LendingClub Corp. (LC) has been one of the longest standing online banks and marketplaces for consumers to get loans.

The company has operated very conservatively over the years and it should also be noted its results have been consistently INCONSISTENT. Consumers do love LendingClub’s products and offerings, as its NPS score is a very impressive 80+:

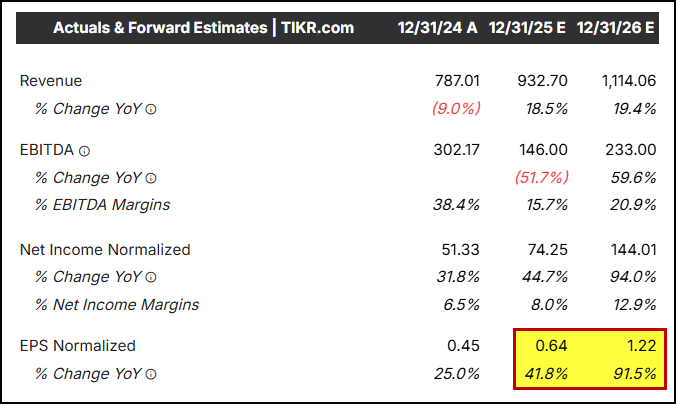

Notwithstanding its inconsistent past, LendingClub reported a dynamic beat and raise quarter, with revenue growth and original growth inflecting above 30%, which spearheaded a 100%+ EPS beat relative to consensus:

LendingClub is seeing success attracting new consumers to its offerings with new product launches as well as new marketing initiatives. The new marketing programs are luring back inactive consumers to engage more with its marketplace, creating a strong set-up for the back half of the year.

Historically, Q3 is the best quarter of the year for the company, typically up 7%-8% sequentially.

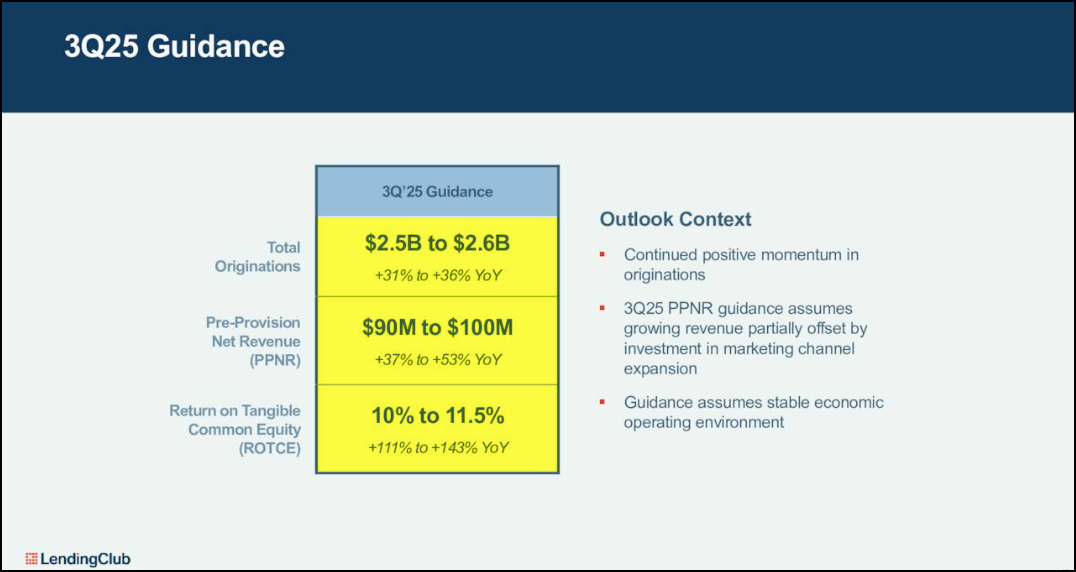

Looking ahead, LendingClub raised its origination guidance for $2.5-$2.6B in Q3, which translates into a strong guide up relative to current estimates. Importantly, the company also guided to a flat Q4, relative to Q3, which is significant as Q4 is usually down from Q3.

Essentially, LendingClub reported a big beat AND two guide ups. That is the significant inflection here and why we bought in during AH last night.

Before this report, LendingClub was expected to make $0.62 in EPS in 2025. Now, Jefferies has them making $1, along with $1.42 next year. We think LendingClub will end up doing $1.15 this year.

While next year is a ways off, given that LendingClub is poised to exit the year at a $1.60 run rate, we believe the odds are very good they earn close to $2 a share. All of these numbers compare very favorably to where estimates were ahead of this print:

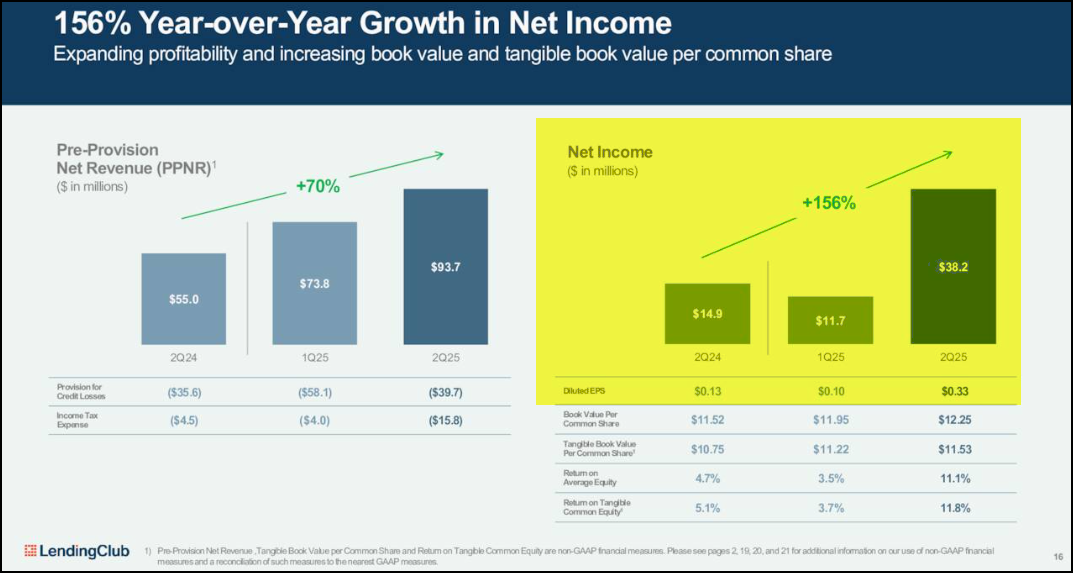

Currently, LC is trading up 23% pre-market. We bought the stock in After Hours last night with a $15.90 cost basis. The last time LC printed a $.33 quarter its stock was coming down from the $40s during the Pandemic.

Though we are not looking for a move into the $40s, we DO think there is a clear shot to $20 in the very near-term. Subsequently, $25-$30 should be in play if LendingClub can post another beat in Q3.

Remember, EPS growth inflected by 150%+, so it's reasonable to expect LC’s multiple to re-rate to 20x after another good quarter. Just look at the re-rates in SOFI and DAVE as growth re-accelerated the last few quarters:

Looking ahead to Q3, LendingClub’s top line is poised to inflect to the mid-to-high 30s as new marketing efforts produce better results. We think there is upside to the current guidance:

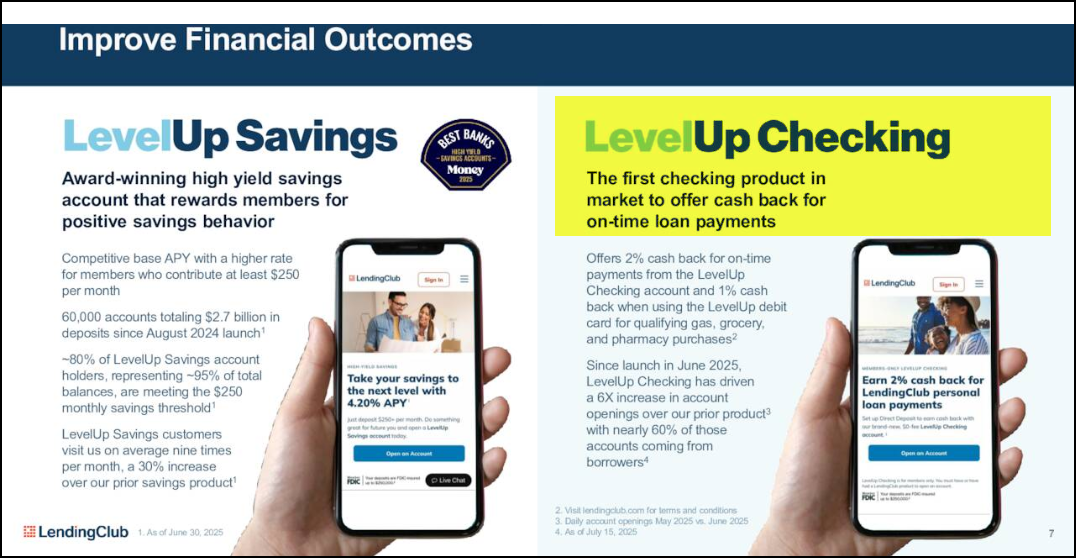

In June the company launched an important new product called LevelUp Checking.

This is an important new product success for LendingClub, as new account openings are up 6x compared to before LevelUp’s release:

Here is what Management had to say about LevelUp Checking:

"We recently launched LevelUp Checking specifically for our borrowers, along with paying 1% interest on qualifying balances, it has 2 key features:

First, is 1% unlimited cash back on everyday purchases like gas and groceries. Here, we're rewarding our members for using money that they have versus money that they borrow thereby incenting good financial behavior.

Second, and this is unique to us. We're offering 2% cash back for on-time personal loan payments from a LevelUp Checking account. We're rewarding borrowers for their financial discipline while allowing us to benefit from a stickier relationship.

While it's still early, the initial results are encouraging, we're now opening 6x more checking accounts per day than prior to launch with nearly 60% of these accounts being opened by borrowers."

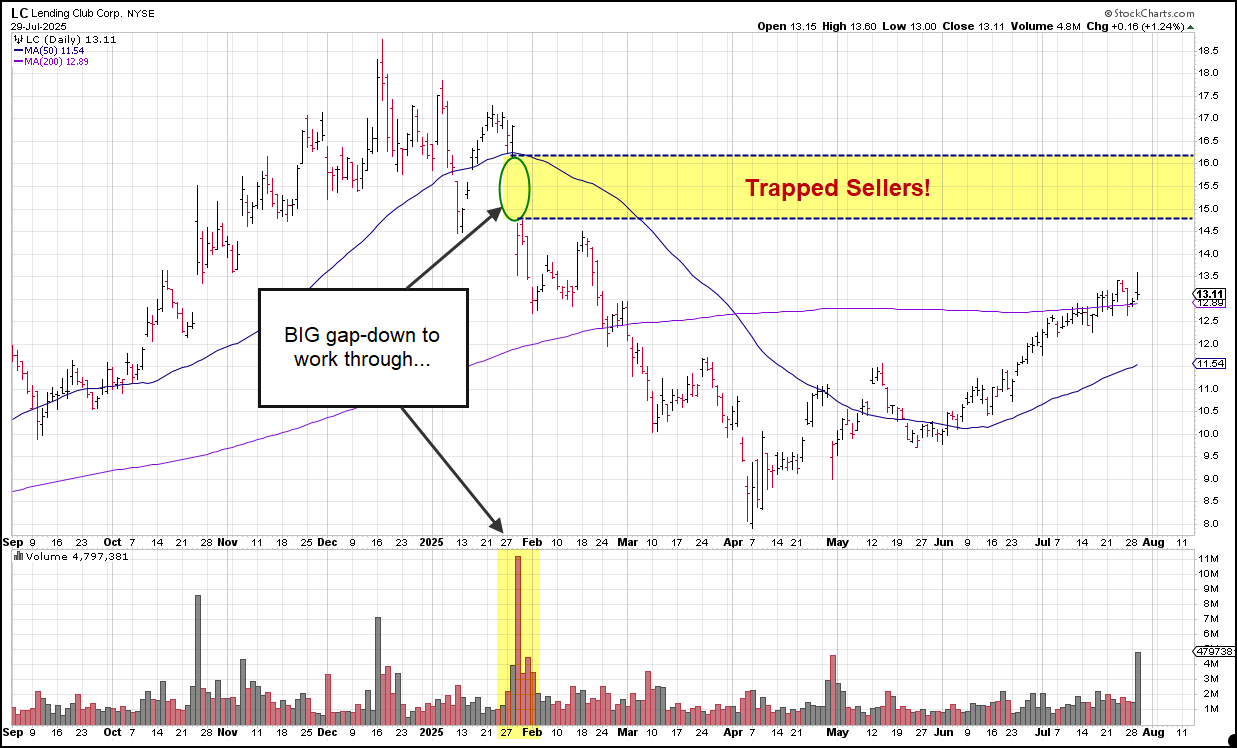

Technically, LC has a big gap-down at $16 to work through.

Similar to how WGS got stunted as it gapped-up into a huge band of resistance, there is certainly the risk LC does not follow through due to this gap where trapped sellers lay.

We therefore think LC will need to trade 8-11M shares today, an ~8-11x volume inflection relative to ADV, for the stock to forge to new highs.

STOP LOSS: We will stop out 10% below cost. We attach 80% odds this works, thus the looser-than-normal stop.

LendingClub has all the “Top Tier” elements we look for in an inflection, and our process dictates moving into the name with an oversized position. In our experience, BIG beat and raises that result in demonstratively higher forward numbers will typically translate into a marked re-rate of a stock.

It’s also very rare to find accelerating growth AND a cheap valuation in this market. So we are looking for other generalist funds to join the LendingClub party in the coming days and weeks, which will amplify the inflection in the stock.

Given that earnings for 2025 are poised to rise 125% this year and another 40-50% next year, we like our odds with LendingClub.

That said, we could be wrong.

The market may simply not agree with our assessment that LC deserves a mid-teen multiple due to its history of inconsistent execution. But with LendingClub’s clear inflection and easy-to-model forward numbers, we think the market will quickly see what we see. So we will take this bet every time.

We intend to scale out of a 1/3 to 2/3 of our position on a move to new highs and the $20s. We will plan to ride the final tranche for what could be a long-term move to $25-$30 the next few quarters.

LC Conviction Level: 8.5

-------------------------------------------------------------------------------

Disclosure: We are long LC stock and calls. We may change our positioning at a moment’s notice, without notifying you of any such moves.

Disclaimer: All of the information in this piece has been prepped by Inflections Consulting LLC. Readers should know that it would be incorrect to assume that past and future names of interest will be profitable or will not turn into a loss. Inflections Consulting LLC does not and will not assume any liability for any loss that could occur if you invested in such stocks written about.

All the content in these reports have been prepared by Inflections Consulting LLC. We believe our sources to be reliable, but there is no guarantee here. The information in this piece does not constitute either an offer nor a solicitation to buy or sell any of the securities name-dropped in this piece.

All contents are derived from original or published sources believed reliable, but not guaranteed. This report is for the information of Top Tier Inflections members/subscribers, only. Absolutely none of our content may be reproduced in whole or in part without prior written permission from Inflections Consulting LLC. All rights reserved.

In no shape or manner should the views expressed in this piece be considered investment advice. We reserve the right to change our positioning in our LC and options positions at a moment’s notice without updating you on any such change in opinion and positioning. That may be tomorrow, even before our price target is hit. Facts change, our opinions can change quickly too.

Investors need to consider their investment risk tolerance before investing in the stock market and also before investing in any of the stocks mentioned in this report.