We attach 80% odds that Ramaco Resources, Inc. (METC) is headed to $30-$40 by the end of this year. We see 50% odds we can overshoot to $50+ too. Let's dig in.

The rare earth sector has reached a critical inflection point, spearheaded by last week's $400M investment into MP Materials, the only current domestic producer of rare earths. Yesterday, the group inflection became amplified with Apple's $500M investment into MP Materials, as well.

This inflection is poised to gather steam in numerous ways in the coming months and quarters.

Yesterday, the DoD stated they plan to backstop the entire group. So, one can expect additional public/private partnership/investments into other important players in the space.

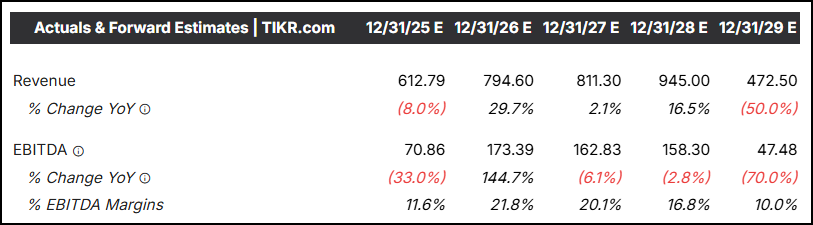

Turning to Ramaco, the company is a coal producer. They have real revenues and EBITDA. This morning, Jefferies ascribed nearly $13 of value to their coal operations. Here is what consensus looks like currently - the company has done a great job of operating with some of the highest EBITDA margins, relative to competitors:

In 2012, Ramaco spent $2M and bought the Brook Mine coal deposit in Wyoming. This purchase may go down in American mining history as one of the most prolific purchases ever. What? Let's explain.

Eight years ago, scientists from the Department of Energy came to the company. Their AI models showed strong odds for a significant rare earth deposits in this coal formation. Well, they were right.

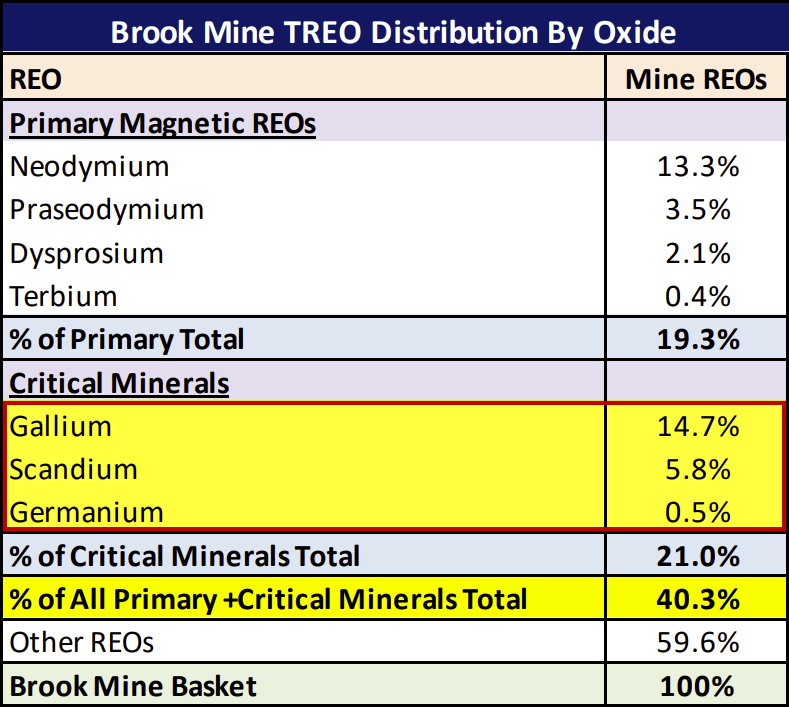

Last week, Ramaco released a finalized report from noted engineering firm, Fluor, showcasing the vast reserves of 7 critical minerals. The CEO summarized these results in a shareholder letter. We took the liberty to bold the most important details:

"Before I present both the Fluor and Weir International findings, I want to frame the dimensional potential. We have studied roughly one third or roughly 4,500 acres of a 16,000-acre deposit. Ramaco largely owns the mineral reserves in fee. The overall Brook Mine contains over 1.1 billion tons of coal deposit and is one of the largest private mineral holdings in the West.

As I explain in more detail below, we have reason to believe that as we progress our further analysis of the overall site, and the remaining two thirds of the deposit is then tested and cored at greater depths, that the overall size of the deposit may increase with similar mineral profile characteristics.

Interestingly, given the location of the deposit on the far edge of the Powder River Basin (PRB), we have been advised that the rare earth deposit characteristics at the Brook Mine may be narrowly confined to the immediate area of the site.

We received an original mining permit from the State of Wyoming to annually mine roughly 2 million tons of ore contained in coal on the site. We have been encouraged by the federal government in order to meet the nation’s critical supply needs to consider both the acceleration of the timing of development of the mine, as well as a possible future expansion of its production and processing capacity. We will be working with stakeholders to consider our ability to do both, which could enhance the ultimate potential to both our shareholders as well as the country.

As to the mine’s potential, based on the work that we have done with our technical partners, we believe the Brook Mine would support about 3-5% of total United States permanent magnet demand, or more than 30% of the demand for U.S. defense applications, which is estimated at 10% of total U.S. magnet metal demand."

Importantly, there are 4 big advantages Ramaco has with their rare earth deposits, including:

What's "critical" to understand here is that Ramaco's reserves have a shelf life of 42 years. And the current estimated reserves are based off of only 1/3 of its acreage.

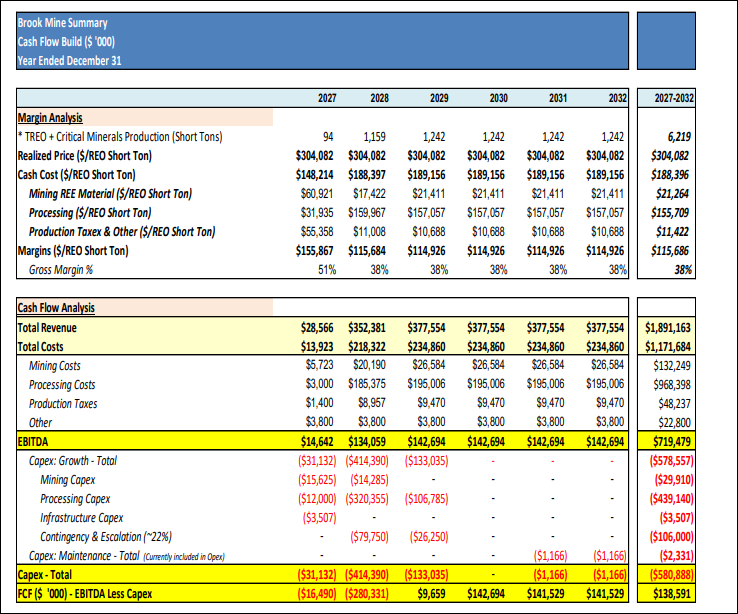

In its assessment report, Fluor laid out what the model looks like at scale in 2028. If one were to apply a similar 21x EV/EBITDA multiple that MP has received by the market (~$12B valuation), then over the next 18 months, METC could head to $65 on a sum-of-parts basis: $51.75 of value for its REE deposits and ~$13 of value for its coal operations. Here is Fluor's long-term model:

METC included this comp in its shareholder letter. This is why the stock has been under such rabid accumulation. While there is clear execution risk with the processing plant yet to be built and nearly $600M of capital required to achieve scale, relative to MP's valuation, METC is still significantly undervalued in the low-to-mid $20s:

Last week at the ribbon-cutting ceremony for the Brook Mine in Wyoming, the head of the Department of Energy was there. Ramaco recently added Senator Joe Manchin to the board. The company is already having back channel discussions with the government about how they can work together.

In the near-term, Ramaco has announced plans to do a shareholder/analyst call shortly. This is the next catalyst.

Another potential catalyst is our belief that METC is also likely to secure a DoD investment as well. The DoD is on record stating it is “all in” on rare earths.

"The US Department of Defense plans to continue working with rare earths companies to ensure diverse American supply of the critical minerals used across the economy," stated a senior defense official following the announcement of the landmark investment [in MP Materials].”

Similar to Apple’s subsequent investment in MP, we believe METC will also receive direct investments from large defense companies like Northrop or Raytheon, to name a few. These are just a couple of logical companies that will be happy to invest in order to secure long-term domestic supplies.

If we are correct and these investments into METC come to fruition, we think the stock will quickly boomerang into the $30s and head toward $40. This is the heart of what we are playing for here.

While there is a long-term case for $60 to $100:

Shouldn’t METC theoretically trade for at least half, if not two-thirds, of MP's market cap? Consider that its REE deposits contain NO radiation, and will be 100% domestically-sourced, AND potentially provide 30% of the permanent DoD reserve requirements for the next 42 years.

We are not going there, yet. That is a long journey – one where we would certainly keep a third of our position if our thesis plays out.

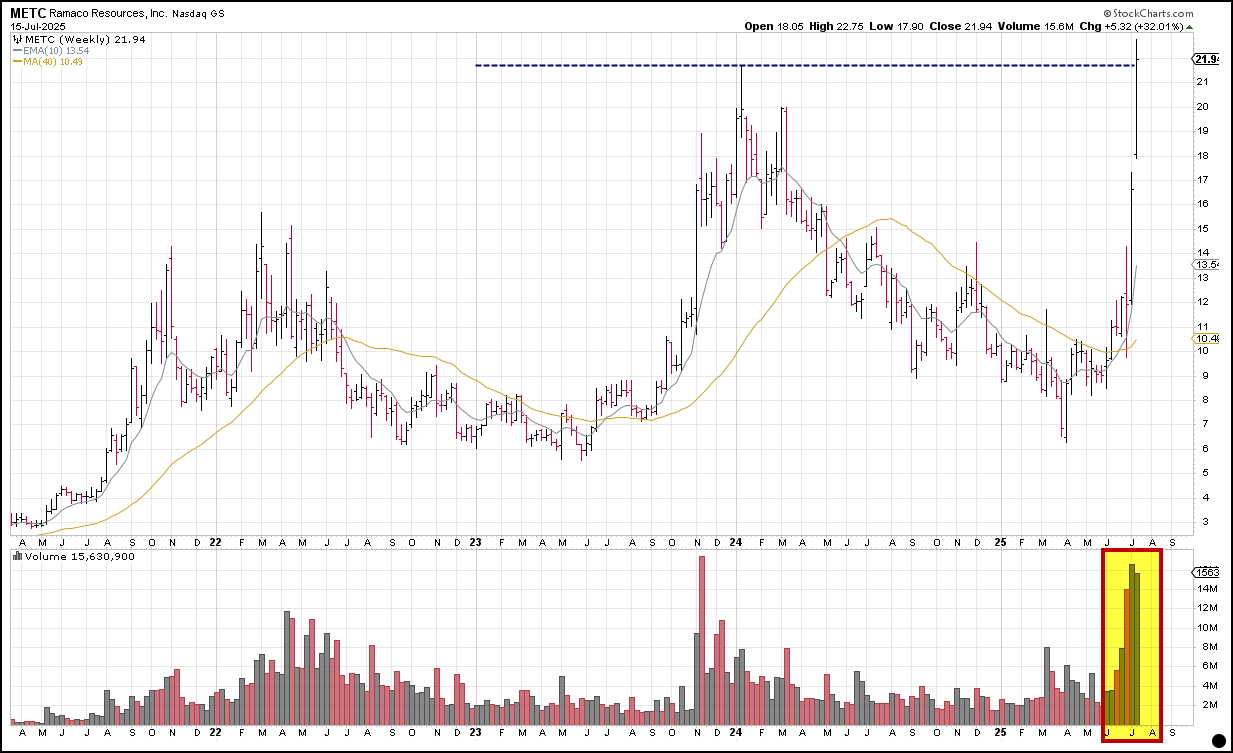

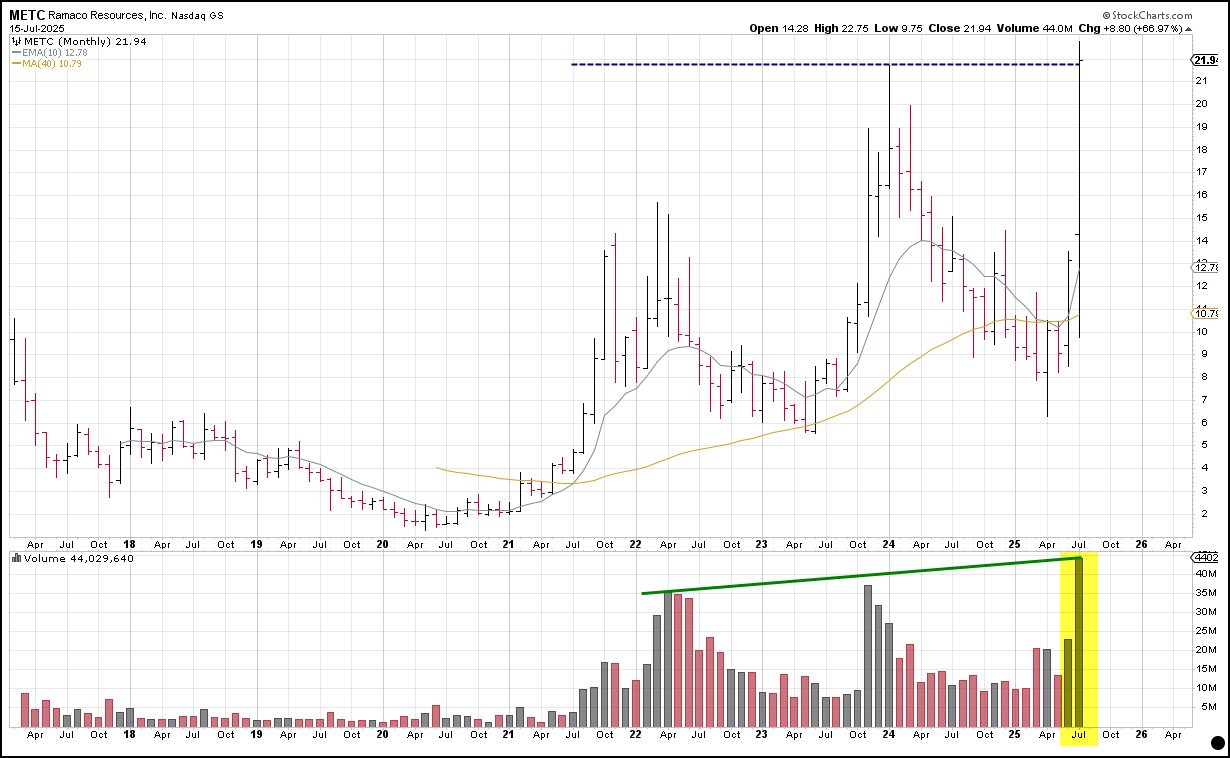

Turning to the technicals, METC has traded three of its biggest volume days ever over the last week. It just made All-Time Highs today.

Stocks making ATH's from 8 year bases – we focus on METC was $15 eight years ago, not that it has doubled the last week – typically stage dramatic moves in the following months and quarters. That has how multi-baggers happen. And this is what we think is unfolding here.

We are very bullish on METC in the low-to-mid $20s. We plan to add to our stock and options position this morning. In the coming days, we will add to our positions tactically on dips to $20-$23 as well.

Stop Loss: Implementing a 3-Month Time Stop here, as we want to ride this 10-conviction name for the for-mentioned likely near-term catalysts still ahead. We expect them to drive meaningful additional upside to the shares.

Execution remains the front-and-center risk in the Ramaco story. As Management attested, the company is “blazing some new ground here” and its own refining processes have yet to be optimized. This includes the design and construction of a full-scale commercial plant.

Financing also presents a risk as the company intends to explore external options and/or tapping the public market to raise the $600M in CapEx required for its new processing plant.

Finally, the capriciousness nature of the current administration brings headline risk, should Trump change his mind on REEs or strike a subsequent deal with China. We feel the odds are very low for this, however.

---------------------------------------------------------------------------

Disclosure: We are long METC stock and calls. We may change our positioning at a moment’s notice, without notifying you of any such moves.

Disclaimer: All of the information in this piece has been prepped by Inflections Consulting LLC. Readers should know that it would be incorrect to assume that past and future names of interest will be profitable or will not turn into a loss. Inflections Consulting LLC does not and will not assume any liability for any loss that could occur if you invested in such stocks written about.

All the content in these reports have been prepared by Inflections Consulting LLC. We believe our sources to be reliable, but there is no guarantee here. The information in this piece does not constitute either an offer nor a solicitation to buy or sell any of the securities name-dropped in this piece.

All contents are derived from original or published sources believed reliable, but not guaranteed. This report is for the information of Top Tier Inflections members/subscribers, only. Absolutely none of our content may be reproduced in whole or in part without prior written permission from Inflections Consulting LLC. All rights reserved.

In no shape or manner should the views expressed in this piece be considered investment advice. We reserve the right to change our positioning in our METC stock and options positions at a moment’s notice without updating you on any such change in opinion and positioning. That may be tomorrow, even before our price target is hit. Facts change, our opinions can change quickly too.

Investors need to consider their investment risk tolerance before investing in the stock market and also before investing in any of the stocks mentioned in this report.