Upstart Holdings, Inc. (UPST) crushed it. At least for now, Upstart wins the TOP TIER INFLECTION POINT AWARD for this Q4 2024 earnings season:

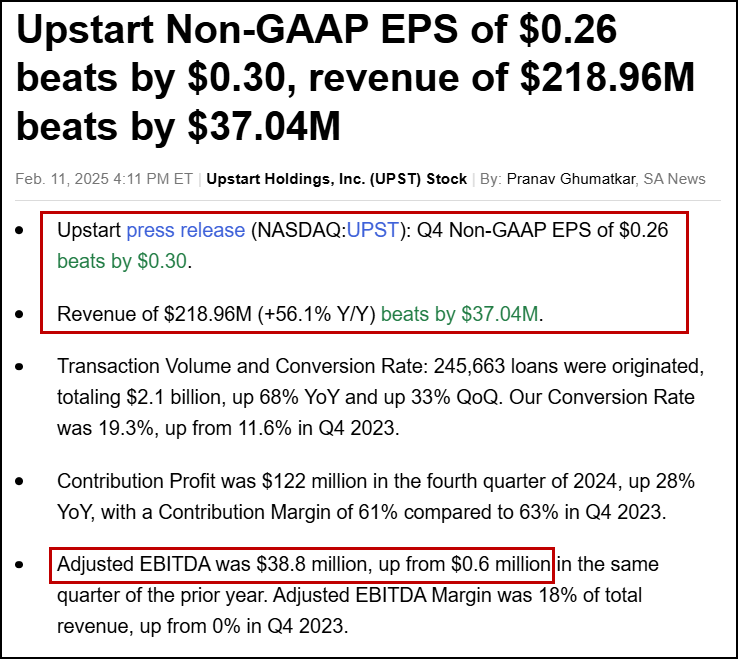

1. First, UPST did not just crush Q4, they OBLITERATED it:

Said Upstart Co-Founder/CEO, Dave Girouard:

"In Q4 of 2024, our business grew dramatically across all product categories, delivered Adjusted EBITDA at levels not seen since the first quarter of 2022, and came within a whisker of returning to GAAP profitability… We launched into 2025 with unparalleled energy and optimism for the future of Upstart AI lending and the mission we're on together.

This quarter was just so damn good. Here is where consensus was coming into the print:

Revenues bested consensus by $37.04M. This was 20% ABOVE consensus.

On many levels this report reminds me of the acceleration we saw in POWL, SMCI, ROOT and WGS before they went parabolic.

Like UPST, all of those companies delivered quadruple bareled inflection points, where the company not only beat on both revenues and EPS, but then also guided up strongly for its next quarter, finished off with a magnificent guide up for the ENTIRE YEAR.

Other super impressive stats, included:

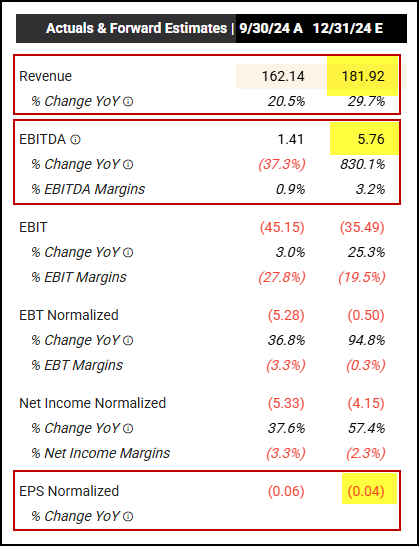

2. The Q1 guide was well above consensus, with room left for further upside acceleration in BOTH Q1 and Q2:

For Q1 2025, it expects revenue of ~$200M (vs. $184.6M Wall Street consensus); adjusted EBITDA of ~$27M (vs. $10.7M Visible Alpha estimate).

So, not only an 8% revenue beat, but also, a 152% BEAT GUIDE UP, relative to consensus.

3. And, then the icing on the cake - the eye opening guide up FOR 2025.

First, here is where consensus was:

For Q1 2025: Revenue of ~$200M (vs. $184.6M Wall Street consensus); Adj EBITDA of ~$27M (vs. $10.7M Visible Alpha estimate).

For FY 2025: Revenues of $1B (20% ABOVE CONSENSUS); EBITDA MARGINS WELL ABOVE CONSENSUS TO BOOT...

Considering this management team has been through the ringer - in 14 months, UPST cratered from $400+ down to $12.50 after a couple of BAD MISSES - they have done a much better job of framing and beating guidance handily this quarter and in Q3, as well. Super impressive.

The improvement seems poised to continue , with Upstart closing in on a few deals that will help offload half of the $800Mish in loans the company has on its balance sheet. UPST did two converts last year. I do worry they may do another one if the stock goes to $100 quickly, but that's a high class, short-term problem with an $84 cost.

With Upstart's quad-bareled inflection point manifesting so powerfully, we established a Top 5 position in UPST tonight.

We left room to add on dips to $81-$83. We would be shocked if $80 gave way on the first flush, but anything is certainly possible with Tariff Man hard at work every week.

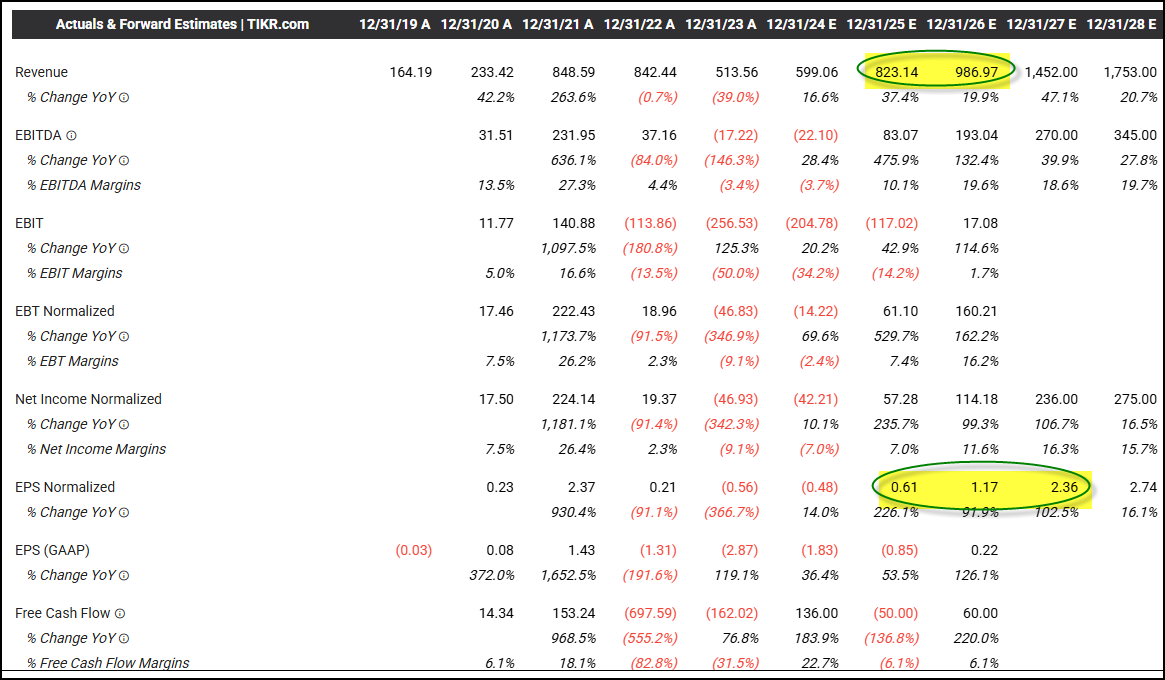

We think UPST will grow its revenues ~55% this year and could also see a 35% rise in 2026. In such scenarios, EPS will go from $2 this year to $4.00 next year.

We think the stock can gun to $100, perhaps quickly, especially with 20M shares short.

There are ~112M shares fully-diluted. So a $14B Market Cap, or 10x likely 2026 sales of $1.4B, would translate into an $125 stock the second half of this year.

With a tremendously enhanced balance sheet and private credit and other credit market players onboard, credit is available for Upstart to scale strongly this year. We expect its underlying profitability to inflect tremendously like it did in Q4, when expenses went up only 2%, while revenues grew 30%+ sequentially.

POWERFUL STUFF.

Longer-term, in a very good tape, UPST could eventually even garner a cra cra Price-to-Sales Multiple of 15x again, should its 2025 best consensus as strongly as we think it will. In a very good tape, UPST could even head toward $200, perhaps, a lot more quickly than anyone currently envisions.

Lastly, I love UPST's weekly. Lot of fuel here:

Gonna leave it there from me.

-----------------------------------------------------------------------

Disclosure: We are long UPST stock and calls. We may change our positioning at a moment’s notice, without notifying you of any such moves.

Disclaimer: All of the information in this piece has been prepped by Inflections Consulting LLC. Readers should know that it would be incorrect to assume that past and future names of interest will be profitable or will not turn into a loss. Inflections Consulting LLC does not and will not assume any liability for any loss that could occur if you invested in such stocks written about.

All the content in these reports have been prepared by Inflections Consulting LLC. We believe our sources to be reliable, but there is no guarantee here. The information in this piece does not constitute either an offer nor a solicitation to buy or sell any of the securities name-dropped in this piece.

All contents are derived from original or published sources believed reliable, but not guaranteed. This report is for the information of Top Tier Inflections members/subscribers, only. Absolutely none of our content may be reproduced in whole or in part without prior written permission from Inflections Consulting LLC. All rights reserved.

In no shape or manner should the views expressed in this piece be considered investment advice. We reserve the right to change our positioning in our UPST stock and options positions at a moment’s notice without updating you on any such change in opinion and positioning. That may be tomorrow, even before our price target is hit. Facts change, our opinions can change quickly too.

Investors need to consider their investment risk tolerance before investing in the stock market and also before investing in any of the stocks mentioned in this report.