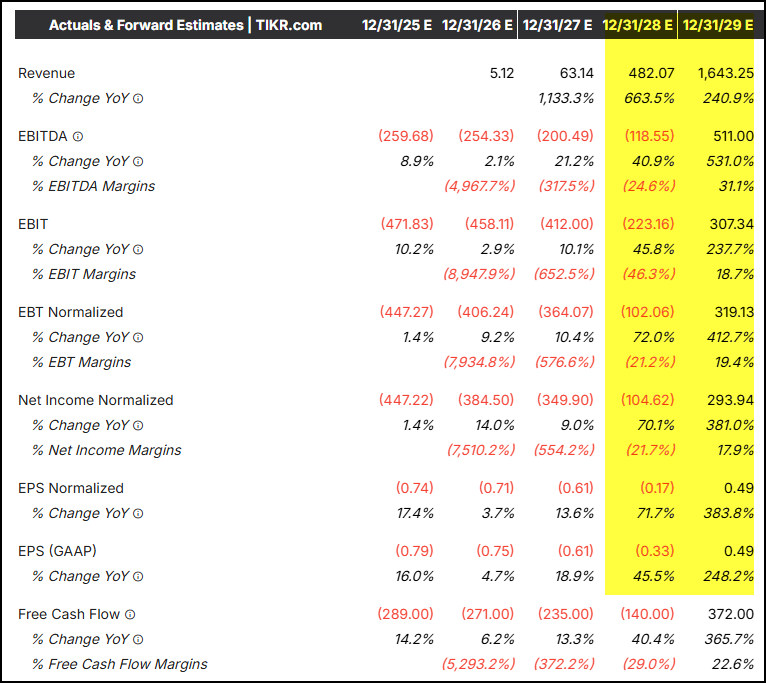

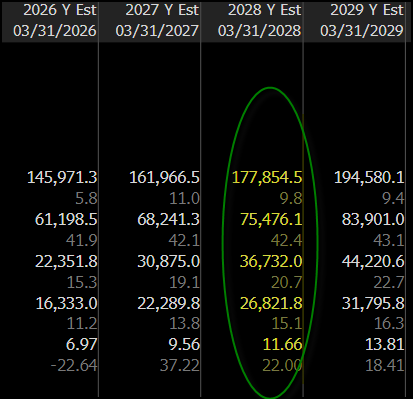

While still years out, check out where consensus stands for 2028-2029. There are some juicy numbers there - the benefit of its capital-light business model being created:

By 2030-2031, QS could be doing $2.5B-$4B in revenues if its technology gets adopted by other large OEMs and it continues to generate 50% EBITDA margins. To this end, we believe QS is actionable in the near-term, as on its conference call late last week, the company announced it has begun close talks with a new Top 10 Global OEM potential customer.

For those worried about further dilution, QuantumScape has enough of a cash runway to last now through 2030, so dilution will be minimal from here.

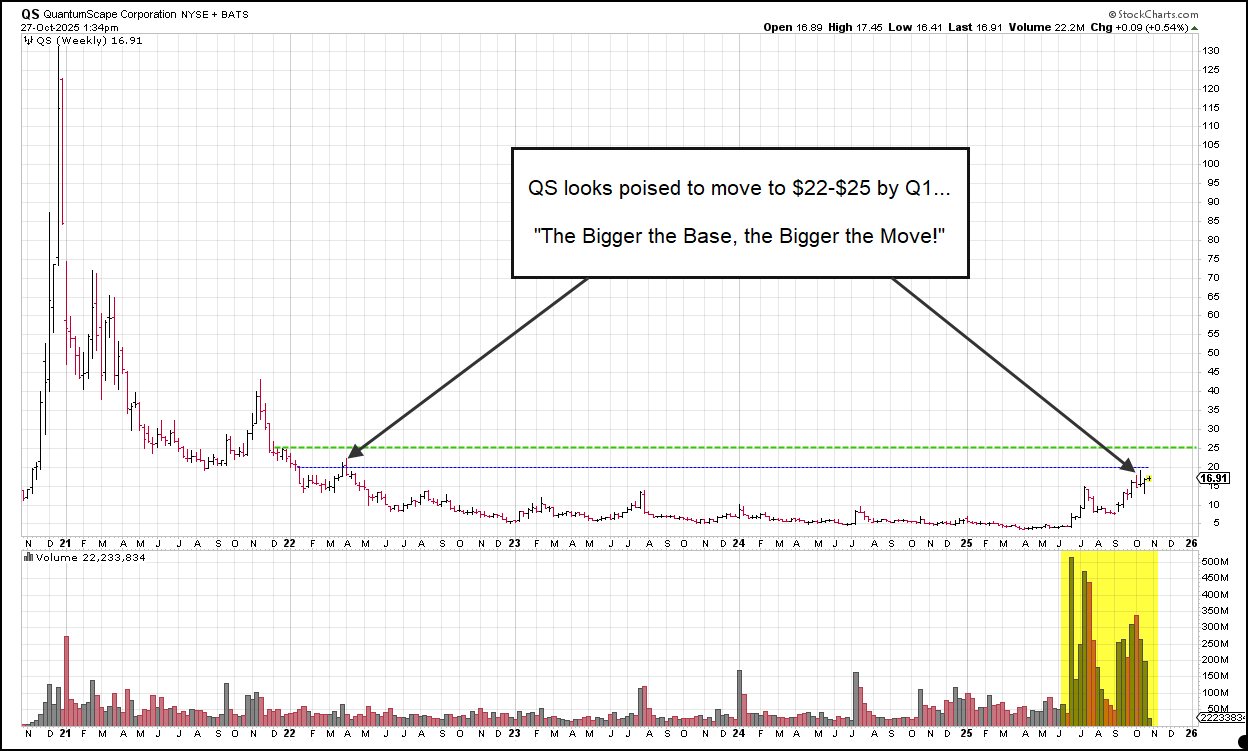

Taken together, we believe QS is poised for another marked leg higher. This has potential to be a Tesla-like disruptor and we think the news flow gets incrementally better its recent run-up is a precursor to another big up-leg into year-end.

The technical picture suggests a move to $22-$25 by early Q1 is forthcoming...

"The bigger the base, the bigger the move!"

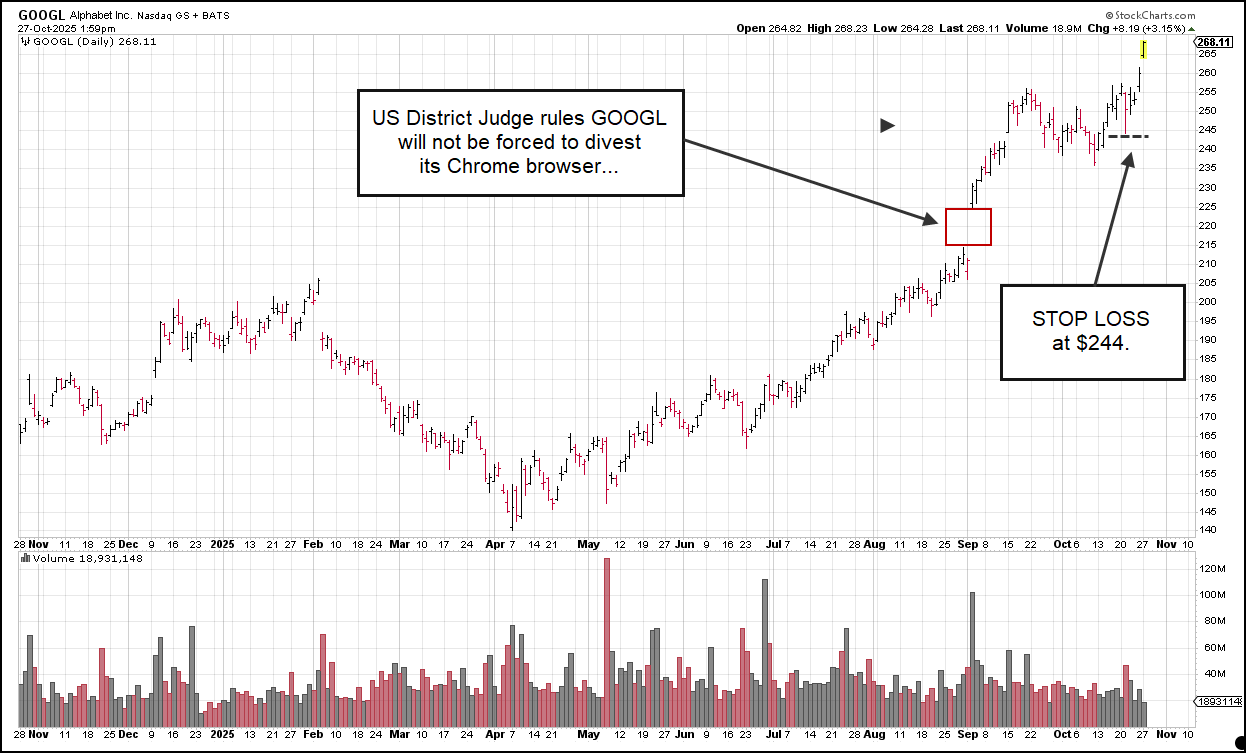

Turning to two Mag 7 stocks, we are very bullish on Alphabet Inc. (GOOGL) heading into its print this week.

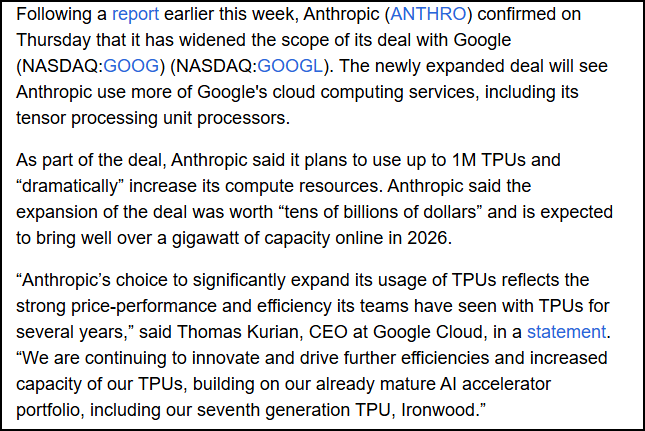

Last week's deal for "tens of billions" of revenues from Anthropic was a seminal announcement that we believe has not been fully-digested by the market. We think this incrementally increases the odds that Alphabet's 2026 numbers are too low, a key metric the Sell Side will be focused on this earnings call:

Ad checks have been very strong for Q3 and fears of OpenAI decimating Google's search business have been overblown.

We plan to implement a STOP LOSS at $244, just below last week's lows:

If we are right, and there is a path to 25% EPS growth for next year, we think Alphabet can re-rate to a mid-twenty PE, which gets us to $300 by Q1.

Not sexy, but very high odds are thesis plays out.

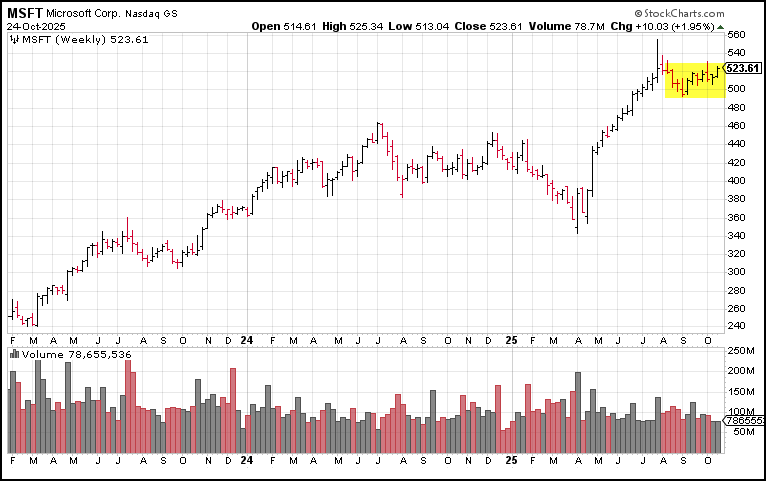

As for the software space, we like Mr. Softie, Microsoft Corp. (MSFT), into earnings. Its technical pattern is pristine:

Channel checks have been very bullish, as well. Here is a quick blurb from UBS last week:

"In speaking with 11 customers and partners at Oracle's (ORCL) AI World event, UBS analyst Karl Keirstead said the tone of the conversations about core cloud infrastructure spending was positive. Spending on artificial intelligence inference and training spending should provide the opportunity for upside as well, he added.

“We see minimal upside to Street estimates for AWS, with more upside potential in Azure and Google Cloud,” Keirstead wrote in a note to clients.

Delving deeper, he said the tone in the conversations was better than it was just three months ago, and the “progression in tone about overall cloud infra spending is notable.”

“While several of the [Fortune 500] enterprises spoke to flattish IT budgets in 2025, none – zero – were planning on incremental spending cuts or delays and in fact some partners said that they began seeing a loosening of budgets in 3Q, an 'unfreezing'”, Keirstead explained.

“While this diligence focused on the 85-90% of AWS, Azure and Google Cloud revs coming from enterprise customers ('core' demand), demand for cloud-hosted GPUs from AI model providers and start-ups remains outstanding, with no obvious slowdown in 3Q25.”

Other notable takeaways from the conversations include the fact that AI-induced pull-through of data software demand should help the hyperscalers and companies such as Snowflake (SNOW).

There is also the belief that Microsoft Azure is taking market share, as three partners said their Azure practices accelerated in the third-quarter or were expected to in the fourth-quarter. Conversely, the partners described their Amazon Web Services practices as “landing slightly below expectations” for the third-quarter, with forecasts of steady in the fourth quarter, Keirstead relayed."

We will stop out at $499. We expect MSFT to immediately push higher. If we are correct, then we can see a pathway to $600 by Q1. So good symmetry here, reward to risk wise, we believe.

And then, we have one final new buy for tomorrow - Alibaba (BABA).

With its arm wrestling with the U.S. almost done, we think China will now turn its attention to revitalizing its domestic economy and that Alibaba is the best way to play it, as not only a play on an eventually improved consumer, but also, as the best A.I. play.

Importantly, BABA is still well below all-time highs. If our thesis plays out, once BABA clears its first zone of resistance $200-$210, we see a spirited move to $260 and then $300 playing out:

And, why not? If BABA's AI chips begin to replace some of NVDA's why can't the company earn $13-$14 in Fiscal 2028? A modest re-rate to a low 20s P/E would get us back to all-time highs. After all, if earnings are poised to inflect to all-time highs, won't the stock discount that ahead of time? We think this is poised to occur in BABA. Here is what consensus looks like:

We plan to give BABA extra room due to how tough the Chinese stocks trade. We will use a stop loss at $163.75, just below last week's lows. If we are right, we will then raise our stop in increments, as we view this as a longer-term hold and a trade we are viewing from a longer-term prism.

While a sell the news is certainly possible in the very near-term - as expectations were certainly building for this China deal - with the overarching fundamental backdrop improving materially on numerous fronts, we plan to incrementally add exposure to the capital we oversee not only tomorrow but throughout this week and through year-end.

Earnings season really kicks in this week, so we are also leaving room to add new buys as well, as this is our time when we typically do our best work - when vol is low, new leaders are inflecting and new themese are manifesting. This is the backdrop we now have and one which we believe could extend well into 2026, potentially, setting us up for what may be prove to be a parabolic run for the ages spurred on by a Goldilocks backdrop on steroids.

Stay tuned. We expect to be in touch quite frequently in the coming weeks and months with new Top Tier Inflections.

--------------------------------------------------------------------------------------

Disclosure: We are long ALLT, BABA, GILT, GOOGL, MSFT, QS. We may change our positioning at a moment’s notice, without notifying you of any such moves.

Disclaimer: All of the information in this piece has been prepped by Inflections Consulting LLC. Readers should know that it would be incorrect to assume that past and future names of interest will be profitable or will not turn into a loss. Inflections Consulting LLC does not and will not assume any liability for any loss that could occur if you invested in such stocks written about.

All the content in these reports have been prepared by Inflections Consulting LLC. We believe our sources to be reliable, but there is no guarantee here. The information in this piece does not constitute either an offer nor a solicitation to buy or sell any of the securities name-dropped in this piece.

All contents are derived from original or published sources believed reliable, but not guaranteed. This report is for the information of Top Tier Inflections members/subscribers, only. Absolutely none of our content may be reproduced in whole or in part without prior written permission from Inflections Consulting LLC. All rights reserved.

In no shape or manner should the views expressed in this piece be considered investment advice. We reserve the right to change our positioning in stock and options positions at a moment’s notice without updating you on any such change in opinion and positioning. That may be tomorrow, even before our price target is hit. Facts change, our opinions can change quickly too.

Investors need to consider their investment risk tolerance before investing in the stock market and also before investing in any of the stocks mentioned in this report.