Sezzle Inc. (SEZL) did it again.

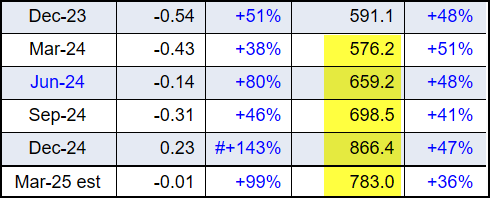

Not just another beat and raise, but a decisive acceleration in its top line during a seasonally weak quarter:

As they did throughout last year, forward guidance for the entire year was also dramatically raised:

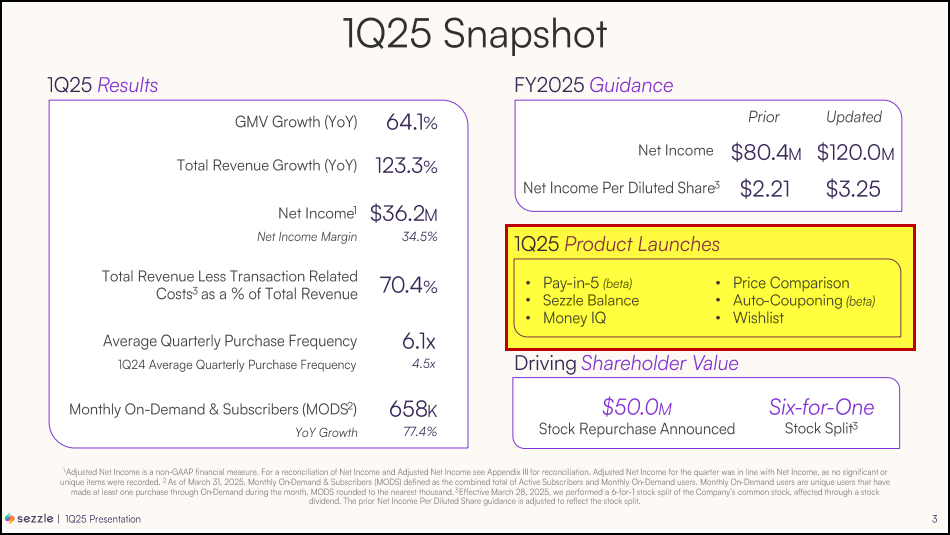

Sezzle raises FY25 adjusted EPS view to $3.25 from $2.21.

Raises FY25 revenue view to up 60-65% from up 25-30%.

"Our investments in innovation and consumer experience drove new highs in engagement and performance in the first quarter," noted Charlie Youakim, Sezzle Chairman and CEO.

"Stronger consumer activity and better-than-expected repayment trends propelled quarterly earnings above our expectations. These positive developments give us the confidence to raise our 2025 Net Income guidance by nearly 50% to $120M."

Importantly, due to a host of new products ramping with its banking partner, WeBank, and its new OnDemand product scaling quickly, further upside to consensus is likely.

This is how a typical Buy-Now Pay Later E-Commerce company (in this case, Affirm Holdings, Inc. - AFRM) revenue ramp looks during the year, Q1 down from Q4, with a steady sequential ramp during the year:

Because Sezzle is much smaller than Affirm, the company is a lot nimbler, able to release a multitude of new products in the last few quarters that are only hitting scale now.

Looking ahead, a few new important products are ready to ramp in Q3, too, which will provide additional catalysts to its business on top of its typical seasonal tailwinds.

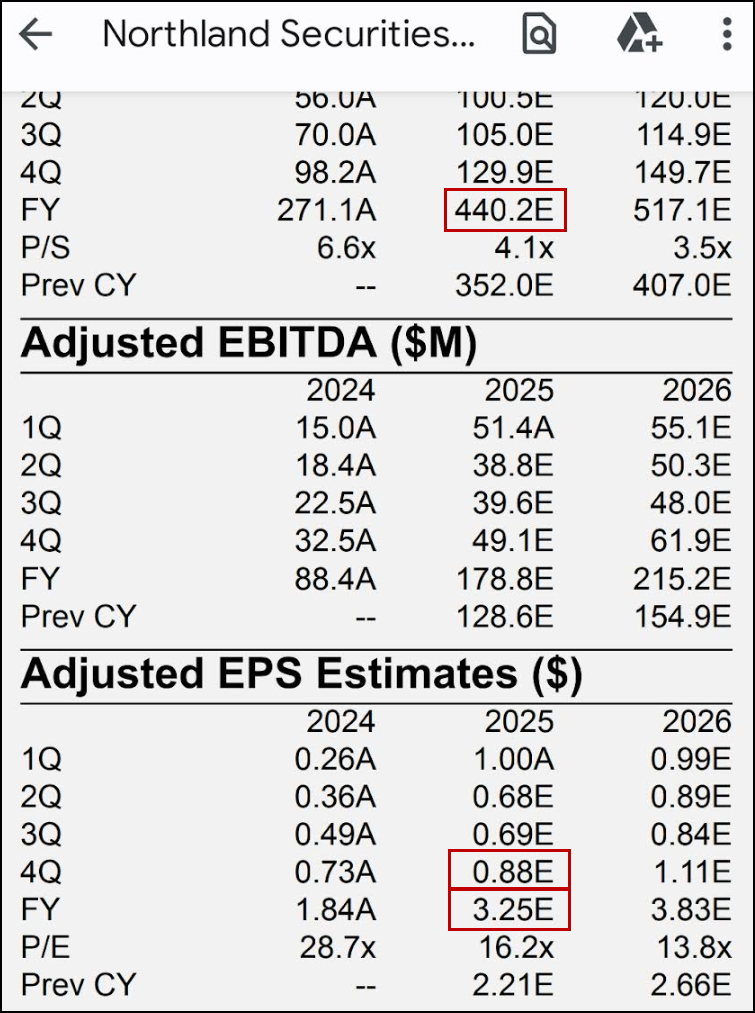

So, we look at Northland's model (the analyst has been spot on) and we still see massive upside this year, to ~$500M in revenues and $5.50 in EPS. For instance, we are at $1.75-$2 in EPS for Q4 (the best quarter of the year) WELL ABOVE Northland’s $0.88:

A key reason for the major upside has been Sezzle's ability to drive consumer engagement. To wit, 6.1x quarterly purchases vs 4.5x in last year's Q1. Consumers are using Sezzle's app more and more.

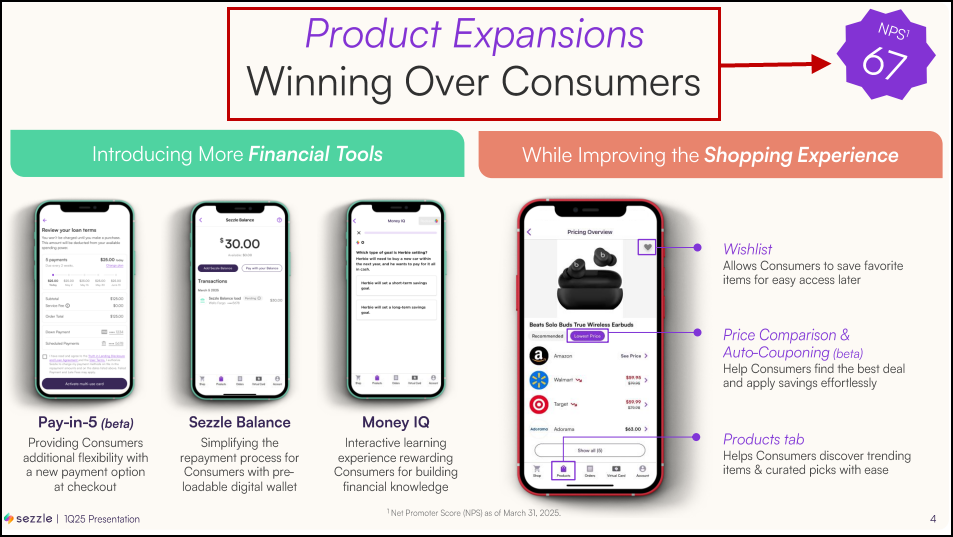

Why? A host of new products keep coming out, enhancing the appeal of the app for consumers:

Here is a more in-depth summary. Note the high 60s NPS score. Consumers love Sezzle:

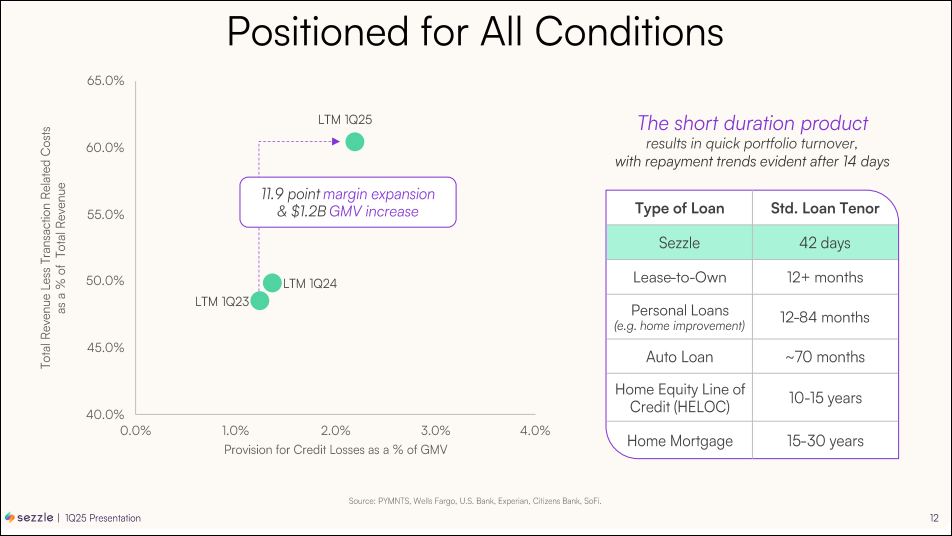

On the credit side, Sezzle will soon be able to offer a number of new banking products with its WeBank partnership. The WeBank partnership has also enhanced Sezzle’s overall profitability too. In Q1, credit defaults performed much better than expectations:

We think SEZL will earn ~$5.5 in EPS this year, FY25, on ~$495-$500M in revenues. While its top-line growth will decelerate in 2026 to 35-40%, we still see revenues closing in on $700M with $7.5-$8 in EPS.

Young consumers love Buy Now/Pay Later. A weakening economy drives the Buy Now/Pay Later flywheel. While Sezzle is only the #5 player in the Buy Now Pay Later space, it is growing double-digits the next few years. Sezzle is taking share from the bigger players in a vector experiencing dynamic growth.

Net-net, its early days for Sezzle and we see strong odds the company will be approaching $1B in sales in 2027. Amazing, especially when you consider Sezzle was only founded 7/8 years ago.

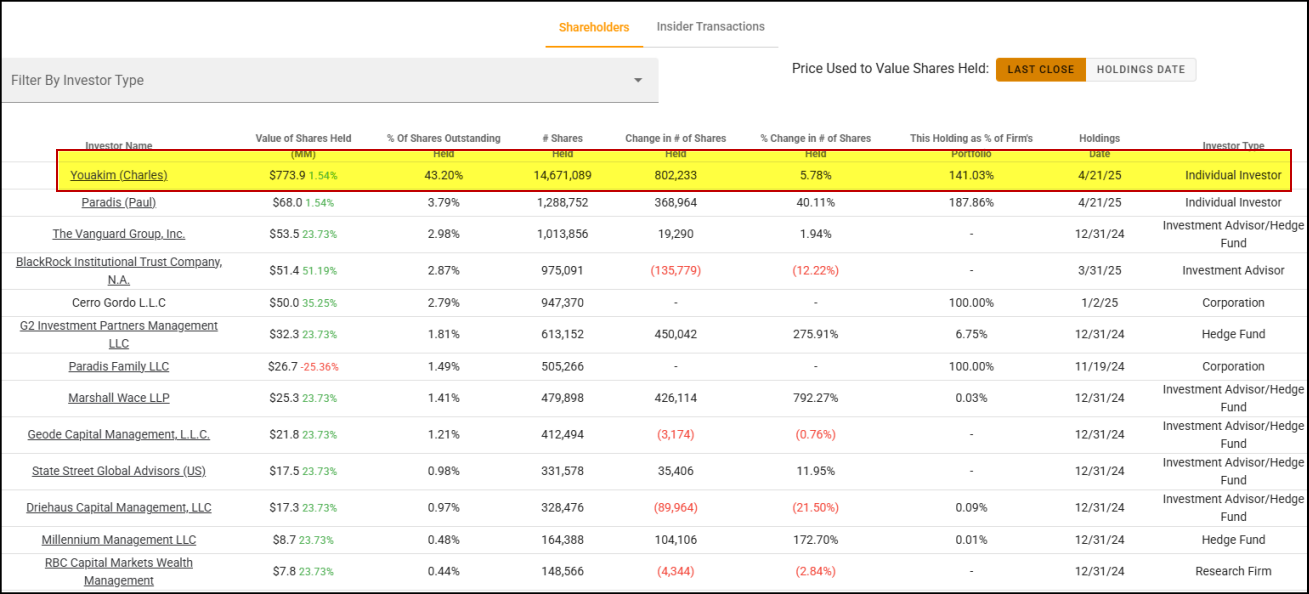

Finally, a big hat tip to SEZL's CEO, Charlie Youakim, who is a huge Buffett acolyte. While the stock was a huge multi-bagger winner last year, he held his entire stake:

Youakim knows what he has here, a company poised to scale to $500M and $1B not that far down the road.

This type of growth will typically garner an 8x Price-to-Sales multiple. At $100, which is our near-term price objective on the shares (by early summer), SEZL will trade for 5x likely-2026 numbers. So, long-term upside to $150-$250 is still viable over next 2-3 years, as well.

This type of overshoot becomes feasible when you consider the very tight float (17.06M shares) still in play with Sezzle.

We initiated our position in After Hours last night and added to it in the pre-market this morning. We would start a small position this morning and look to add on any flushes to the mid-to-high $60s.

We will look to scale out of our position as the stock moves to $85, $90 and $100. We plan to keep a third of our SEZL position, after $100, to ride for long-term gains.

Stop Loss: Given our conviction on SEZL, our stop is very loose at $61, specifically set to give this room to trade and play out.

Our Conviction Level is a 10.

Our math could be overly aggressive on our models. Any sharp economic downturn could lead to higher consumer default rates and, therefore, a lower multiple for Sezzle.

With numbers seemingly too-good-to-be-true, the shorts will almost certainly come at it again – although their cries will fall on deaf ears in the very short-term. With 10% of the stock currently short, expect the naysayers to get steamrolled today, just as they were in PRCH yesterday.

Sezzle’s quadruple-barrelled Top Tier Inflection was the best beat and raise we have seen in 2025.

------------------------------------------------------------------------

Disclosure: We are long SEZL stock and calls. We may change our positioning at a moment’s notice, without notifying you of any such moves.

Disclaimer: All of the information in this piece has been prepped by Inflections Consulting LLC. Readers should know that it would be incorrect to assume that past and future names of interest will be profitable or will not turn into a loss. Inflections Consulting LLC does not and will not assume any liability for any loss that could occur if you invested in such stocks written about.

All the content in these reports have been prepared by Inflections Consulting LLC. We believe our sources to be reliable, but there is no guarantee here. The information in this piece does not constitute either an offer nor a solicitation to buy or sell any of the securities name-dropped in this piece.

All contents are derived from original or published sources believed reliable, but not guaranteed. This report is for the information of Top Tier Inflections members/subscribers, only. Absolutely none of our content may be reproduced in whole or in part without prior written permission from Inflections Consulting LLC. All rights reserved.

In no shape or manner should the views expressed in this piece be considered investment advice. We reserve the right to change our positioning in our SEZL stock and options positions at a moment’s notice without updating you on any such change in opinion and positioning. That may be tomorrow, even before our price target is hit. Facts change, our opinions can change quickly too.

Investors need to consider their investment risk tolerance before investing in the stock market and also before investing in any of the stocks mentioned in this report.