Kiniksa Pharma (KNSA) is a biotech company ramping one drug for Pericarditis, which is swelling and irritation of the thin, saclike tissue surrounding the heart. More 411 here on Pericarditis.

Kiniksa has the ONLY approved biologic to treat Pericarditis and the company is only 13% penetrated. Pericarditis is a multi-year disease which has multiple recurrences. So, there is a big runway for the company and they should become a $1B company in 2027.

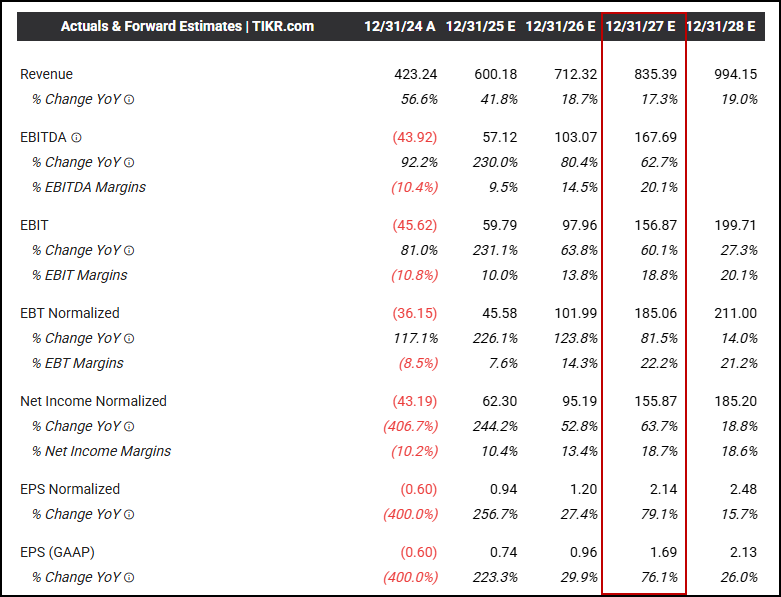

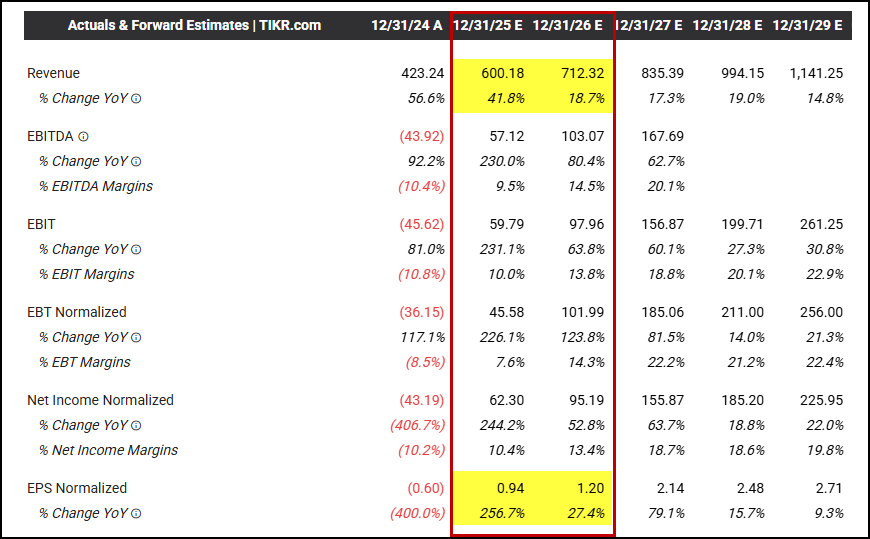

Here is what consensus currently looks like:

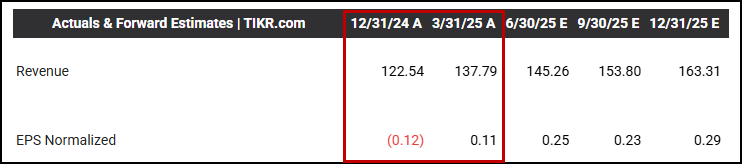

Q1 is typically the most difficult quarter for reimbursement for orphan drug companies. Usually, Q1 is down ~10% sequentially from Q4 to Q1 (note highlights):

Not this quarter, where revenues GREW 10%, sequentially:

This inflection is significant for three reasons:

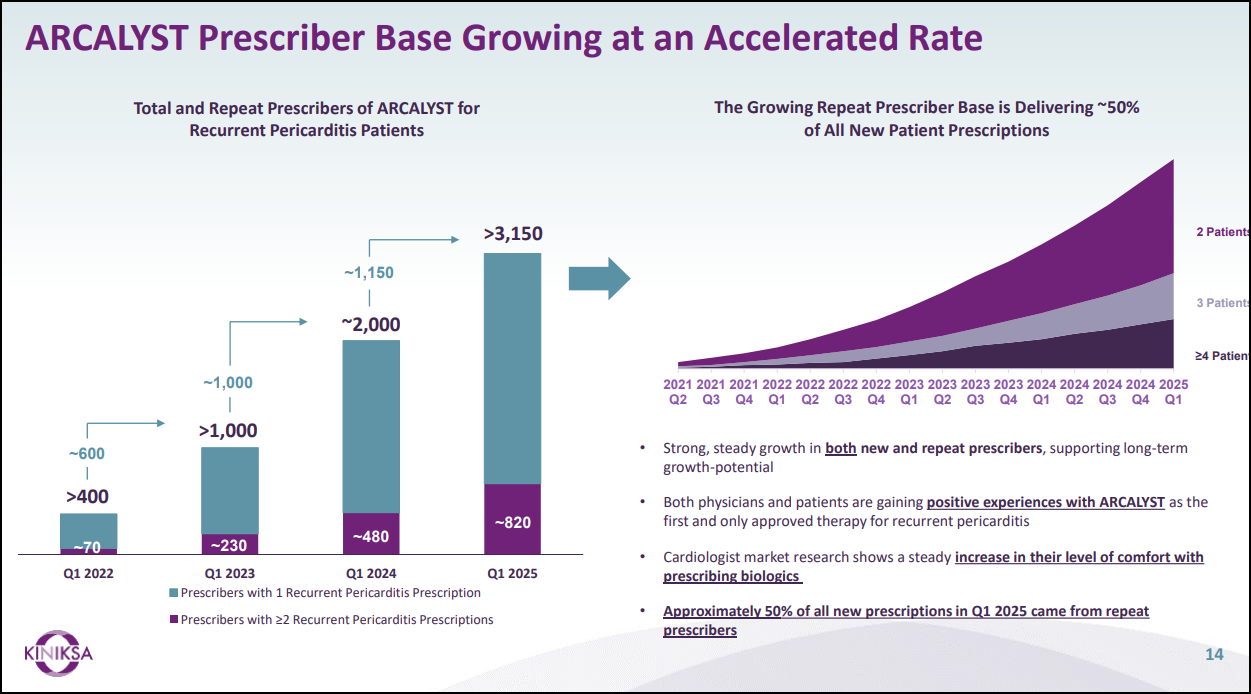

1. Adoption has accelerated again with Kiniksa gaining over 300 new physicians prescribing the drug:

Kiniksa has also expanded its sales force, ramping from 50 to 85 reps over the past few quarters. We think this will increase adoption naturally, helping the company to stack revenues quickly.

Kiniksa is also smartly being proactive on a number of digital initiatives to help drive awareness and is implementing care teams to sound the word to doctors about the need for long-term usage of ARCALYST. These efforts have helped forward-ordering expectations by doctors to expand nicely:

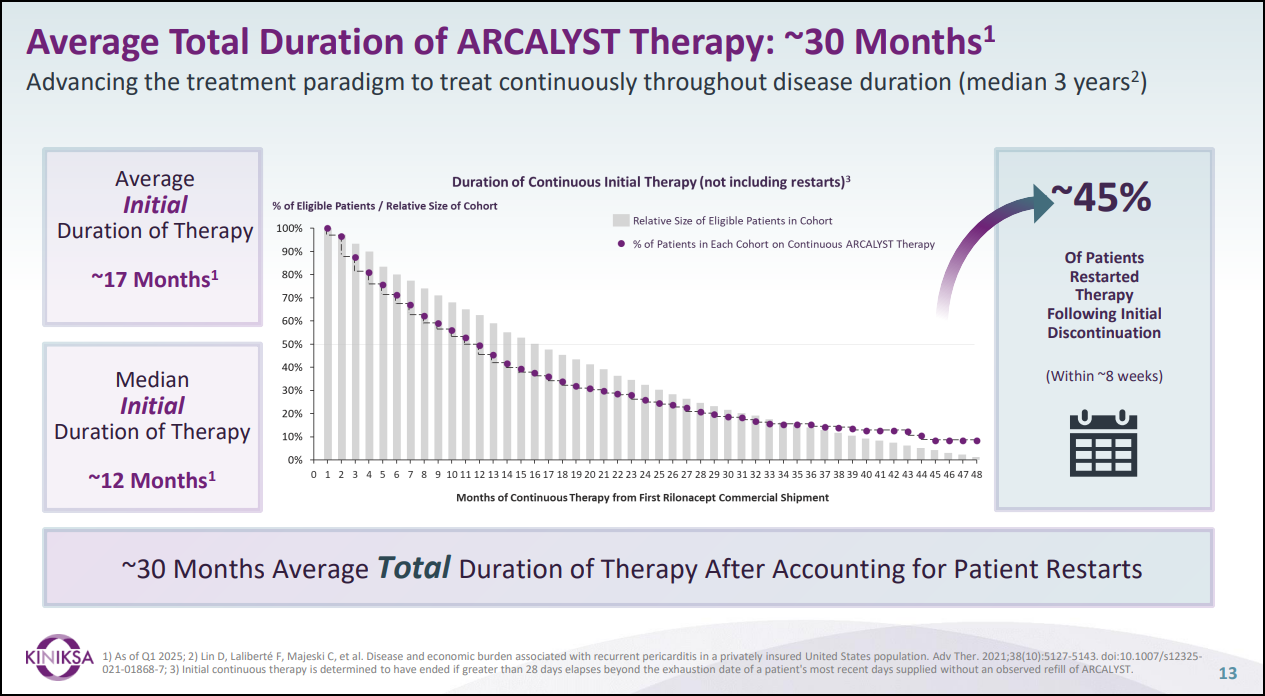

Another component to the story we love is how the duration of treatment is becoming extended, from 27 months previously to 30 months now. This will translate into a longer revenue tail for each patient:

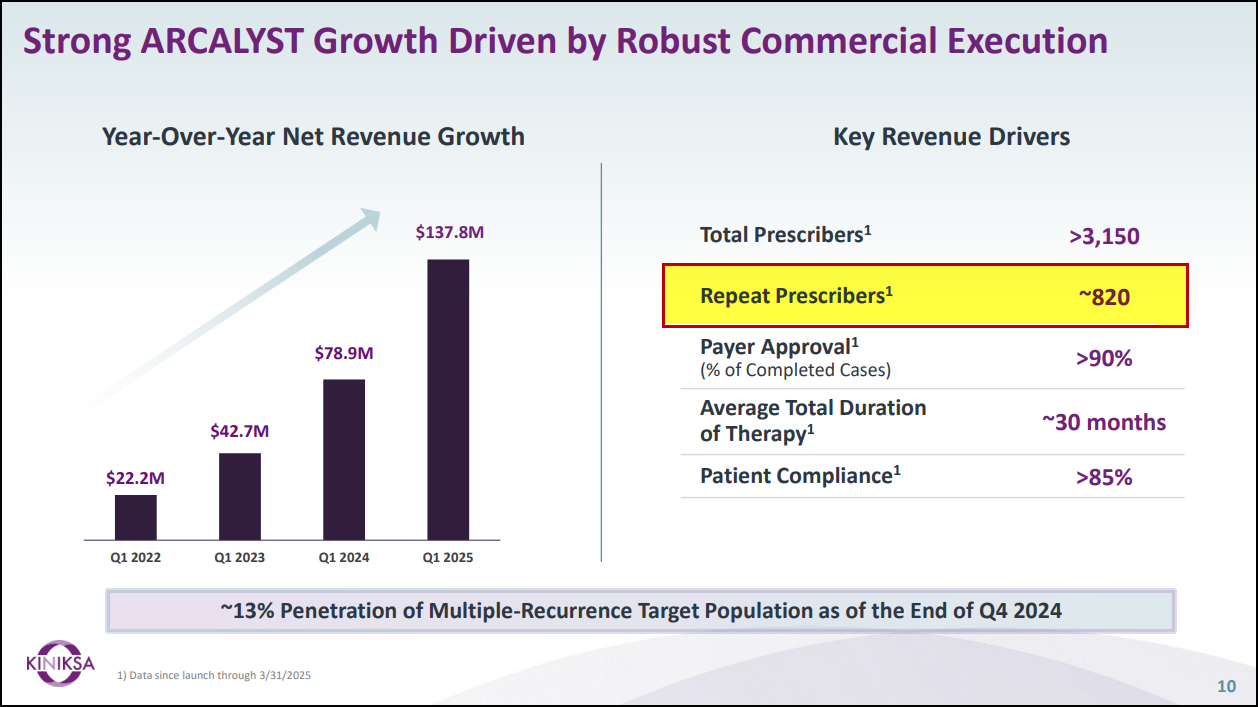

2. A 50% of all new prescriptions in Q1 2025 came from repeat prescribers. As noted in the slide below, repeat prescribers were 820 in Q1, which was up almost 85% Y/Y. This means doctors who have adopted Kiniksa’s, ARCALYST, are rolling it out to their new patients as well, illustrating their satisfaction with the safety and efficacy of the drug:

3. With revenues accelerating to 75% in Q1, it creates an easy bar for Kiniksa to surpass forward consensus in the next few quarters. We think Kiniksa does 57% revenue growth this year, well above the guidance raise issued by the company.

Importantly, not only did KNSA beat consensus nicely in Q1, they also announced a strong guide up for the entire year:

Reports Q1 revenue $137.8M, consensus $131.71M.

"Kiniksa continues to drive strong growth with ARCALYST. In Q1 of 2025, our robust commercial execution resulted in a meaningful increase in active commercial patients, driven by increases to the prescriber base, longer average total duration of treatment, and changes to Medicare Part D.

As a result of strong Q1 performance, we are increasing our expected 2025 ARCALYST net sales to between $590-$605M from our previous guidance of between $560-$580M.”

Typically, Q1 to Q2, Kiniksa has seen a 35% increase sequentially in revenues. Current consensus is calling for only a ~7% increase, or, only a 34% Y/Y increase in revenues. We see strong upside, relative to consensus:

We see $667M this year and $880M next year, along with $1.15 in EPS this year and $2.25 next year. Notably each metric is WELL ABOVE CONSENSUS. Take a look:

As for KNSA stock, it literally has done nothing in 10 years.

We think this inflection is somewhat easy to model out and other savvy healthcare investors will hold tight the next few quarters. Why sell when a seminal inflection point, with a clear line of sight to $1B in revenues and 20% EBITDA margins, is within view.

As such, it won’t take much incremental buying to spur this nascent breakout to 52-week highs, and, eventually, all-time highs:

We are buying via VWAP today and reserving room to add on dips to $25.50-$26. We see the stock heading to $30 in the near-term and to $35-$40 by year end.

Stop Loss: We plan to use a 10% STOP from cost. This is wider than normal, but due to our 10 conviction in the name – only given to the best Top Tier Inflections – we think a wider stop is warranted.

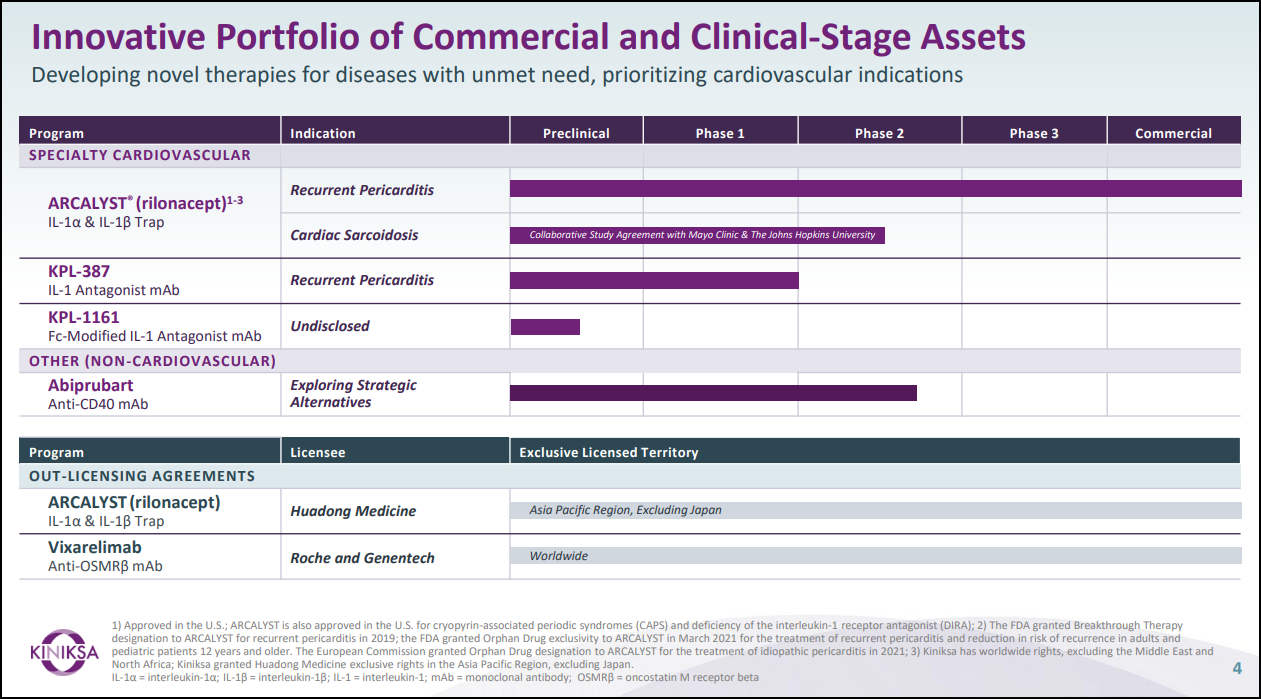

Clearly, one product companies always have a big risk just by focusing on the one product. Importantly, KNSA is a rare breed of a fast growing biotech company that is also investing in its expanded pipeline:

As for tariff exposure, it is de minimis, as its partner, Regeneron, who gets half the profits from the drug, is positioned well there, geographically. In terms of other risks, we think reimbursement risk is also de minimis, which leaves us with market risk.

Financing risk is non-existent as the company is sitting on $250M in cash and also generating cash.

But, considering KNSA has done nothing since coming public, we think it is one of the chosen few to enter its own bull market this year.

---------------------------------------------------------------------

Disclosure: We are long KNSA stock and calls. We may change our positioning at a moment’s notice, without notifying you of any such moves.

Disclaimer: All of the information in this piece has been prepped by Inflections Consulting LLC. Readers should know that it would be incorrect to assume that past and future names of interest will be profitable or will not turn into a loss. Inflections Consulting LLC does not and will not assume any liability for any loss that could occur if you invested in such stocks written about.

All the content in these reports have been prepared by Inflections Consulting LLC. We believe our sources to be reliable, but there is no guarantee here. The information in this piece does not constitute either an offer nor a solicitation to buy or sell any of the securities name-dropped in this piece.

All contents are derived from original or published sources believed reliable, but not guaranteed. This report is for the information of Top Tier Inflections members/subscribers, only. Absolutely none of our content may be reproduced in whole or in part without prior written permission from Inflections Consulting LLC. All rights reserved.

In no shape or manner should the views expressed in this piece be considered investment advice. We reserve the right to change our positioning in our KNSA stock and options positions at a moment’s notice without updating you on any such change in opinion and positioning. That may be tomorrow, even before our price target is hit. Facts change, our opinions can change quickly too.

Investors need to consider their investment risk tolerance before investing in the stock market and also before investing in any of the stocks mentioned in this report.